Welcome to this week's edition of On the Moneyed Midways, a collection of the best posts from each of the week's blog carnivals dedicated to money and business-related matters, with one post declared to be The Best Post of the Week, Anywhere!(TM)!

Welcome to this week's edition of On the Moneyed Midways, a collection of the best posts from each of the week's blog carnivals dedicated to money and business-related matters, with one post declared to be The Best Post of the Week, Anywhere!(TM)!

We've been intensely busy with other projects this week, but we still found time to find the best money, business and career-related posts the blogosphere has to offer, all offered for your review below....

| On the Moneyed Midways: July 29, 2006 | |||

|---|---|---|---|

| Carnival | Contributor | Post | Comment |

| Carnival of Business | How to Catch Employees Stealing | sequence.inc | Did you ever wonder how companies catch thieving employees? Tracy Coenen links to her article in the Wisconsin Law Journal to show how. |

| Carnival of Business | A Penny Saved | Samablog | Rob Sama has done something I've been meaning get around to one of these days - build a tool to figure out how whether it's worth your while to melt down your pennies! He doesn't include the costs of sorting, smelting, transportation, storage and transactions, but it's still makes for a fun exercise! |

| Carnival of the Capitalists | The Selection Decision | ExecuPundit | Michael Wade reveals some of the inner corporate dynamics that came into play in a company's CEO selection process. |

| Carnival of Career Intensity | Happy People are the Key | BOB - Business Opportunities Blog | Marcus Markou writes that "passionate people breathe life into a business. They take the business to new levels. But how do you make people passionate about business?" |

| Carnival of Debt Reduction | Simple Debt Reduction Strategies | No Credit Needed | NCN walks through an example for how to create your own unique debt reduction strategy. |

| Carnival of Investing | Making Money Work for You | Wealth Building World | Bob Curtis provides a primer for what beginning investors need to do to start making their money work for them, in a post that's essential reading for all investors. |

| Carnival of Personal Finance | What's in Your Wallet? Cash or Credit? | How To Make a Million Dollars | No, it's not a CapitalOne blogad. G at How to Make a Million Dollars says that you should be carrying cash *and* credit in your pocketbook and that you should use them differently. |

| Carnival of Marketing | Pop Music's Lessons For Marketing | David Maister's Passion, People and Principles | It's getting hard to go a week and not select a contribution by David Maister. This week, David asks questions that many fans of pop have might have asked over the years, including why music doesn't seem to matter as much as marketing? |

| Festival of Frugality | Check Out These 5 Gas Myths | Blueprint for Financial Prosperity | Jim uncovers five myths (via CNN Money) about saving gas when driving. |

| Personal Development Carnival | Insider Secrets to Interviewing Success: How to Get the Job You Want | Leadership Findings | Kingsley Tagbo has interviewed at a lot of companies over the years and has done very well in getting job offers. Here, he shares his interview guide in The Best Post of the Week, Anywhere! |

| Personal Growth Carnival | The Secret to Breaking Out of the Box | J. Timothy King's Blog | J. Timothy King asks the question: "How often do we rule out choices because of our mistaken beliefs?" then shows how to break out of that box. |

Previous Editions

- On the Moneyed Midways – July 29, 2006

- On the Moneyed Midways – July 21, 2006

- On the Moneyed Midways – July 14, 2006

- On the Moneyed Midways – July 7, 2006

- On the Moneyed Midways – June 30, 2006

- On the Moneyed Midways – June 23, 2006

- On the Moneyed Midways – June 16, 2006

- On the Moneyed Midways – June 9, 2006

- On the Moneyed Midways – June 2, 2006

- On the Moneyed Midways – May 26, 2006

- On the Moneyed Midways – May 19, 2006

- On the Moneyed Midways – May 12, 2006

- On the Moneyed Midways – May 5, 2006

- On the Moneyed Midways – April 28, 2006

- On the Moneyed Midways – April 21, 2006

- On the Moneyed Midways – April 14, 2006

- On the Moneyed Midways – April 7, 2006

- On the Moneyed Midways – March 31, 2006

- On the Moneyed Midways – March 24, 2006

- On the Moneyed Midways – March 31, 2006

- On the Moneyed Midways – St. Patrick's Day 2006 Edition

- On the Moneyed Midways – March 10, 2006

- On the Moneyed Midways - The inaugural edition from March 3, 2006!

Roughly every month and a half, the Federal Reserve's Open Market Committee meets in a dark cellar with a dark purpose - to sacrifice a goat and to read its entrails so that they might set the level of the Federal Funds Rate.

Or something like that. The truth is that there's precious little public knowledge about what exactly the Fed does when it sets the interest rate that it charges banks for overnight loans to support their operations.

Fortunately however, there's a whole platoon of Fed-watching economists and analysts who have created their own methods of reading the Fed's tea leaves to divine what the Fed will do. Today's new tool is based upon a method for estimating what level the Fed is ultimately targeting when it sets the Federal Funds Rate that was developed by Greg Mankiw, Harvard professor, former chairman of the President's Council of Economic Advisors, and experienced practioner of the dark, dismal science.

Mankiw's method for estimating the Federal Funds Rate was outlined in his May 2001 paper on U.S. Monetary Policy During the 1990s (available as a 96KB PDF document) and again in a recent blog entry.

To use the tool, you'll need two simple bits of data:

- The current Consumer Price Index inflation rate (excluding food and energy) over the last 12 months.

- The current Seasonally Adjusted Employment Rate.

And that's all - now you too can, in the words of Mankiw, "set interest rates like a pro!"

Using the tool's default data, which is current as of May/June 2006, the method estimates that the Fed should set the Federal Funds Rate to 5.42%. At the current level of 5.25%, this suggests that the Fed may be very close to its desired target rate for the current economic circumstances, with a good probability that the Fed's Open Market Committee will increase the rate once again by .25 points to 5.5%.

At least, that is, until current economic circumstances change again - then its back off to the basement with a frightened goat....

Welcome to this week's edition of On the Moneyed Midways, a summary of the best posts from each of the week's blog carnivals dedicated to money and business-related matters, with one post declared to be The Best Post of the Week, Anywhere!(TM)!

Just scroll down for the best posts the week that was....

| On the Moneyed Midways: July 21, 2006 | |||

|---|---|---|---|

| Carnival | Contributor | Post | Comment |

| Carnival of Business | Superachievers' Top Ten | Career Intensity | David Lorenzo defines what makes superachievers so special and weighs in on how you can develop their traits. |

| Carnival of the Capitalists | The Island of Venezuela | View from a Height | Joshua Sharf shows how Hugo Chavez' policies are removing Venezuela from the bloodflow of the world's economy. |

| Carnival of the Capitalists | The Brute Force Approach to Productivity | Slow Leadership | Carmine Coyote wonders why businesses almost always revert to brute force methods (increasing time worked without increasing staff) to improve their productivity numbers. |

| Carnival of Career Intensity | Acres of Diamonds: What Are You Looking For? | Emmanuel Oluwatosin: Inspiring Excellence, Realising Ambitions | Emmanuel Oluwatosin recounts the legend of Ali Hafed, a man who left everything behind for the promise of great wealth. |

| Carnival of Debt Reduction | Student Loan "Dilemma" | Blueprint for Financial Prosperity | Jim confronts the desire to pay off student loan debt despite its low interest rate compared to his other debt. |

| Carnival of Investing | When Being Bad Pays | Don't Mess with Taxes | Kay Bell examines the counterpoint to socially responsible investing! |

| Carnival of Personal Finance | Inside FSBO Offer Negotiations | 2million - My Journey to Financial Freedom | 2million takes you inside his negotiations for a home. The Best Post of the Week, Anywhere! |

| Carnival of Marketing | No One Knows How Advertising Works | planningblog | Carol in London attended a recent talk Robert Heath gave at an Account Planning Group meeting - lots of insight into what works in advertising. |

| Carnival of Wal-Mart | The Cost of Working at Wal-Mart | Nice Cookies | Stacey Lynn did the math to find out how much less money she would spend at Wal-Mart if she didn't work there. |

| Festival of Frugality | Getting the Cheapest Shipping | MomAdvice | Amy Allen Clark has found a new option for shipping packages cheaply - a great post for those with shops at E-bay or Amazon! |

| Personal Development Carnival | A Defeat Is Not a Failure | Bouncing Back | Jeannie Bauer finds a very profound truth behind the difference between defeat and failure. |

Previous Editions

- On the Moneyed Midways – July 21, 2006

- On the Moneyed Midways – July 14, 2006

- On the Moneyed Midways – July 7, 2006

- On the Moneyed Midways – June 30, 2006

- On the Moneyed Midways – June 23, 2006

- On the Moneyed Midways – June 16, 2006

- On the Moneyed Midways – June 9, 2006

- On the Moneyed Midways – June 2, 2006

- On the Moneyed Midways – May 26, 2006

- On the Moneyed Midways – May 19, 2006

- On the Moneyed Midways – May 12, 2006

- On the Moneyed Midways – May 5, 2006

- On the Moneyed Midways – April 28, 2006

- On the Moneyed Midways – April 21, 2006

- On the Moneyed Midways – April 14, 2006

- On the Moneyed Midways – April 7, 2006

- On the Moneyed Midways – March 31, 2006

- On the Moneyed Midways – March 24, 2006

- On the Moneyed Midways – March 31, 2006

- On the Moneyed Midways – St. Patrick's Day 2006 Edition

- On the Moneyed Midways – March 10, 2006

- On the Moneyed Midways - The inaugural edition from March 3, 2006!

Earlier this week, the New York Times announced that it would be shrinking the size of its pages to save money. Oh, and its staff too. Again.

Here's a quick timeline of New York Times recent history of staff reductions:

- January 2001

- New York Times announces that it will cut 69 jobs of its Internet staff (at the time, 17% of its Internet workforce.)

- April 2001

- New York Times announces will begin across-the-board layoffs. Job cuts include 100 employees from its regional newspaper group.

- May 2005

- New York Times annouces staff reductions of 190 employees (less than 2% of workforce).

- September 2005

- New York Times announces layoffs of 500 employees (4% of workforce.)

- July 2006

- New York Times announces will shrink newspaper (newsprint), news (5%) and employee headcount by 250 (2%).

By our count, we find that the New York Times has laid off some 1109 employees in the six years since the beginning of the century, a little over 8% of the total number of its employees in 2000.

The Real Question

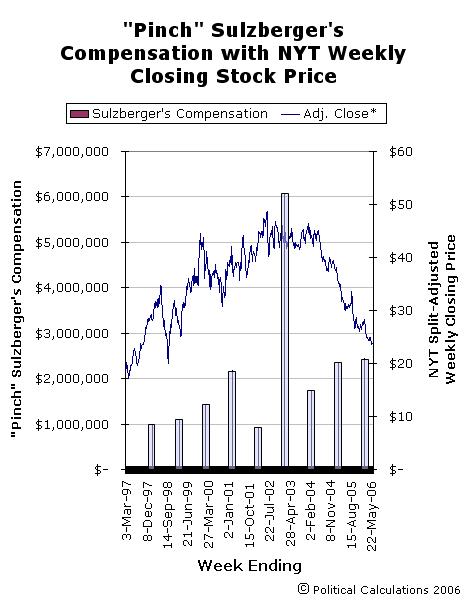

Of course, the real question has nothing to do with how many hard-working people the New York Times will slash from its payroll. Oh, no. The real question is: How will the same business conditions that have led to the ongoing shrinkage (in workforce, and now literally) of the New York Times affect publisher Arthur "Pinch" Sulzberger's annual bonus?

What makes this question relevant is how the New York Times' Board of Directors acted just last year, as the Times' management team, led by Sulzberger, moved to reduce its staff by 500 people as a permanent cost savings measure. Despite the newspaper's stagnant business condition, which apparently required the ouster of 4% of its staff, they awarded him a substantial bonus of $560,521 in cash and granted him restricted stock units worth $817,500 - on top of his $1,055,596 annual salary for a grand total of $2,433,617 in total financial compensation.

But, let's put the situation at the New York Times differently - we'll compare the newspaper's business condition (represented by its stock price) with Sulzberger's compensation in the chart below:

Is Pinch in for a pay cut this year? Draw your own conclusions, but consider the following two questions and answers....

Why was Pinch's pay so low in 2001? We've listed Sulzberger's compensation in the chart above as occurring when the New York Times annual report for the previous year's business was released - in this case, in March 2001. Here, Pinch's low pay level is the result of the New York Times' falling advertising revenues throughout 2000, which led, in good part, to the paper's layoffs later in 2001. Sulzberger did not receive a bonus for that year, which accounts for its "low" level compared to other years.

Why did Pinch get such a huge spike in compensation in 2002? It might have something to do with what the New York Times called the largest circulation gains it experienced in over 10 years, which also coincided with the papers Pulitzer-prize winning coverage of the terrorist attacks on the U.S. on September 11, 2001 (it won seven Pulitzers - its most ever in a single year.)

The paper's performance since then, reflected in its recently announced cost reduction measures, suggests that Sulzberger's compensation in 2002 was grossly excessive as the New York Times has moved away from the balanced coverage of stories of both great national and local interest.

Because of that factor, it's difficult to see a responsible board of directors approving any bonus for the newspaper's management team in the upcoming year. It may all be a moot point however since Sulzberger's family controls the company's board and can set whatever minimal and arbitrary performance requirements it desires in setting its compensation policies for executive bonuses.

Previously on Political Calculations

Harrison Loke of Finandom recently reviewed an article by Otesa Middleton Miles on the Bankrate.com web site, which looked at the math that real estate investors should do when making investment decisions. The math behind determining a property's capitalization rate caught our eye and has inspired our latest tool!

Harrison Loke of Finandom recently reviewed an article by Otesa Middleton Miles on the Bankrate.com web site, which looked at the math that real estate investors should do when making investment decisions. The math behind determining a property's capitalization rate caught our eye and has inspired our latest tool!

The capitalization rate for a real estate investment property is the ratio of annual net rental income received for the property divided by its purchase price, which is expressed as a percentage. It's useful in that it allows an investor to compare potential real estate investments by property values independently of how the financing for the properties being considered would be structured (amount of down payment, interest rates, closing costs, etc.)

Here's the data you'll need to use the tool:

- Annual rental income.

- Annual operating expenses (not including mortgage payments.)

- The property's purchase price.

And that's all! Here's the tool:

How To Use the Capitalization Rate as an Investor

The article quotes real estate investor Doug Crowe for how an investor would use this information:

If you're selling a property, says Crowe, "It's better to have a buyer willing to accept a lower cap rate. But if I'm buying, I want a high cap rate." For instance, if you buy a property with a cap rate of 8 percent and did nothing to it but raise the price, the cap rate drops to 7 percent. You've made a profit.

The article notes that capitalization rates of 7-8% are common in the midwest region of the U.S., while 6% is common on the coasts.

Previously on Political Calculations

- Investing in Real Estate for Cash Flow - our tool for calculating cash-on-cash return!

Labels: investing, real estate, tool

Recently, Political Calculations asked and answered the question of how well American families are handling their debt using data from the Federal Reserve's 2004 Survey of Consumer Finances, which was published in February 2006. Today, we're going back to that source to answer a different question - who's more likely to be in debt: the rich or the poor?

Using net worth as our metric for determining wealth status, we'll first look at who's in debt by seeing how many people in each of the report's net worth percentile brackets (profiled here) have any debt of any kind. The following table has been extracted from Table 11 (p A28) of the survey report:

| Debt Holding Status by Net Worth Percentiles | ||

|---|---|---|

| Net Worth Percentile Bracket | Percentage of Families in Bracket with Debt | Percentage of Families in Bracket Without Debt |

| 0 - 25 | 64.9% | 35.1% |

| 25 - 50 | 83.8% | 16.2% |

| 50 - 75 | 83.2% | 16.8% |

| 75 - 90 | 74.6% | 25.4% |

| 90 - 100 | 72.7% | 27.3% |

Remarkably, we see that the poorest group, defined as those in the 0 to 25th net worth percentile bracket, are the least likely to even have debt, with 35.1% of this group being debt free! Instead, we find that the group most likely to have debt is in the 25th to 50th percentile bracket, whose net worth ranges from $13,300 at the low end to $93,100 at the high end. The second most likely group to have debt, following closely behind the 25-50th percentile group, is found in the 50th to 75th percentile bracket, where the net worth of families at the top end of the bracket is $328,500.

Who might have guessed that those with the lowest net worth would be the least likely to have debt?!

Previously on Political Calculations

Labels: debt management

If only there was a place on the web where you could catch up on all the best blog posts from all of the business, money and career-related blog carnivals. Wait a minute! Isn't that what On the Moneyed Midways, a summary of the best posts from each of the week's blog carnivals dedicated to money and business-related matters, with one post declared to be The Best Post of the Week, Anywhere!(TM) is all about?

Well, you know the answer to that question, otherwise you would have hit the back button on your browser already! Just scroll down for the wrap-up of the week that was....

| On the Moneyed Midways: July 14, 2006 | |||

|---|---|---|---|

| Carnival | Contributor | Post | Comment |

| Carnival of Business | Forming an S-Corporation to Reduce Self Employment Taxes | My Money Blog | If you are, or if you're thinking about, working for yourself, this post may well help you work out how to set up your enterprise. |

| Carnival of Business | Price Controls | InsureBlog | Bob Vineyard reflects on the unintended, yet expected consequences that price controls on pending health insurance legislation will have. |

| Carnival of Career Intensity | Triple Your Free Time: 4 Simple Steps | RadicalHop | Peter Kua says that "you don't have free time because you don't have a strategy for it" and shows how you can take action to see that you get the free time you need. |

| Carnival of Debt Reduction | Plan to Curb Out of Control Spending | DebtFree4ever.net | Kevin Surbaugh reveals how unplanned spending strained his ability to retire his outstanding debt and shares what changes he'll be making to better control his finances. |

| Carnival of Investing | Financial Phobia | Young and Broke | Amanda notes the situation of people who are otherwise "intelligent and perfectly competent in other areas of their lives but are struck dumb at the notion of dealing with investments and other financial matters." |

| Carnival of Marketing | The New Sales Cycle: Forecast Failure in 8 Easy Steps | Jack Yoest | Jack Yoest provides a list of the things to look for when failure is headed toward your sales department. |

| Carnival of Personal Development | How to Avoid Greed? | My Financial Awareness | Pete finds that "there is nothing wrong with having money. The problem is when we define ourselves by what we have or do not have." |

| Carnival of Personal Finance | How I Learned to Care About Economics | Experiments in Finance | Ricemutt, a lifelong American, is stunned by the common knowledge of economics in the Dominican Republic. The Best Post of the Week, Anywhere! |

| Carnival of Wal-Mart | What Is Wal-Mart Worth to a Town? | Palousitics | How valuable is the world's largest retailer to a small town? Tom Forbes shines a light on what Homer, Louisiana lost when Wal-Mart pulled up stakes in the town. |

| Festival of Frugality | Ceiling Fans - Just a Waste of Money? | JMcGready's Misc. Universe | Ceiling fans are often touted as having year-round energy savings, but J McGready looks at an article that shows studies find that's not-so-true during the heating season. |

| Festival of Job Hunting | Are You Climbing to the Top When There Is No Top? | Aridni | "How much is the big guy making?" asks Katie when considering job possibilities, who notes that your long-term goals should play an important role in pursuing your career options. |

| Personal Development Carnival | Here There Be Dragons! | On Making Money | Fear of the unknown often stops people in their tracks. Eric demonstrates that the real heroes are those who overcome their fears and slay the dragons. |

Previous Editions

- On the Moneyed Midways – July 14, 2006

- On the Moneyed Midways – July 7, 2006

- On the Moneyed Midways – June 30, 2006

- On the Moneyed Midways – June 23, 2006

- On the Moneyed Midways – June 16, 2006

- On the Moneyed Midways – June 9, 2006

- On the Moneyed Midways – June 2, 2006

- On the Moneyed Midways – May 26, 2006

- On the Moneyed Midways – May 19, 2006

- On the Moneyed Midways – May 12, 2006

- On the Moneyed Midways – May 5, 2006

- On the Moneyed Midways – April 28, 2006

- On the Moneyed Midways – April 21, 2006

- On the Moneyed Midways – April 14, 2006

- On the Moneyed Midways – April 7, 2006

- On the Moneyed Midways – March 31, 2006

- On the Moneyed Midways – March 24, 2006

- On the Moneyed Midways – March 31, 2006

- On the Moneyed Midways – St. Patrick's Day 2006 Edition

- On the Moneyed Midways – March 10, 2006

- On the Moneyed Midways - The inaugural edition from March 3, 2006!

How much debt do Americans have and can they handle it?

How much debt do Americans have and can they handle it?

To answer these questions, we here at Political Calculations went to the Federal Reserve's 2004 Survey of Consumer Finances (SCF), which provides a breakdown of the median amount of debt (of any kind) held by the surveyed families. The Fed interviewed some 4,552 families, which through the miracle of statistical sampling, represent approximately 112.1 million families in the United States!

The survey report breaks down its data by a number of different methods (age, income, work status, etc.), but the method we found most interesting was by net worth. The following table shows the breakdown of the percentile brackets by which the report presented its data, along with the corresponding median income and net worth for each bracket range:

| 2004 SCF Net Worth Percentile Data | |||

|---|---|---|---|

| Net Worth Percentile Bracket | Median Income | Median Net Worth | Net Worth at Top of Bracket |

| 0 - 25 | $20,500 | $1,700 | $13,300 |

| 25 - 50 | $37,000 | $43,600 | $93,100 |

| 50 - 75 | $52,400 | $170,700 | $328,500 |

| 75 - 90 | $77,000 | $506,800 | $831,600 |

| 90 - 100 | $143,800 | $1,430,100 | N/A |

So that's the basic profile of who's been surveyed. Now, let's see the median debt that each grouping has along with their median debt burden, which is defined as the percentage of debt payments divided by income (also called the debt-to-income ratio.) This latter figure gives us a good indication of how well the families surveyed are able to manage their debt:

| Median Debt and Median Debt Burden by Net Worth Percentiles | ||

|---|---|---|

| Net Worth Percentile Bracket | Median Debt Held | Median Debt Burden |

| 0 - 25 | $11,400 | 13.0% |

| 25 - 50 | $44,200 | 21.2% |

| 50 - 75 | $90,100 | 21.4% |

| 75 - 90 | $110,700 | 17.9% |

| 90 - 100 | $190,800 | 12.6% |

We can measure how well families manage debt by seeing where they fall on the debt burden scale. Lending institutions are reluctant to extend credit for individuals whose debt-to-income ratio is greater than 36% - often charging people with a debt ratio above 36% higher rates of interest to discourage them from exceeding this debt burden level. Since the median debt held in each grouping is well below this level, it indicates that overall, Americans are in pretty good shape when it comes to managing their debt.

Labels: debt management

If McDonalds really wants to improve its margins, it should offer the McDonald Sandwich on its menu.

What ever happened to this group of losers?

The Airbus behemoth is in trouble - but that's nothing compared to the state of the company's business and its underlying management turmoil. Why is it that companies need to strike an iceberg before dealing seriously with their inherent problems?

Finally, a conspiracy theory I can fully endorse!

Is the New York Times being rejected by its readers?

In New York City, at least, the answer appears to be "Yes." The following chart illustrates the declining importance of the newspaper's circulation in the 31-county area that makes up its home market, which has dropped from representing 64% of its total weekday circulation in 1993 to just 49% in 2005. Numerically speaking, the New York Times' circulation in the "Big Apple" has fallen some 27.1% from more than 757,000 in September 1993 to almost 553,000 in September 2005, according to data derived from the NY Times parent company's annual 10-K SEC filings:

The chart also shows that the New York Times has been able to largely avoid the continuing decline in overall circulation being experienced by local newspapers across the United States, declining only 4.8% overall during this 15 year period. By contrast, the Los Angeles Times, the second largest daily newspaper in the U.S., has seen its circulation drop from 1,104,317 in 1993 to 843,432 in 2005 - a decline of 23.6%.

The New York Times has thus far avoided a fate similar to the Los Angeles Times through a concerted campaign that it launched in 1998 to focus upon becoming a national newspaper, rather than being the leading newspaper in the U.S.' largest city.

Interestingly, both the New York Times and the Los Angeles Times share a strong leftist editorial bias that has become much more stringent in the years from 1993 to the present day. One wonders how much of the erosion of each paper's local circulation may be due to their editorial board's growing contempt for opposing viewpoints held by a large percentage of the population in their home markets.

Recommended Further Reading

Thomas Lifson and Jack Risko provide a neat analysis of the state of the New York Times' business in All the Risk That's Fit to Disclose from March 2, 2006 in The American Thinker.

Do you have a Home Equity Line of Credit (HELOC)? Have recent interest rate hikes made it unappealing as a source from which to draw credit? Consider the following scenario presented by CNN/Money magazine (HT: Mapgirl's Fiscal Challenge):

Home-equity lines of credit were the crack cocaine of the home-improvement binge of the past few years, and it's easy to see why.

Three years ago, the minimum monthly payment on a $100,000 line of credit was just $333. But now that the prime interest rate (which is the rate most HELOCs are pegged to) has doubled to 8 percent, the minimum is $666.

If you can't pay off the HELOC, you may be able to convert it to a conventional loan.

Another solution is to refinance it and your mortgage into a single fixed-rate loan - if, that is, you can find a rate that beats what you are paying for both loans and saves you enough to cover refi costs.

So, that's what we're going to do! First, we'll need to determine your blended interest rate, which is where our latest tool comes into play! Just enter the appropriate data in the input fields below, and click "Calculate" to find your effective combined interest rate between your mortgage and HELOC:

Now, you have the key information you need to shop for a new mortgage where you might consolidate your debt. By comparing the Blended Interest Rate you determined above to the mortgage rates available today (in our view, Bankrate.com provides an excellent starting point for shopping for loans), you can quickly determine if consolidating your loans this way makes sense for you by seeing if lower mortgage rates are available.

But before you take the plunge, don't forget to take the cost of refinancing along with the potential of saving money in the long run into your considerations - Political Calculations has developed tools to help you do the math where these factors are concerned!

Labels: debt management, tool

Welcome again to this week's edition of On the Moneyed Midways, where we round up the best posts from each of the blog carnivals dedicated to money and business-related matters, with one post declared to be The Best Post of the Week, Anywhere!(TM)

Since this week covered the Fourth of July holiday, several carnivals were on hiatus, including the popular Festival of Frugality, but we uncovered two new carnivals to fill the gap: The Carnival of Home Business and the monthly Carnival of Taxes. So just scroll on down for all the best business and money blogging in the week that was the first week of July 2006!

| On the Moneyed Midways: July 7, 2006 | |||

|---|---|---|---|

| Carnival | Contributor | Post | Comment |

| Carnival of Business | Alignment and Accountability | David Maister's Passion, People and Principles | Quoting David: "Companies are most successful when they are built on - and live up to - a solid, clearly articulated ideology (also known as a mission or values.)" |

| Carnival of the Capitalists | Business Fundamentalism Revisited | Slow Leadership | Carmine Coyote searches for the right balance of belief and evidence in business management. The Best Post of the Week, Anywhere! |

| Carnival of Career Intensity | The Best Type of Business to Be In | Paul's Tips | Paul finds the secret to success in business is to focus upon improving your business' "template:" "It's the template, not any of the individual strategies or stores, that creates the most value." |

| Carnival of Debt Reduction | Making My Money Count | The Family CEO | The Family CEO uncovers extra income from surprising sources and applies it to paying down the family's credit card balances. A very neat post for finding bonuses on the web! |

| Carnival of Home Business | The Barriers to Starting Your Own Business | Matt Inglot | Matt Inglot identifies Lack of Time, Too Much Risk, Lack of Knowledge and Fear of the Unknown as the major barriers to launching a new business - and also links to resources for overcoming each of these barriers! |

| Carnival of Investing | Investment Selection: How to Evaluate a Company's Management | Free Money Finance | FMF interviews Fred Kobrick, the author of The Big Money on the importance of evaluating the quality of company management when deciding where to invest. |

| Carnival of Marketing | Birth of a New Advertising Medium | Jos'Blog | Jos. Birken uncovers something new afoot in the world of advertising - ads that can be seen from space, or more precisely, ads that may be seen from space via Google Earth. Who knew it would come to this?! |

| Carnival of Personal Finance | Pay Off Your Mortgage Early? | Debt Free | Does it make sense for you to pay off your mortgage early? Debtlog weighs the options. |

| Carnival of Taxes | Who Does Uncle Sam Audit? | Brian Brown, CPA | Brian Brown lists the various "triggers" that spark the agents of the United States Internal Revenue Service to start going through all your financial records with a fine tooth comb. |

| Personal Development Carnival | 11 Ways of Staying Focused | David Cheong | David Cheong provides his guide to keeping on task when working and notes that the 11 techniques he presents apply in both personal and business settings. |

Previous Editions

- On the Moneyed Midways – July 7, 2006

- On the Moneyed Midways – June 30, 2006

- On the Moneyed Midways – June 23, 2006

- On the Moneyed Midways – June 16, 2006

- On the Moneyed Midways – June 9, 2006

- On the Moneyed Midways – June 2, 2006

- On the Moneyed Midways – May 26, 2006

- On the Moneyed Midways – May 19, 2006

- On the Moneyed Midways – May 12, 2006

- On the Moneyed Midways – May 5, 2006

- On the Moneyed Midways – April 28, 2006

- On the Moneyed Midways – April 21, 2006

- On the Moneyed Midways – April 14, 2006

- On the Moneyed Midways – April 7, 2006

- On the Moneyed Midways – March 31, 2006

- On the Moneyed Midways – March 24, 2006

- On the Moneyed Midways – March 31, 2006

- On the Moneyed Midways – St. Patrick's Day 2006 Edition

- On the Moneyed Midways – March 10, 2006

- On the Moneyed Midways - The inaugural edition from March 3, 2006!

People borrow money for all sorts of reasons, but when it comes to refinancing their loans, people predominantly choose to do so for what comes down to be two simple reasons:

- To increase personal cash flow by reducing the size of their loan payments.

- To increase their wealth by reducing the total amount paid over the remaining life of the loan.

Political Calculations has previously looked at whether it makes sense to refinance a loan purely on the basis of whether an individual's increased cash flow would cover the costs of refinancing, but today, we'll investigate the second reason people choose to restructure their debt.

The tool below has been set up with default data that shows the individual's monthly payment going up substantially after refinancing. Does it make sense to refinance given this circumstance? Just click the "Calculate" button to find out!

As an added bonus, you can use the tool below with your own numbers to determine whether or not it makes sense to refinance your loan by comparing how much you would have paid if you simply let your existing loan ride against what you'll pay if you refinance:

Some Analysis

Using our default data, we see that even if your monthly payment costs go up after refinancing, it's still possible that you will save money overall, depending upon the size of your new payment and how long your new loan lasts!

Then again, if the amount of your payments went up *and* you have a negative result in the tool above, it would be much to your advantage to keep your existing loan as it is.

Labels: debt management, tool

Welcome to the blogosphere's toolchest! Here, unlike other blogs dedicated to analyzing current events, we create easy-to-use, simple tools to do the math related to them so you can get in on the action too! If you would like to learn more about these tools, or if you would like to contribute ideas to develop for this blog, please e-mail us at:

ironman at politicalcalculations

Thanks in advance!

Closing values for previous trading day.

This site is primarily powered by:

CSS Validation

RSS Site Feed

JavaScript

The tools on this site are built using JavaScript. If you would like to learn more, one of the best free resources on the web is available at W3Schools.com.

Other Cool Resources

Blog Roll