On their most fundamental level, changes in stock prices are primarily driven by changes in the expected rate of growth of their underlying dividends per share. More specifically, the amount of the change in stock prices occurs in direct proportion to the magnitude of the change expected to occur in the growth rate of dividends per share at specific points in time.

On their most fundamental level, changes in stock prices are primarily driven by changes in the expected rate of growth of their underlying dividends per share. More specifically, the amount of the change in stock prices occurs in direct proportion to the magnitude of the change expected to occur in the growth rate of dividends per share at specific points in time.

We have to point this out because, according to Felix Salmon, there is no other possible explanation for the Dow Jones Industrial Average to have dropped 268.22 points (2.65%) to 9,879.30, the Nasdaq 100 to have dropped 85.45 points (3.85%) to 2,135.18 and the S&P 500 to have fallen some 33.33 points (3.10%) to 1,041.24 on 29 June 2010:

What do you call a market which rises on bad news and panics — as it's doing today — on no news at all? The 10-year Treasury is now yielding less than 3%, the Dow's back below 10,000, the VIX is over 30, and the Nasdaq is down 2.4% in a matter of minutes; French stocks have fallen more than 3% today, and in general the global risk-aversion trade seems to be back on.

Interestingly, gold is down a little today: maybe at these levels it's more of a risk asset than a safe haven. But more generally I think we're seeing what happens to markets which are much more global, complex, and interconnected than they’ve ever been in the past: correlations can appear out of nowhere, and it's silly to even attempt to explain significant intraday market movements by recourse to anything in the news.

That didn't stop reporters like Angela Moon from trying to pin the blame for the drop in stock prices on a sharp decline in consumer confidence in the U.S., but that reporting misses the rather obvious point that all the indices started the day in the "pit of despair," as stock price futures were down well before any of the consumer confidence news hit the airwaves.

So how do we know that something fundamental is behind the action in the market on 29 June 2010? It turns out that's a simple question to answer. It's because the market is behaving as though it is!

Here's our chart showing the relationship between the change in the rate of growth of stock prices with the change in the expected future rate of growth of dividends per share for the S&P 500:

What we think is going on is that investors have shifted their forward-looking focus in time for setting stock prices to be one or two quarters further forward in time than 2011-Q2, the most distant future quarter for which we have dividend futures data, which we've indicated in the chart above by the dashed red lines.

Using the expected change in the rate of growth of the S&P 500's dividends per share for 2011-Q2 as a base reference point, investors are acting as though they expect the S&P 500's dividends per share to fall to $23.31 from the $23.57 currently expected to be reached in June 2011. We won't know for sure that's the case until the distant futures data for 2011-Q3 and 2011-Q4 becomes available, but for now, it's the best we can do with the data we do have available to us [1].

If those figures hold, they would indicate that investors anticipate that the U.S. economy will enter back into a recession, or at least into microrecession, in the latter half of 2011. The expected negative acceleration of dividends per share then would largely be responsible for the decline we've observed in stock prices since April 2010.

For July 2010, assuming investors maintain their focus on whatever future quarter in 2011 that produces this negative acceleration, we can expect average stock prices for the S&P 500 to average somewhere in the range of 1014 and 1052, with 1033 as the effective midpoint of the range.

Side Notes

[1] Our regular readers will recall that we first did a similar exercise to anticipate that the stock market was about to begin its downward descent back on 4 May 2010, where we used the then most distant future available data from the fourth quarter of 2010 as the reference point in time from which to project where dividends would need to be to coincide with where the acceleration of stock prices suggested it might be.

We found back then that to produce the same deceleration from that highly elevated level of positive acceleration, dividends per share would have to drop to $20.88 from 2010-Q4's projected $21.88 per share to produce the equivalent negative acceleration. The difference in the projected dividend we calculate now as compared to then is entirely attributable to the different reference points we used from which to base our calculations along with minor changes in the expected future level of dividends that have taken place in the time since.

Ironically, the level of dividends per share have generally been rising over much of that time. However, it's what the expected acceleration of dividends per share at specific points in time where investors have focused their attention that matters when it comes to projecting where stock prices will be in the very near future!

Labels: chaos, dividends, forecasting, SP 500

Ever since Apple rolled out the original iPhone and made mobile-phone based computing applications hipper than hip, we've been seeking to develop the ultimate viral mobile app. And with the iPhone 4 having just been released, coupled with the pending release of the Droid-X phones built through an unholy alliance between Verizon and Google [1], we finally decided it was time to strike!

So we're pulling out all the stops and applying everything we've learned in developing hundreds of online applications over the past several years, and especially what we learned from the very few that went viral.

So we're pulling out all the stops and applying everything we've learned in developing hundreds of online applications over the past several years, and especially what we learned from the very few that went viral.

What lessons are those? Here's the short summary:

A. It has to easily solve a common, if perhaps underestimated, problem.

B. That problem should have something to do with avoiding disaster in male-female relationships.

C. And involve alcohol (aka "The cause of, and solution to, all of life's problems.")

That's harder to do than you might think. But we've done it, thanks to groundbreaking research commissioned by Bausch & Lomb into determining the exact threshold of alcohol consumption at which people who you might previously have found to be visually unattractive while sober instead become irresistibly attractive! Here's the 2005 news article describing the scientific achievement:

That's harder to do than you might think. But we've done it, thanks to groundbreaking research commissioned by Bausch & Lomb into determining the exact threshold of alcohol consumption at which people who you might previously have found to be visually unattractive while sober instead become irresistibly attractive! Here's the 2005 news article describing the scientific achievement:

Scientists believe they have worked out a formula to calculate how "beer goggles" affect a drinker's vision.

The drink-fuelled phenomenon is said to transform supposedly "ugly" people into beauties - until the morning after.

Researchers at Manchester University say while beauty is in the eye of the beer-holder, the amount of alcohol consumed is not the only factor.

Additional factors include the level of light in the pub or club, the drinker's own eyesight and the room's smokiness.

The distance between two people is also a factor.

They all add up to make the aesthetically-challenged more attractive, according to the formula.

The popularly known "beer goggles" effect is known to lead to all sorts of embarrassing, if not incredibly uncomfortable social situations, especially if an intimate encounter takes place while under the effect.

And that's the basis of what we'll describe as our ultimate mobile app! Now, thanks to modern cellular technology and our newest tool, both men and women will be able to assess just how impaired their visual judgments might be when it matters most - when they can still back out of a developing social situation during a night of fun that might otherwise become completely awkward the next day on account of personal aesthetics!

Before today's technology, men and women out on the town would have had no way to put the formula to effective use, but now that all changes because all it takes is just a few quick entries and the ultimate mobile app will do the math for you. On the spot. Even if you're already well into your evening and your judgment is already well impaired!

Here's the quick guide for interpreting the results:

A formula rating of less than one means no effect. Between one and 50 the person you would normally find unattractive appears less "visually offensive".

Non-appealing people become suddenly attractive between 51 and 100. At more than 100, someone not considered attractive looks like a super model.

Of course, since you're likely impaired as you are using this app, the app will communicate this information to you in more direct terms.

So go ahead and take it for a test drive! If you've read down this far, you know you'll be needing it soon, or better yet, you know someone who needs to know about it....

[1] We assume any relationship that requires any sort of payment to George Lucas for any reason to be unholy.

Image Credits: blog.usa.gov and the Standard Drinks Model

Labels: geek logik, none really, satire, tool

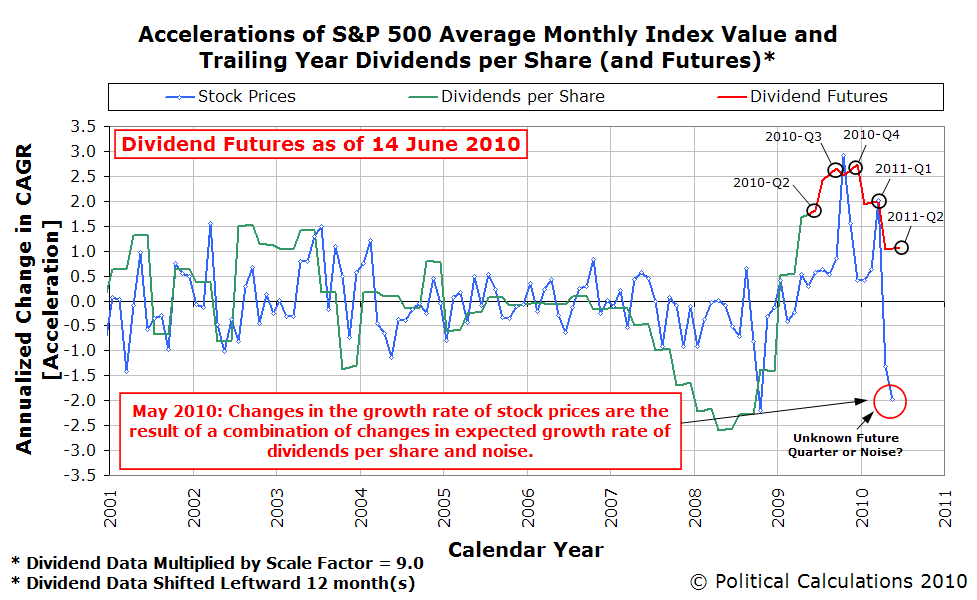

Can we draw a single graph that captures exactly what investors have been seeing since the middle of last year when they look ahead at the prospects for the U.S. economy?

Our chart below shows how the S&P 500's trailing year dividends per share have been projected to change into the future since 14 July 2009 for each quarter where we have dividend futures data available:

In addition to our comments presented on the chart, we'll also note that the growth in expected cash dividend payouts between the fourth quarter of 2010 and the first quarter of 2011 is unusually strong.

That result may be an artifact of the time frame for which the stock index futures contracts apply. Here, for any given quarter, these futures run through the end of the third week of the month in which the quarter ends.

So, for example, the futures contract that applies for the fourth quarter of 2010 will expire on 17 December 2010. Any cash dividends that are expected to be paid out to investors from that date forward through the end of the contract covering the first quarter of 2011 includes dividend payments being made during the final weeks of December 2010.

That's significant this year since taxes on income received through dividend payments are scheduled to increase dramatically for any such income earned after 31 December 2010. Companies and investors may be acting to load up their dividend payments in 2010 to avoid having to pay higher taxes on that kind of income in 2011.

A more normal seasonal pattern would be for the quarterly payout of cash dividends to peak in the fourth quarter of a given tax year. That the first quarter of 2011 is set to have such a jump in dividend payouts is an indication that something unusual is at work.

A more normal seasonal pattern would be for the quarterly payout of cash dividends to peak in the fourth quarter of a given tax year. That the first quarter of 2011 is set to have such a jump in dividend payouts is an indication that something unusual is at work.

It also explains why we have such a discrepancy between what the dividend futures data indicates will be the level of trailing year dividends per share at the end of 2010 with what Standard & Poor indicates.

Here, Howard Silverblatt projects (via the spreadsheet for S&P 500 Earnings and Estimates provided under the Monthly Performance Data section of S&P's Market Attributes page) that trailing year dividends per share for the S&P 500 at the end of calendar year 2010 will be $23.67. By contrast, the December 2010 dividend futures contract that only covers the period through 17 December 2010 indicates that the trailing year figure for 2010 will be $22.32 per share.

That difference suggests that a lot of dividend payments are going to get crammed into the last two weeks of 2010 as investors play the grown-up version of "Beat the Clock."

Image Credit: Vintage Game World

Labels: dividends, SP 500, taxes

Welcome to the Friday, June 25, 2010 edition of On the Moneyed Midways! Each week, we read dozens of posts contributed to the best money and business-related blog carnivals so we can point you to the best posts we found in each!

Welcome to the Friday, June 25, 2010 edition of On the Moneyed Midways! Each week, we read dozens of posts contributed to the best money and business-related blog carnivals so we can point you to the best posts we found in each!

It's clearly summer, as many of the carnivals we regularly feature are on vacation this week! And in the spirit of summer, where we'd much rather be doing anything other than working, we're just going to get straight to this week's edition!

The best posts we found in the week that was are ready to launch your essential weekend reading....

| On the Moneyed Midways for June 25, 2010 | |||

|---|---|---|---|

| Carnival | Post | Blog | Comments |

| Carnival of Debt Reduction | Obama Credit Card Debt Relief: Will the President Pay Your Debts? | ptMoney | "No. He won't." PT takes on some of the more bizarre and deceptive advertising that some really shady debt settlement companies have adopted to exploit the President's ever-expanding series of bailouts. |

| Carnival of HR | Establishing a Culture of Distributed Leadership | Great Leadership | What does it take to have junior leaders able to take charge and get positive results without having to wait for their superiors in their organizations to act? Dan McCarthy explains in The Best Post of the Week, Anywhere! |

| Carnival of Personal Finance | Does Going to Work Actually Cost You Money? | Red Stapler Chronicles | RutgersKevin tells some tall tales inspired by the movies and TV to describe how some employees escaped from having to participate in their office pools and community fundraising activities. |

| Festival of Frugality | Selling on Craigslist | Live Real, Now | It's the top pick in this week's Festival of Frugality, and we agree! LRN delivers the concise guide to selling your stuff on Craigslist. |

| Carnival of Money Stories | I Admit, I'm a Cheater (and I Don't Feel Guilty) | Money Beagle | We were both shocked and dismayed to find out the Money Beagle is a cheater. But oddly enough, we're okay with it too, seeing as Mr. Beagle is legitimately shopping around for a good deal. |

| Best of Money | Walmart vs. Super Market vs. Commissary | Richly Reasonable | Does Wal-Mart really provide the best deals? And how does it compare to the commissaries that are available for military personnel and their families? Lauren comparison shops to find where the best deals are! |

OMM's Running Index for 2010

Presented in reverse chronological order....

- On the Moneyed Midways - June 25, 2010

- On the Moneyed Midways - June 18, 2010

- On the Moneyed Midways - June 11, 2010

- On the Moneyed Midways - June 4, 2010

- On the Moneyed Midways - May 28, 2010

- On the Moneyed Midways - May 21, 2010

- On the Moneyed Midways - May 14, 2010

- On the Moneyed Midways - May 7, 2010

- On the Moneyed Midways - April 30, 2010

- On the Moneyed Midways - April 23, 2010

- On the Moneyed Midways - April 16, 2010

- On the Moneyed Midways - April 9, 2010

- On the Moneyed Midways - April 2, 2010

- On the Moneyed Midways - March 26, 2010

- On the Moneyed Midways - March 19, 2010

- On the Moneyed Midways - March 12, 2010

- On the Moneyed Midways - March 5, 2010

- On the Moneyed Midways - February 26, 2010

- On the Moneyed Midways - February 19, 2010

- On the Moneyed Midways - February 13, 2010

- On the Moneyed Midways - February 5, 2010

- On the Moneyed Midways - January 29, 2010

- On the Moneyed Midways - January 23, 2010

- On the Moneyed Midways - January 15, 2010

Older Editions

- OMM: The Best Posts of 2009 and our full index for the year!

- OMM's Running Index for 2008

- OMM's Running Index for 2007

- The Best Blogs Found in 2006 (and our full 2006 index)!

Labels: carnival

Having established that a new trend in employee layoffs began between 14 November 2009 and 21 November 2009, we've modified the statistical chart we originally presented yesterday to show its full extent.

In doing that, we also recalculated the typical range of natural variation we would expect to see for the previous trend, and in doing so, found an anomaly. The data for 11 July 2009 falls outside that range, which is defined as being within three standard deviations of the mean linear trend line for the data defining the trend.

In doing that, we also recalculated the typical range of natural variation we would expect to see for the previous trend, and in doing so, found an anomaly. The data for 11 July 2009 falls outside that range, which is defined as being within three standard deviations of the mean linear trend line for the data defining the trend.

We recognize this point as an outlier in the data for the trend that existed between 28 March 2009 and 14 November 2009, in that the following data points quickly returned to follow the primary trend line. But we also recognize that there must be a specific cause for such a deviation from the trend.

As it happens, the only economic factor that could have impacted the decision of businesses for retaining employees that occurred at this time is the government's Car Allowance Rebate System (CARS, aka "Cash for Clunkers") stimulus program.

As we noted yesterday, changes in established trends for seasonally adjusted initial unemployment claim filings typically lag two to three weeks behind the events that change the future economic outlook for businesses. With the Cash for Clunkers program signed into law on 24 June 2009 and taking effect on 1 July 2009, we find no other coinciding events that would potentially affect business staffing decisions on a large scale. The program ran through 24 August 2009.

As we noted yesterday, changes in established trends for seasonally adjusted initial unemployment claim filings typically lag two to three weeks behind the events that change the future economic outlook for businesses. With the Cash for Clunkers program signed into law on 24 June 2009 and taking effect on 1 July 2009, we find no other coinciding events that would potentially affect business staffing decisions on a large scale. The program ran through 24 August 2009.

With the program's limited duration, the benefits for American workers in the form of avoided layoffs from the stimulus program were very short-lived. We note that before the dates of the program, the number of initial unemployment claims filed were above the trend line in 10 of 13 weeks, while following the program, the number of initial unemployment claims filed were above the trend line in 7 of 12 weeks. During the program's run, the number of initial unemployment claims filed were only above the trend line in three of eight weeks, indicating that the program was successful in avoiding a higher number of layoffs in the other five weeks that it ran.

The data indicates that the Cash for Clunkers program did not significantly alter the established trend in layoffs during this period, which was declining in any case.

Which brings us to the present. We were incorrect in stating yesterday that Geoff of Innocent Bystanders hadn't identified a potential cause driving the current trend in U.S. layoffs. He did, finding that the introduction of health care legislation in the House of Representatives on 29 October 2009 was the likely cause of the deviation from the previously established trend, fully beating us to an analysis-based conclusion that was the likely cause by two weeks! And then, he first speculated that might the case back on 15 April 2010, long before we began putting the pieces together ourselves.

Yeah, we've added Innocent Bystanders to our blog roll!...

Labels: jobs

The U.S. government measures the number of layoffs in the U.S. economy by counting the number of Initial Unemployment Insurance Claims made each week. We thought it would make for a neat project to go back through the last four years of that data to see if we could successfully apply our statistical dating analysis technique, which would make it possible to isolate what events may have triggered major shifts in layoff activity in the United States throughout that time.

The chart to the right reveals what we found when we looked at all the reported data in the time from 20 May 2006 through 22 May 2010. Here, we determined that there were five major trends during this period, where we determined the mean trend line and the range of natural variation we would expect to see for each subperiod. That range of natural variation for each trend is defined as being within three standard deviations of the mean trend line that applies for each observed trend. Assuming that data follows a normal distribution, we would expect that any individual data point for a given trend would fall within this defined range some 99.8% of the time.

The chart to the right reveals what we found when we looked at all the reported data in the time from 20 May 2006 through 22 May 2010. Here, we determined that there were five major trends during this period, where we determined the mean trend line and the range of natural variation we would expect to see for each subperiod. That range of natural variation for each trend is defined as being within three standard deviations of the mean trend line that applies for each observed trend. Assuming that data follows a normal distribution, we would expect that any individual data point for a given trend would fall within this defined range some 99.8% of the time.

We recognize a break in an established trend whenever a data point falls outside that range of expected natural variation. The chart above shows four such breaks, which are indicated by the solid blue diamonds labeled with the indicated dates in blue: 24 November 2007, 26 July 2008, 2 May 2009 and 10 April 2010.

Missouri Unemployment Line Having found these break points, we use the new trend that is established afterward to track backwards to a point in time where we can identify that the new trend appears to have taken effect. We marked these points in time on the chart with solid red diamonds, which we recognize as being the end of the reporting period where the new trends established themselves.

Missouri Unemployment Line Having found these break points, we use the new trend that is established afterward to track backwards to a point in time where we can identify that the new trend appears to have taken effect. We marked these points in time on the chart with solid red diamonds, which we recognize as being the end of the reporting period where the new trends established themselves.

From here, it's just a matter of some detective work to determine what events led to the change in the rate at which businesses have laid off employees during the past four years. We do make two assumptions: First, businesses considering laying off employees require 2 to 3 weeks to act on their plans following a change in the outlook for their business. This time lag coincides with the typical weekly, biweekly, bimonthly and monthly pay periods for employees in the U.S., where we consider that businesses will follow through on executing their existing plans through their current pay period before implementing any changes driven by the change in their business outlook to coincide with their next pay cycle.

Second, we only consider events that would apply to the United States' job market. For example, the beginning of the Greek sovereign debt crisis would coincide with the new trend we observe beginning between 14 November 2009 and 21 November 2009, however since that crisis began with the announcement of a much larger-than-expected annual deficit, which would do little to affect the employee retention decisions of U.S. businesses, who were largely unaware of the news, we can exclude it as not relevant to their decision making.

We've presented our findings of the likely triggers for shifts in U.S. layoff activity in the table below:

| Timing and Events of Major Shifts in Layoffs of U.S. Employees | ||

|---|---|---|

| Date of Confirmed Break from Previous Trend | Period in Which New Trend Takes Effect | Likely Event Triggering New Employment Trend (Occurs 2 to 3 Weeks Prior to New Trend Taking Effect) |

| 24 Nov 2007 | 6 Oct 2007 - 13 Oct 2007 | Federal Reserve acts to slash interest rates for the first time in 4 1/2 years as it begins to respond to the growing housing and credit crisis, which coincides with a spike in the TED spread. Negative change in future outlook for economy leads U.S. businesses to begin increasing the rate of layoffs on a small scale. |

| 26 Jul 2008 | 21 Jun 2008 - 28 Jun 2008 | Oil prices spike toward inflation-adjusted all-time highs (over $140 per barrel in 2008 U.S. dollars.) Negative change in future outlook for economy leads businesses to sharply accelerate the rate of employee layoffs. |

| 2 May 2009 | 21 Mar 2009 - 28 Mar 2009 | Stock market bottoms as future outlook for U.S. economy improves, as rate at which the U.S. economic situation is worsening stops increasing and begins to decelerate instead. U.S. businesses react to the positive change in their outlook by significantly slowing the pace of their layoffs. |

| 10 Apr 2010 | 14 Nov 2009 - 21 Nov 2009 | Introduction of HR 3962 (Affordable Health Care for America Act) derails improving picture for employees of U.S. businesses, as the measure (and corresponding legislation introduced in the U.S. Senate) is likely to increase the costs to businesses of retaining employees in the future. Employers react to the negative change in their business outlook by slowing the rate of improvement in layoff activity. |

Coincidentally, we should note that President Barack Obama signed massive health care reform legislation into law just 2-3 weeks before the statistical confirmation of the break in the previous trend in U.S. layoffs occurred, so at least there's some sense of ironic symmetry there....

We note that Geoff at Innocent Bystanders has arrived at a similar conclusion regarding the beginning of a new trend in layoffs beginning in November 2009, but hasn't attributed a specific cause to account for the marked shift in layoff activity. Elsewhere, looking more closely at the most recent trend from its origin in mid-November 2009, he finds that it actually is somewhere between being flat to somewhat of an uptick in layoff activity.

If it does indeed turn out to be flat, it would represent the stabilization of layoff activity far above the seasonally adjusted average number of weekly new unemployment claims of 317,911 established in the last stable period that ended between 6 October 2007 and 13 October 2007. Which would be the last time the U.S. economy was anywhere near full employment levels.

Which if our finding holds, says a lot about President Barack Obama's signature achievement.

Labels: economics, jobs, quality

In a recent edition of our weekly best-of-the-business-blogosphere wrap up, On the Moneyed Midways, we featured a video of Dan Pink speaking at TED about what has been learned by behavioral researchers on how to effectively motivate people in business, calling it "the most potentially rewarding use of 18 minutes and 40 seconds of your time today."

Today, we're presenting an animated discussion of another Dan Pink performance, which covers very similar material in just 10 minutes and 48 seconds. It's even better.

HT: Core77

Labels: management, performance

In May 2010, George Washington University and Washington University in St. Louis jointly issued a report on the growth of government spending allocated in the annual budget of the United States' federal government for the purpose of regulating social and economic activity in the nation. Written by Susan Dudley and Melinda Warren, the report primarily focuses its analysis on the U.S. budgets for fiscal years 2010 and 2011. However, we were really taken with the stylized graph presented on the report's cover page.

In May 2010, George Washington University and Washington University in St. Louis jointly issued a report on the growth of government spending allocated in the annual budget of the United States' federal government for the purpose of regulating social and economic activity in the nation. Written by Susan Dudley and Melinda Warren, the report primarily focuses its analysis on the U.S. budgets for fiscal years 2010 and 2011. However, we were really taken with the stylized graph presented on the report's cover page.

The data in the chart is taken from Table 1 of the report and has been adjusted for inflation, with the figures presented in terms of constant 2005 U.S. dollars. We wondered if we could take that data, do a bit of rough regression analysis, then build a tool to both estimate how much government regulation cost U.S. taxpayers between Fiscal Year 1960 and Fiscal Year 2011 and project how much it would be likely to grow into the future.

So we dug deeper into the report and extracted the inflation-adjusted data for each year from Fiscal Year 1960 through 2011, which we found in Table A-5 of the report. Our graph, shown to the left, reveals what we found for the total of social and economic regulation for these years, as well as presenting our mathematical model of the overall trend through these years.

So we dug deeper into the report and extracted the inflation-adjusted data for each year from Fiscal Year 1960 through 2011, which we found in Table A-5 of the report. Our graph, shown to the left, reveals what we found for the total of social and economic regulation for these years, as well as presenting our mathematical model of the overall trend through these years.

What we find is that the cost of social and economic regulation in the United States, has been and is growing at an exponential rate.

The only exception to that pattern is represented by the short term spike in the cost of regulation in 2003, which coincides with the formation of the Transportation Security Agency and its bureaucracy following the September 11, 2001 terrorist attacks. The rate of growth of the cost of regulation has otherwise been consistently around the exponential rate of 5% per year.

But that's not accurate enough for us! We applied the data regression tools available at ZunZun to create the formula we presented in the chart above, so we can better project what the cost of social and economic regulation in the U.S. will be in the future, not to mention quickly estimating where it's been since 1960!

Going by our math, by the end of President Obama's first term in office in 2013, we could reasonably expect the cost of social and economic regulation to be on the order of 60 billion dollars. That's up from the $43.3 billion that regulation cost U.S. taxpayers in 2008.

And that's not even incorporating the cost of the President's health care reform law, which promises to add quite a lot of regulation to the bills that U.S. taxpayers must pay.

And that also doesn't take into account the cost that U.S. individuals and businesses have to pay to comply with U.S. regulations. That might take adding a few zeroes onto the numbers that the tool estimates!

Welcome to the Friday, June 18, 2010 edition of On the Moneyed Midways, the only place you can find the best posts that appeared in the best of the past week's business and money-related blog carnivals!

How can you avoid being a jerk when loaning money to your family members? How much can you save each month by toilet training your cat? Is Goldline a scam? If you've declared bankruptcy, can you still get an American Express card? How much life insurance should you have? Or how much long term care insurance do you need? How can your use of social media in the workplace lead you to get fired? And when should you pay off those pesky student loans?

Those are the questions being asked this week - the answers to these questions and more await you below!

| On the Moneyed Midways for June 18, 2010 | |||

|---|---|---|---|

| Carnival | Post | Blog | Comments |

| Carnival of Debt Reduction | Can I Get an American Express Credit Card After Bankruptcy? | Ask Mr. Credit Card | Mr. Credit Card says no, you can't on your own. But perhaps someone could make you an authorized user of theirs. |

| Carnival of HR | 7.2 Wasy to Get Fired with Social Media | Blogging 4 Jobs | Jessica Miller-Merrell shares the video of her live presentation describing how things like tweeting and facebooking can lead to the unemployment line. |

| Carnival of Personal Finance | Is Goldline a Scam | Bargaineering | Absolutely essential reading! Sure, as an investment, gold has never been worth zero, but Jim Wang wonders if one of the leading companies marketing investments in gold is really a scam. He thinks not, comparing them to people hawking $2 bottles of water outside ballgames and concerts. |

| Best of Money | How Much Extra Should You Pay on Student Loans | Foreigner's Finances | Austin Morgan takes on the complicated nature of student loans in considering what recent graduates need to consider when acting to pay off their loans. The emphasis on where to place students loans on your budget priority list make this The Best Post of the Week, Anywhere! |

| Cavalcade of Risk | The Eight Money Ratios, Part 4 | Free Money Finance | FMF specifies the rules of thumb for determining how much life insurance you need at any age from 25 to 65 as well as how much long term care insurance you might need. |

| Festival of Frugality | 27. Toilet Train Your Cats | 1000 Ways to Save a Buck | Can you train your cat(s) to be like Mr. Jinx in Meet the Parents and save money? Kelly identifies the stakes as being savings of $30/month if you can and lists a couple of kits designed to help you train your cat(s)! |

| Carnival of Money Stories | How to Loan Money to Relatives Without Being a Jerk | Complex Search | Nathan Richardson finds the secret to successfully loaning money to family members is to keep the terms of the deal really simple and to keep the relationship as honest as possible. |

OMM's Running Index for 2010

Presented in reverse chronological order....

- On the Moneyed Midways - June 18, 2010

- On the Moneyed Midways - June 11, 2010

- On the Moneyed Midways - June 4, 2010

- On the Moneyed Midways - May 28, 2010

- On the Moneyed Midways - May 21, 2010

- On the Moneyed Midways - May 14, 2010

- On the Moneyed Midways - May 7, 2010

- On the Moneyed Midways - April 30, 2010

- On the Moneyed Midways - April 23, 2010

- On the Moneyed Midways - April 16, 2010

- On the Moneyed Midways - April 9, 2010

- On the Moneyed Midways - April 2, 2010

- On the Moneyed Midways - March 26, 2010

- On the Moneyed Midways - March 19, 2010

- On the Moneyed Midways - March 12, 2010

- On the Moneyed Midways - March 5, 2010

- On the Moneyed Midways - February 26, 2010

- On the Moneyed Midways - February 19, 2010

- On the Moneyed Midways - February 13, 2010

- On the Moneyed Midways - February 5, 2010

- On the Moneyed Midways - January 29, 2010

- On the Moneyed Midways - January 23, 2010

- On the Moneyed Midways - January 15, 2010

Older Editions

- OMM: The Best Posts of 2009 and our full index for the year!

- OMM's Running Index for 2008

- OMM's Running Index for 2007

- The Best Blogs Found in 2006 (and our full 2006 index)!

Labels: carnival

Especially after you see this sign, which we offer in the spirit of Core77's "Imperiled Icons" bleg:

Yes, it's real.

Labels: none really

We first calculated the average individual American's effective oil consumption per day back in June 2008. Today, in considering Barack Obama's first Oval Office address to the nation, in which he stated his desire for individual Americans to transition away from consuming so much oil, we thought we'd revisit and update the data to see if Americans have been or are as wasteful with oil resources as the President would appear to believe.

The chart to the right reveals what we found when we took the U.S. Energy Information Agency's figures for the average number of thousands of barrels of Finished Petroleum Products Supplied to the U.S. per day, converted those figures to the equivalent number of U.S. gallons, then divided that result by the number of people within the United States, as measured by the U.S. Census' Resident Population Estimate for each month from January 1982 through March 2010 (we found that data in two places - here it is for between April 1980 through November 2000, and for April 2000 through the present).

The chart to the right reveals what we found when we took the U.S. Energy Information Agency's figures for the average number of thousands of barrels of Finished Petroleum Products Supplied to the U.S. per day, converted those figures to the equivalent number of U.S. gallons, then divided that result by the number of people within the United States, as measured by the U.S. Census' Resident Population Estimate for each month from January 1982 through March 2010 (we found that data in two places - here it is for between April 1980 through November 2000, and for April 2000 through the present).

What we find is that since January 1982, the average daily oil consumption for individual Americans living in the United States has averaged 2.56 gallons per person. More remarkably, we see that Americans have dramatically reduced their consumption of oil and its derivative products since July 2007.

So dramatically, in fact, that Americans today are consuming roughly one-third of a gallon per person less than they did on average from January 1982 through November 2007, the last full month before the largest recession in the U.S. since World War II began. As of March 2010, Americans are consuming an average 2.28 gallons of oil per day.

That drop has occurred even as the resident population of the United States steadily increased throughout this period, which means that most of the decline may largely be attributed to falling aggregate economic productivity during these years.

What's more, when we calculate the standard deviation of the individual American's effective daily oil consumption and plot lines indicating the "statistically normal" limits within which we would expect to find any data point some 99.7% of the time, we confirm that the oil consumption of individual Americans has already broken below what would be considered normal in more healthy economic circumstances.

What's more, when we calculate the standard deviation of the individual American's effective daily oil consumption and plot lines indicating the "statistically normal" limits within which we would expect to find any data point some 99.7% of the time, we confirm that the oil consumption of individual Americans has already broken below what would be considered normal in more healthy economic circumstances.

We should note that we've already identified a sharply falling demand for oil as being a key indicator of economic distress in the modern world.

We'll conclude by observing that Barack Obama would appear to already be getting his wish with respect to the oil consumption of Americans. Unfortunately for Americans desiring the return of a healthy economy, he would seem to not be satisfied with achieving his goals.

To generalize something we said before: "There are people who may want to blame anything bad having to do with oil on the collective buying habits and lifestyles of American consumers, but this is one dog that just won't hunt! You can safely rest assured that anyone who does so is just looking for an excuse to screw the American consumer over for their own personal benefit."

Labels: data visualization, gas consumption

In looking at the latest quarterly dividend futures data, we found what could well turn out to be a historical anomaly in the data if the future plays out as investors currently expect.

In looking at the latest quarterly dividend futures data, we found what could well turn out to be a historical anomaly in the data if the future plays out as investors currently expect.

Looking ahead to 2011, we see the first quarter of 2011 as a peak in the cash dividends per share expected to be paid out, with a projected $6.16 per share currently expected to be paid out to investors, which is both greater than the preceding expected fourth quarter payout in 2010 and the following expected second quarter payout of 2011.

What makes this extremely unusual is that in the quarterly data we have recorded by S&P in their Index Earnings data spreadsheet going back to the first quarter of 1988, this would be the only time we've ever seen that pattern in the available historical data. (Note: We have trailing year dividend data going back much farther.)

The proof of that may be seen in our following chart, in which we're showing the quarterly dividend data for the S&P 500 going back to the first quarter of 1998, through the dividend futures data going through the second quarter of 2011 that we have available as of today:

The usual pattern is to see dividends per share to peak in the fourth quarter of each year, as companies seek to pay out a larger share of the profits they earned during the previous year to their shareholders in the current tax year for individuals.

Meanwhile, during periods of recession, it's not unusual for the first quarter data to be greater than the following quarter, as companies trim dividend payments in hard times, but the first quarter will normally be less than the preceding fourth quarter.

So 2011 is shaping up to be unique. We wouldn't say the current period of disorder in the stock market, and by extension, the private sector of the U.S. economy, is set to end anytime soon.

Labels: dividends

Suddenly, last Thursday, we discovered that we could see six months farther into the future!

What happened is that our preferred source for dividends future data finally began showing the expected level of dividend payments to be made between now and when the S&P 500 index futures contract for the second quarter of 2011 expires in June 2011.

Finally able to see past the end of 2010, the chart to the right shows what we found: the growth rate of the S&P 500's dividend per share is expected to begin decelerating through the first half of next year.

Finally able to see past the end of 2010, the chart to the right shows what we found: the growth rate of the S&P 500's dividend per share is expected to begin decelerating through the first half of next year.

We suspect that this deceleration, combined with the noise generated by the recent series of crises in the European bond market, is largely responsible for the recent declines in U.S. stock prices.

The additional data now allows us to better quantify how much of the market's recent decline is the result of the noise we see emanating from Europe versus how much is being driven by changes in the fundamental outlook for the companies that make up the S&P 500. In our chart, the effect of noise would be measured by the vertical difference between the expected change in the growth rate of dividends per share in June 2011 from the observed change in the growth rate of stock prices, through May 2010.

As a result, we're updating our previous forecast for the S&P 500 in June 2010. Given the futures data available for 14 June 2010 and assuming the approximate level of noise we've been observing in the last two months, we would expect the average of stock prices for the S&P 500 to fall in a range between 1074 and 1118 during this month. Our assumptions continue to be driven by the idea that the noise we observe in the market will continue until it stops, and as long as it appears to be stable, we can continue to treat that noise as if it were being driven by a fundamental change in the future outlook of investors.

Without the negative effect of Europe's debt-driven crises upon the U.S. stock market, and assuming a more typical level of noise in the market, we would instead expect to see stock prices in June 2010 range between 1212 and 1257.

There is one caveat to our assumptions. Since we now can't see past June 2011, which is just 12 months away, it is possible that investors are looking even farther forward to a point in time beyond that point, to a future quarter where we do not yet have dividend futures data. Given how stock prices are behaving, it could well be that investors are expecting changes in the the growth rate of the market's dividends per share to decline more sharply than the data we do have available now indicates.

So it's quite possible that there's less noise than would seem to be present in the market today, and that the decline in stock prices we've seen in the last two months is being driven by a worsening fundamental outlook for U.S. businesses in 2011.

We'll be able to tell if that's the case once we have dividend futures data available through December 2011.

Labels: dividends, forecasting, SP 500

Welcome to the Friday, June 11, 2010 edition of On the Moneyed Midways, where we review and present the best posts from the week's best money and business-related blog carnivals to provide your essential weekend reading material!

This week's top contribution from the Carnival of Debt Reduction wasn't the best post of the week, but it pointed to what we think might be the most potentially rewarding use of 18 minutes and 40 seconds of your time today - it's all about what works for motivating people to achieve greater things:

Now, who's ready to implement the ROWE strategy? Which oddly enough encapsulates our philosophy for why we produce each week's edition of OMM - we do it every Friday (and occasionally Saturday) so it's there where you're ready for it on your own schedule!

After all it's your time. We thank you for passing some of it with us and hope we've provided you something you find valuable.

Speaking of which, the best posts we found in the week that was await you below....

| On the Moneyed Midways for June 11, 2010 | |||

|---|---|---|---|

| Carnival | Post | Blog | Comments |

| Carnival of Debt Reduction | How the Candle Problem Can Help You Reduce Your Debt? | Debt-Tips.com | What is "the candle problem" and how might you use it to reduce your debt load? Kris Bickell points to the lessons that can be learned from Dan Pink's motivation video from TED to explain it all, which we liked so much we're featuring it above for your convenience! |

| Carnival of HR | Unemployed? Then Don't Even Bother Applying | bnet Personal Success | Suzanne Lucas, whom we best know as the Evil HR Lady, weighs in on the story of a company where the unemployed need not apply and how to exploit being unemployed to give you an advantage when seeking new work. |

| Carnival of Personal Finance | Dollar-Cost Averaging Takes the Stress Out of Investing | Foreigner's Finances | Austin Morgan argues that a dollar cost averaging investment strategy can do a lot to reduce your exposure to market volatility over time. |

| Carnival of Taxes | Ten Things I Don't Want to Pay Tax for Anymore | Monevator | The Investor goes on a rant about all the wasteful places taxpayer money goes in his native Britain. Absolutely essential reading!, because you know your own national government should be stopped from doing similar stupid things! |

| Best of Money | Don't Devalue Yourself | Budgets Are Sexy | Jess Michelsen guest posts about what you need to consider before you ask for what you're worth. The Best Post of the Week, Anywhere! |

| Carnival of Money Stories | How to Take Control of Your Finances the Manly Way | Good Financial Cents | Jeff Rose provides a venue for Greg Garland to tell the story of how he manned up to confront his personal debt situation. |

OMM's Running Index for 2010

Presented in reverse chronological order....

- On the Moneyed Midways - June 11, 2010

- On the Moneyed Midways - June 4, 2010

- On the Moneyed Midways - May 28, 2010

- On the Moneyed Midways - May 21, 2010

- On the Moneyed Midways - May 14, 2010

- On the Moneyed Midways - May 7, 2010

- On the Moneyed Midways - April 30, 2010

- On the Moneyed Midways - April 23, 2010

- On the Moneyed Midways - April 16, 2010

- On the Moneyed Midways - April 9, 2010

- On the Moneyed Midways - April 2, 2010

- On the Moneyed Midways - March 26, 2010

- On the Moneyed Midways - March 19, 2010

- On the Moneyed Midways - March 12, 2010

- On the Moneyed Midways - March 5, 2010

- On the Moneyed Midways - February 26, 2010

- On the Moneyed Midways - February 19, 2010

- On the Moneyed Midways - February 13, 2010

- On the Moneyed Midways - February 5, 2010

- On the Moneyed Midways - January 29, 2010

- On the Moneyed Midways - January 23, 2010

- On the Moneyed Midways - January 15, 2010

Older Editions

- OMM: The Best Posts of 2009 and our full index for the year!

- OMM's Running Index for 2008

- OMM's Running Index for 2007

- The Best Blogs Found in 2006 (and our full 2006 index)!

Labels: carnival

Welcome to the blogosphere's toolchest! Here, unlike other blogs dedicated to analyzing current events, we create easy-to-use, simple tools to do the math related to them so you can get in on the action too! If you would like to learn more about these tools, or if you would like to contribute ideas to develop for this blog, please e-mail us at:

ironman at politicalcalculations

Thanks in advance!

Closing values for previous trading day.

This site is primarily powered by:

CSS Validation

RSS Site Feed

JavaScript

The tools on this site are built using JavaScript. If you would like to learn more, one of the best free resources on the web is available at W3Schools.com.

Other Cool Resources

Blog Roll