Want to take a Rorschach test? We've extracted the following illustrations from U.S. Patent 6,612,440 - we'll tell you what it is below the image....

If you saw spectacles looking at a banana-shaped object, you're probably not alone. Or far off, because fortunately for your psychological health assessment, bananas are indeed involved....

What you're looking at is a section view (Figure 2) and an isometric view (Figure 3) of half of a "Banana Protection Device". Because, well, you must store and transport your bananas carefully - even when they've been sliced in half lengthwise. The patent abstract explains:

A banana protective device for storing and transporting a banana carefully. The banana protective device includes a container having a first cover member and a second cover member being hingedly attached to the first cover member and being adapted to store a banana therein; and also includes pad members being securely disposed upon the first and second cover members for protecting and cushioning the banana; and further includes fastening members being attached to the first and second cover members for fastenably closing the first and second cover members together.

No, we're not making this up. The patent really says that.

And at least now you have something to carefully store and transport the cheapest thing you can buy outside of the food court at Costco....

Other Stuff We Can't Believe Really Exists

- It's Not What You Think....

- Inventions in Everything: Soup Bowl Attraction

- Inventions in Everything: Making Life More Difficult

- Inventions in Everything: The Oreo Separator Machine

- Air Shark!

- Markets in Everything: Stormtrooper Motorcycle Suit

- The Bike That Rides You

- One Inventor's Stick-to-itiveness

- High Five!

- Inventions for Everything

- The Best Mousetrap Ever

- An Invention for the True Wine Connoisseur

- Three of Ten Things You Don't Need on St. Patrick's Day

- The Future Just Got a Lot Cooler Than It Used to Be

- The Worst Piece of Design Ever Done

- The Magic Marker of the Future

- Coming Soon, to a Gym Near You!

Labels: none really, technology

How has President Obama's view of the desirable level of federal government spending evolved since he came into office?

This is the flip side to our previous analysis of the government revenue forecasting ability of U.S. Presidents, in which we found that a President risks losing credibility for their economic initiatives when government revenues fail to match the forecasts they make in their annual budget proposals.

Fortunately for President Obama, his credibility isn't at risk of falling even lower with this aspect of the federal government budget. Instead, we will evaluate his judgment.

Unlike the situation with collecting revenue, where factors outside the U.S. government's control affect how much revenue it can actually collect, the federal government is fully capable of spending every single dollar it intends to spend. As a result, a President's budget proposal really represents their view of the appropriate level of spending needed to satisfy their political priorities.

Our chart below reveals how Presidential desires for federal spending have stacked up against reality for each the budget proposals made by both President Bush or President Obama for each of the U.S. government's fiscal year from 2004 through 2014 (FY2004 to FY2014).

Looking over President Bush's record, we find that the federal government's actual level of spending was often anywhere from $60 billion to $90 billion greater than the amount originally proposed by the President. This is largely the result of the U.S. Congress adding spending on top of the amounts proposed by the President. Generally speaking, this outcome suggests that President Bush's political priorities were largely agreed to by the U.S. Congress during his tenure in office.

By contrast, President Obama's spending proposals have always been considerably out of whack with respect to the general consensus within the United States for the appropriate level of federal government spending, which we can observe in the vertical separation between President Obama's desired level of spending and the actual amount of spending that has occurred during his time in office. Politically, we can observe just how out of whack President Obama's desires for spending have been in the near universal margins by which his budget proposals have been rejected in the U.S. Congress.

That however appears to have changed somewhat with his most recent budget proposal for Fiscal Year 2014, the first following his re-election, where President Obama would appear to have finally begun to rein in his ambition for higher spending to fund his political initiatives, as the amount of federal spending would appear to be anywhere from $100 to $200 billion more per year than what the U.S. government would have spent under an extended projection of President Bush's FY2007 budget proposal.

While the President's FY2014 budget proposal is anywhere from $100 billion to $300 billion less than what President Obama has previously proposed for the U.S. government to spend in any of his first-term budgets, it still runs a minimum of $475 billion above the President's historically non-credible forecasts for the federal government's revenue collections.

That's progress in evolving toward a more financially-sound budget, whose priorities are more in tune with those of the American people, but there is still a lot of room left for President Obama to continue his evolution in that direction.

Labels: forecasting, national debt

Yesterday was all abuzz as the just-released Case-Shiller index for March 2013 revealed that home prices in the U.S. had increased by 10.9 percent from their March 2012 level.

That, of course, is nearly two-month old news. Our first chart jumps a month forward in time to see where things stand through April 2013:

Here, the U.S. Census Bureau reports that median new home sale prices in the U.S. reached a preliminary record value of $271,600 in April 2013, with the 12-month trailing average of median new home sale prices reaching a preliminary record value of $250,633. We say these values are preliminary since they will be revised as additional data is recorded in the next several months. The recent trend has been for the data to be revised upward.

Meanwhile, Sentier Research indicates that median household income has reached a value of $51,546 in April 2013, up from the $51,320 that they previously reported for March 2013. Here, the 12-month trailing average of median household income in the U.S. is $51,301.

In the nine months since the second U.S. housing bubble began to inflate in July 2012, the median sale price of new homes in the United States has increased at an average rate of well over $22 for each $1 increase in median household income. The only period of time in modern American history that had a similar rate of price escalation was the original inflation phase of the first U.S. housing bubble.

Our second chart shows more of that history. The red-dashed line box in the upper right hand corner is detailed in our first chart:

Meanwhile, the staff of the Wall Street Journal is resisting the mere idea that a new bubble has begun to inflate in the U.S. housing market:

Recent increases in home prices have already ignited new talk of a housing bubble. Don’t believe it.

Some regions are seeing a surge of housing demand amid extremely low interest rates and investors searching for opportunities. And it is true that some regions are up more than 25% from their bottom. But as Dan Greenhaus of BTIG LLC points out, none of the 20 cities tracked by the Standard & Poor’s Case-Shiller home-price indexes is back to its peak level.

"Those previous peaks may not have been justified but they were and are largely seen as 'bubble levels,'" said Mr. Greenhaus. "Can home prices again be in a bubble and yet be 27% below their previous peak? Perhaps, but we don’t yet think so."

The median new home sales price data begs to differ, although the WSJ staff has suggested an alternative explanation for why they are ratcheting up so quickly.

Still, we find this line of thinking to be interesting, in that it indicates that they really believe that the greatly inflated prices of homes during the first U.S. housing bubble were really reasonable and that they could be supported indefinitely on the household incomes of U.S. homebuyers, if not for their bad luck!

From that perspective, it's just unfortunate that today's median new home sale prices are growing so much more quickly than the median household incomes earned by the kind of Americans who might want to buy and live in them.

Previously on Political Calculations

Our ongoing analysis of the development of the second U.S. housing bubble, presented in chronological order below!

- The U.S. Housing Bubble Is Back - we apply our groundbreaking analytical methods to determine that a new housing bubble has begun to inflate in the U.S. economy.

- Fuel, Oxidizer and a Spark - Part 1 - we revisit the origins of the first U.S. housing bubble and identify the factors that ignited it.

- Fuel, Oxidizer and a Spark - Part 2 - we explain why housing prices rose so much more in just four states than they did elsewhere.

- Fuel, Oxidizer and a Spark - Part 3 - we examine the factors that kept the first U.S. housing bubble going, even after the Fed acted to stop throwing so much fuel on the fire.

- Confirming the Second U.S. Housing Bubble - using revised data, we confirm that there is no apparent new-year slowdown in the inflation phase of the new U.S. housing bubble.

- The Second U.S. Housing Bubble Continues to Inflate - we extend our bubble analysis through March 2013!

- As the Housing Bubble Inflates: Month 9 - we mark the ninth month of the second U.S. housing bubble's existence!

Labels: real estate

How good is the President at predicting how much money the U.S. government will collect in revenue from year to year?

The answer to that question matters because when a U.S. President submits a budget proposal to the U.S. Congress, they are effectively putting the credibility of their economic programs on the line. If their revenue projections repeatedly fall short of what the government actually collects from year to year, it is an indication that either they are not in tune with the changing health of the U.S. economy or that their programs are not capable of promoting the kind of economic performance needed to generate the kind of revenue figures they anticipate. And quite possibly, both.

Let's take a closer look at the recent performance of U.S. Presidents. Our chart shows the amount of revenue forecast by President George W. Bush (dashed lines) and President Barack Obama (solid lines) for each of the U.S. government's fiscal years from 2004 through 2014 (FY2004 through FY2014).

In the chart above, the U.S. President's forecast for a given fiscal year is typically made in February of the previous year. For example, President Bush's budget proposal for FY2009 was released with its projection of the U.S. government's revenues through FY2013 in February 2008, nearly 8 months ahead of when the U.S. federal government's 2009 fiscal year began on 1 October 2008.

We note this particular revenue projection because it turned out to be considerably far off the target. Prior to 2008, President Bush's budget proposals had a high degree of credibility, as the federal government's revenues frequently came in at levels slightly higher than the President had forecast.

But in February 2008, President Bush's revenue projections for FY2009 and beyond failed to anticipate the financial system crisis that would take hold during the year, nor did it anticipate the record spike in oil prices that would subsequently lead to near collapse of the U.S. auto industry by the end of the year. Note the permanent fall in the number of Americans employed by the U.S. automotive industry in the following graph (shown in orange on the scale on the right hand side of the chart):

Consequently, in missing the deteriorating health of the U.S. economy during 2008, President Bush's economic agenda quickly lost its credibility during that year, even though it would have appeared to have been successful in the preceding years.

Meanwhile, President Obama's track record of revenue forecasts indicate that his administration has never had a good handle on accurately assessing the health of the U.S. economy, nor has his economic initiatives been successful in stimulating the kind of economic activity needed to meet his revenue projections.

We can see this outcome in our chart above by comparing President Obama's revenue forecasts with the heavy black line in our chart above indicating the U.S. government's actual revenue collections. Here, we find that President Obama's forecast revenues are almost always far more optimistic than the actual outcome. Much as President Obama's unemployment rate forecasts have been.

We can also see President Obama's forecast economic recovery following the 2008-2009 recession progressively get dragged out longer and longer with each year's forecast in our chart. Here, it appears that President Obama has taken a simple straight-line projection of President Bush's revenue projections from the FY2007 budget proposal as his idea of how much revenue the federal government would collect if the U.S. economy were to fully recover from the recession. This straight-line projection then sets the bar for determining how effective President Obama's economic growth programs have been by his own selected standard.

We should note that President Obama has set the bar at a very high level, as the revenue forecasts for President Bush's FY2007 budget proposal was issued in February 2006, just after the peak of the first U.S. housing bubble, in which government revenues were elevated over what they would be in more typical circumstances.

Still, it is clear that this is the standard that President Obama has selected to assess his own economic performance in office. With that being the case, it is also clear that President Obama's economic programs as presented in his annual budget proposals have repeatedly fallen far short of meeting their anticipated performance targets.

We therefore find that President Obama's economic agenda has never had much credibility, especially when measured against the President's chosen measure of success. Which is perhaps why each of his most recent budget proposals have been dead on arrival on Capitol Hill, as no U.S. Congress has acted to pass any of President Obama's proposed budget measures since 2009, whether the national legislature was fully controlled by the President's own political party, as in 2010, or not.

And that is perhaps the best indication that waiting for President Obama's economic recovery is a lot like waiting for a train that will never come.

The lyrics to the Matchbox 20 song by that name are here. They would seem to fit the political situation with President Obama's economic agenda fairly well.

Labels: forecasting, gdp forecast

What are the three cheapest things you can buy outside of the food court at Costco?

After we unexpectedly found we had way too much free time on our hands one day last week, which we found we could spend in one of the wholesale retailer's urban locations, we set out to answer that question. We went up and down all the aisles, seeking to find the bulk or bundled item that would ring up the lowest bill at the checkout.

We won't keep you in suspense. The lowest-priced item you can buy at Costco is bananas.

We won't keep you in suspense. The lowest-priced item you can buy at Costco is bananas.

We found we could walk out of Costco with 3 pounds of bananas for $1.39. Which is not only less expensive, but also a lot more food than the hot dog and soda combination we could have bought for $1.50 at Costco's food court!

The second-lowest priced item we found was salt. Specifically, it was a bundled package of four 1-pound containers of granulated table salt, which could have been ours for just $2.15.

The second-lowest priced item we found was salt. Specifically, it was a bundled package of four 1-pound containers of granulated table salt, which could have been ours for just $2.15.

But we didn't stop there. The second-runner up, and third-place finisher, in our quest to find Costco's lowest-priced items is a tie between a 24-pack of hot dog buns and a 24-pack of hamburger buns, both of which could be had for $2.29.

For fun, let's say that a Costco shopper's meals consisted solely of the three cheapest items one can buy at Costco. And for real fun, let's say that they are connoisseurs of the culinary delicacy of salted bananas served in hot dog buns.

For fun, let's say that a Costco shopper's meals consisted solely of the three cheapest items one can buy at Costco. And for real fun, let's say that they are connoisseurs of the culinary delicacy of salted bananas served in hot dog buns.

Some quick math suggests that their worst case grocery bill from a single shopping trip at the wholesaler would total just $7.22, which would include the four-pound package of salt, one 24-pack of hot dog buns and two bundled packages of bananas. Here, we assume that there are four medium-sized bananas per pound, so our two 3-pound bundles would provide 24 bananas, enough to fill each of the hot dog buns, thus minimizing any potential waste for the grocery items that might spoil, as the salt would have an indefinite shelf life.

Of course, none of these prices include any portion of the $55 annual membership fee that Costco charges its customers as the minimum for being able to buy these bulk and bundled items at such low, low prices, which is a way of helping cover its transaction costs for selling these low-margin, low-unit price products.

Labels: personal finance

Following our Seeking Alpha commenter rant today, it turns out that once again, we're right. Again.

Here's the evidence, in which we take into account the Japanese Black Thursday stock market crash. Our chart below assumes that if the S&P 500 will indeed fall 18.30 points today, as the pre-market open stock price futures for the day currently indicate. Pay close attention to where the daily stock prices (dotted line) and the 20-day moving average (black line) converge:

Why, it's almost as if we anticipated this would happen, absent some action by the Fed....

We've had some fun over the past few days in forcing Seeking Alpha's editors to rewrite portions of our posts to remove our assessment of the intellectual quality of commentary provided by several of that site's more confused commenters to our posts so their feelings wouldn't be hurt, but today, we're just going to rub their faces in it.

Consider this comment from one commenter, who was troubled by one particular passage in a recent article:

You are correct, ironman: "this confuses some Seeking Alpha's commenters"

In fact, I dare anyone to explain "We can observe this transition directly in our chart below as the movement of the daily and 20-day moving average of the change in the rate of growth of stock prices from the red line representing 2013-Q2 to the green line representing 2014-Q1, which corresponds to the change in the year-over-year rates of growth of the trailing year dividends per share expected for each of these quarters."

I'm not saying the article is wrong, just that it's incomprehensible.

What this particularly confused Seeking Alpha commenter found troubling is our verbal description of a chart we provided, in which a black line changes its relative position from keeping pace with a red line to instead converge and begin to keep pace with a green line. As noted on the chart, the black line corresponds to the change in the rate of growth of stock prices, while the red and green lines correspond to the change in the rate of growth of dividends expected for two different quarters in the future.

So it's not like we didn't provide a decoder. It's more that it was ignored....

That was one of the more intelligent comments we saw. Later in the comments thread, we came across this gem from another commenter, who at least recognizes their naivety:

Call me naive, but how do you know investors have shifted their focus from 2nd quarter's dividend rates... to expectations for 1st quarter 2014 dividend rates?

Is this standard knowledge?

Or is it in that first chart that shows dividends moving average compared to stock prices? If so, I see the break upward of stock prices. I don't see anything that correlates or gives a hint that it's a shift in focus by investors to next year's dividend rates.

How do we know? Other than seeing that black line shift from pacing the red line, representing 2013-Q2's dividend rates, to pace the green line instead, representing 2014-Q1's dividend rates? Or any of our previous articles in which we've discussed this quantum-like characteristic of stock prices that are being driven by expected future dividends?

As for being standard knowledge, well, apparently not among Seeking's Alpha's more confused commenters....

But the best was yet to come! Behold the most cortically-subilluminated comment we've seen to date!

Total bafflegab and gobbledygook. As an investor I have not shifted my focus as the author suggests. I am not clairvoyant, but I doubt most investors have, as the author claims. Plus, his insult of commenters to a previous article of his/hers suggest personal insecurity. Author, are you here to educate or to build ego?

For some reason, you are ranked 1 in real estate. Not sure what it means, but it suggests some sort of weakness in SA's rankings. Especially since you have a grand total of 273 followers.

To paraphrase you, it looks like investors have shifted their focus to better authors and empirically supported charts. Best wishes, however.

Thanks to the efforts of Seeking Alpha's intrepid editors, that's a commenter who really had to work hard to get their feelings hurt, as the claimed insult appears nowhere in our articles appearing on Seeking Alpha!

Speaking of which, our articles appear on Seeking Alpha because Seeking Alpha's editors like them and requested permission to re-post them. Since we post anonymously, it's pretty clear that we don't exactly care about ego, and since we're not compensated by Seeking Alpha at all, much less to educate its site visitors, we're not that concerned about fulfilling that function either.

As for being "ranked 1 in real estate" on Seeking Alpha, how cool is that?! Especially since we've only written a handful of articles on real estate in the past year, all in recent months, which means that we've had some sort of impact in generating a migration to better authors and empirically supported charts for that particular topic at Seeking Alpha. Thanks for letting us know - we'd say it's pretty ego-boosting, but then, we still don't care!

Other criticism in Seeking Alpha's comments to our article there was equally off base. Consider this sample:

There has been no mention of a possibility of a correction, market has been on a short term rally since Oct'Nov 2012 and this also must be accounted, so there is a possible correction when buyers through this last rally begin taking profits and fooled people that bought late are screwed.

Hmm. Somehow, this commenter completely missed this quote of ours from our article that appeared at Seeking Alpha on Monday, 20 May 2013:

Now that the pace of acceleration of daily stock prices has risen above the green line on our chart above, we can expect the recent rate of growth to taper off, and even to fall following this period of transition, as there is no fundamental support for stock prices to remain significantly above this level for any sustained period of time, absent some action by the Fed.

Guess what happened on Wednesday, 22 May 2013, around 2:00 PM, after the Fed released minutes of its recent meeting in which the Fed decided that they would not increase their purchases of Treasuries and Mortgage-Backed Securities as part of their current quantitative easing program and would instead continue purchasing them at their current levels....

You have to admit - we were right. Again!

But will the Seeking Alpha commenters who wrote the following be bitter about it? You decide - here's the first comment by a Seeking Alpha commenter who was concerned that someone might base their investments on things we write:

I'm not saying the article is wrong either. It is based on some airy fairy ideation couched as fact. I agree that it is incomprehensible. I am glad it is, for if it made any sense, some poor sucker might base investments based on it. Bleh.

And a second comment on the same vein, where the Seeking Alpha commenter also doubts our ability to anticipate future changes in stock prices:

Unfortunately the article appears to be an prima facie example of the logical fallacy that correlation equals causation. A lot of effort (and reader time) could have saved by just sticking with tea leaves.

Checking the score, that would be one poor sucker doing better than these two particular Seeking Alpha commenters! Except that sucker wouldn't be as poor as these particular Seeking Alpha commenters, even though one appears to count tea leaves among their assets.

There were more comments, but fortunately for our reading experience, they were much more intelligent than the ones we covered in this article today. We'll close by sharing the most honest observation, which we respect:

I am reading a book about cosmology that is easier to understand.

More Seeking Alpha commenters should recognize their cognitive limits. It's not that you're as dim-witted as the above examples suggest, it's more that you don't know what you need to understand to deal with it and aside from this week's break, we're not going to slow down or stop what we're doing to get you up to speed. Just ask a mathematician about Mochizuki's proof of the ABC Conjecture and recognize that you're in the same boat. Fortunately for you however, we've done all our intermediary work live, in real time, online, so you can simply go through our archives to see how we've gotten so far ahead of you.

Yo, Mochizuki! Try this with your guys - it's therapeutic!

Labels: none really

We thought it might be fun to look at the recent trends in the S&P 500 at several different scales. Our first chart shows the current major trend for the S&P 500 index fits in with respect to the average monthly value of stock prices and trailing year dividends per share recorded since December 1991:

Note that at this scale, we're tracking the average monthly index value for the S&P 500, which we find by taking the average of the daily closing values for the S&P 500 index in each calendar month, which allows us to tie into Robert Shiller's and the Cowles Commission's historic data for U.S. stock prices.

Let's focus next upon the current major trend in stock prices, which we've marked on the chart above in the red dashed-line box in the upper right corner. Our second chart shows this data in much greater detail:

Here, we're showing the S&P 500's daily closing prices along with the 20-day moving average for the index' value, which roughly corresponds to the calendar-month based data we presented on our first chart. While this confuses the more dim-witted among Seeking Alpha's commenters, it works fairly well for our purposes because most months contain at least 20 trading days.

This brings up a good question: how do we define a trend? For our purposes, a trend is defined by a power-law relationship between stock prices and trailing year dividends per share. We consider a trend to be orderly when both dividends per share and stock prices are generally increasing in value over time, in such a way that we cannot rule out that the variation in stock prices with respect to the mean trend curve are normally distributed with a statistical hypothesis test. We consider stock prices to be behaving chaotically whenever that basic relationship is not present.

We'll next focus on the most recent microtrend for the S&P 500, which we've indicated in our second chart with the purple dashed-line box in the upper right hand corner. Our third chart focuses on this zone:

In this final chart, we see the fiscal-cliff tax avoidance rally that began on 15 November 2012, which marked the beginning of the period in which publicly-traded companies raided the funds being set aside to pay out dividends in 2013 to instead pay them out in 2012 for the purpose of avoiding the potential tripling of dividend tax rates in the U.S. for their most influential investors. This portion of the rally ended as these investors sold off stocks just before the end of the year to claim capital gains on them before those tax rates would rise as well.

The next portion of the microtrend rally kicked in with the fiscal cliff tax deal shortly afterward on 3 January 2013, which set the maximum tax rate for both dividends and capital gains at 23.8%. Since the fiscal cliff tax deal also hiked the U.S.' top income tax rates up to a maximum of 43.8%, influential investors once again sought to have publicly-traded companies boost their dividends as a means to avoid the higher federal taxes on the wage and salary income they also earn from the companies they own, taking more of their compensation in the form of dividends instead.

And because that change in the structure of compensation for influential investors would also increase the dividend income earned by regular investors, owning stocks has become relatively more attractive, with stock prices continuing to rise in response.

That portion of the recent microtrend ended in late April 2013 following the major announcements made during 2013-Q2's earnings season. Since then, other fundamental factors have contributed to a shift in the quantum level of stock prices, but then, that sort of thing really confuses the cortically-subilluminated among Seeking Alpha's commenters, so we'll just point you backward in time, again, for that remedial discussion....

You know, it occurs to us that if those commenters would just bother to follow the links we provide, they wouldn't keep embarrassing themselves so badly....

Labels: data visualization, SP 500

Since we last looked at the S&P 500's expected trailing twelve-month earnings per share some three months ago, the future for the S&P 500's forecast earnings has become considerably brighter going forward. Which is good, because it also suggests that the U.S. economy went through a recessionary period in the second half of 2012, from which investors are now expecting a recovery.

We can see that's the case in comparing our 15 February 2013 snapshot of the S&P 500's expected trailing year dividends per share for the fourth quarter of 2013 (2013-Q4, ending 31 December 2013) with our new snapshot just taken on 17 May 2013:

Here, for 2013-Q4, we see that investors have increased the level of earnings they expect to be reported for the S&P 500 in 2013 by $7.47 per share from our previous snapshot taken just over three months ago, with the new trailing twelve month figure now expected to be $108.18 per share.

This is close to the level that investors had first expected for 2013-Q4 back on 17 January 2012. But then, back in those heady days, they also expected that the earnings for the S&P 500 in 2012 would be $12.80 per share better than the $86.51 per share that they actually turned out to be. (Note: Standard and Poor may continue to revise its earnings estimate for 2012 for some time still as more refined information becomes available and as companies might restate their previously reported earnings.)

Looking at the full range of values that investors have forecast for the S&P 500's trailing year earnings for 2012, we see that they have ranged from a high of $100.07 per share, which was recorded back on 20 May 2012, to a low of $86.51 per share, as currently estimated. The low value of $86.51 per share also would appear to mark the bottom of an earnings recession for the index.

So why didn't stock prices crash at the same time? Well, as we keep pointing out, earnings don't drive stock prices. Dividends do. And although this confuses many of the more dim-witted commenters at Seeking Alpha, the changes that have taken place in dividends since mid-November 2012 are almost entirely responsible for the rally in stock prices since that time. Or at least up to nearly the end of April 2013, after which the story changes.

But we don't expect that certain people will appreciate that we've already told that story, and don't feel compelled to dumb it down for their benefit....

Reference

Silverblatt, Howard. S&P Indices Market Attribute Series. S&P 500 Monthly Performance Data. S&P 500 Earnings and Estimate Report. [Excel Spreadsheet]. Last Updated 9 May 2013. Accessed 17 May 2013.

Labels: earnings, forecasting, SP 500

You have to admit - we were right. Last week was indeed a big week for the S&P 500!

From Monday, 13 May 2013 to Friday, 17 May 2013, the S&P 500 rose by nearly 2%, or 32.35 points, from 1630.77 to a new record high of 1666.12. Over half the gain for the week came on Friday, 17 May 2013, as the S&P 500 rocketed up by 17 points.

In doing that, the S&P 500 completed the transition it began on 1 May 2013, as investors shifted their forward-looking focus from the second quarter of 2013 to the first quarter of 2014 in setting their expectations for the sustainable portion of future earnings growth for the stock market (a.k.a. "future dividend growth".) We can observe this transition directly in our chart below as the movement of the daily and 20-day moving average of the change in the rate of growth of stock prices from the red line representing 2013-Q2 to the green line representing 2014-Q1, which correspond to the change in the year-over-year rates of growth of the trailing year dividends per share expected for each of these quarters.

Now, even though this confuses the more dim-witted among Seeking Alpha's commenters, this latest transition of investor forward-looking focus from 2013-Q2 to 2014-Q4 follows very similar transitions that have taken place periodically since the end of the Federal Reserve's QE 2.0 program at the end of June 2011. Following the deflation of that mini-bubble in the weeks that followed, stock prices have since been very fundamentally-driven with little noisy exception, with the pace of acceleration of stock prices matching up with the changes in the growth rates of trailing year dividends per share for discrete future quarters.

The transitions of investor forward-looking focus from one future quarter to another, combined with changes in the growth rate of dividends expected in quarters where investors have focused their attention, accounts for nearly all but a small portion of the changes in stock prices that have occurred in the post-QE 2.0 period.

These periods of transition in forward-looking focus also mark the greatest uncertainty we have in anticipating the direction and change of stock prices over time, outside of significant noise events such as the Federal Reserve's quantitative easing programs marking major changes in their acquisition rates of U.S. Treasuries. That was definitely the case with QE 2.0, when the Fed ramped up then discontinued an interest-rate lowering bond-buying program, which resulted in the mini-bubble for stock prices.

However, that has not been the case with QE 3.0, where the Fed ramped up only its purchases of Mortgage Backed Securities in September 2012, or for QE 4.0, which began in December 2012, where the Fed maintained its ongoing acquisition rate of U.S. Treasuries that it set in its "Operation Twist", but stopped selling off an equal value of holdings that was the other part of that operation. The lack of change in the Fed's basic acquisition rate of U.S. Treasuries for both QE 3.0 and QE 4.0 is why these latest quantitative easing programs have had no significant impact upon stock prices.

Now that the pace of acceleration of daily stock prices has risen above the green line on our chart above, we can expect the recent rate of growth to taper off, and even to fall following this period of transition, as there is no fundamental support for stock prices to remain significantly above this level for any sustained period of time, absent some action by the Fed.

That brings us to this week, where a lot of focus will be upon the pronouncements of the Federal Reserve. At present, there are a number of indications of recessionary conditions being present in the U.S. economy, which the Fed might attempt to offset by amping up its purchases of U.S. Treasuries. The market's response to such a noise event would be the only reason for the latest rally in stock prices to continue at their current rapid pace of escalation, as the earnings season for the second quarter of 2012 is nearly over, leaving little time left for corporate earnings announcements and changes in dividend policies to affect stock prices.

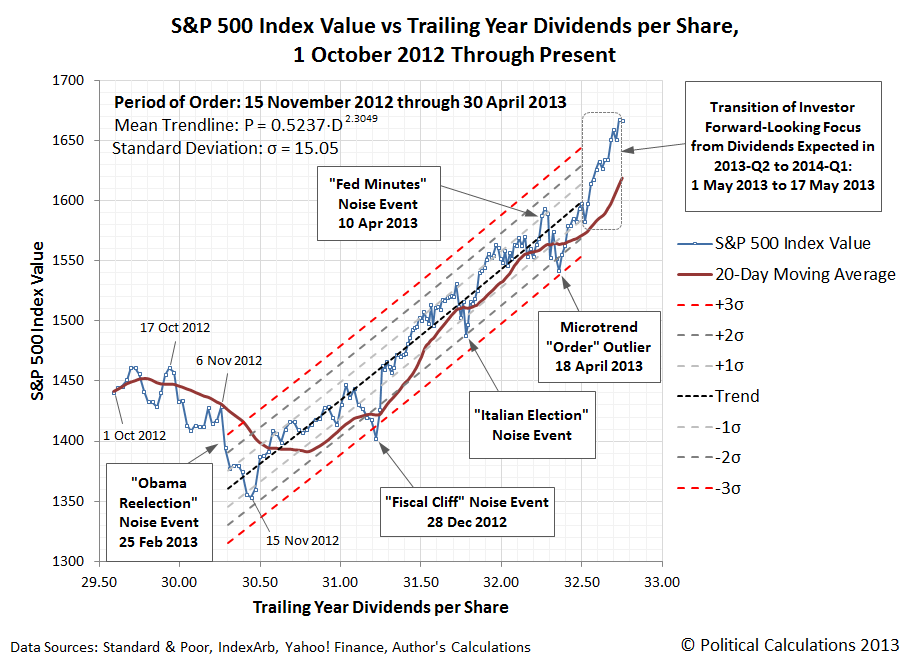

Speaking of which let's take a closer look at that microtrend rally. Our following chart shows the upward rise of stock prices since 15 November 2013, nearly one month before the Fed began its QE 4.0 program, with respect to the S&P 500's trailing year dividends per share:

We mark the beginning of the newest microtrend rally in stock prices from 1 May 2013, which coincides with the divergence of stock prices from the level that is defined by the dividends that are expected to be paid by the end of 2013-Q2. The new microtrend rally is characterized by an even more rapid escalation rate for stock prices than seen in the period from 15 November through 30 April 2013, which is also something that we associate with transition periods in where investors set their forward-looking expectations.

We'll take a closer look at the longer trend in stock prices later this week....

Labels: chaos, dividends, SP 500

Late in 2011, after realizing that Spain had run up an exceptionally large budget deficit for the year, exceeding 8.5% of the nation's entire GDP, the newly elected government of Mariano Rajoy set out to get Spain's fiscal situation under control.

To do that, Rajoy committed Spain to a program of spending cuts and tax hikes in 2012, as demanded by the European Commission (EC). A program that appears to have only succeeded in crashing Spain's troubled economy in 2012. (Refresh the image below to see Spain's quarterly GDP growth rates from 2010 through the end of 2012.)

Source: tradingeconomics.com

But which aspect of Rajoy's austerity program is most responsible for sinking Spain's fortunes? Was it the spending cuts? Or was it the tax rate hikes?

Believe it or not, we can answer that question! And to do it, we'll use data from the United States for its fiscal multipliers!

What's a fiscal multiplier, you ask? A fiscal multiplier is a ratio that tells us how much a nation's income, or GDP, is affected by changes in its government's spending or taxation policies. They are typically used by economists to predict how much more or less economic activity there will be in an economy as a result of a change in the levels of government spending or taxation.

What's a fiscal multiplier, you ask? A fiscal multiplier is a ratio that tells us how much a nation's income, or GDP, is affected by changes in its government's spending or taxation policies. They are typically used by economists to predict how much more or less economic activity there will be in an economy as a result of a change in the levels of government spending or taxation.

That's where the data from the U.S. comes into play, because we'll use the fiscal multipliers that have been calculated for both government spending and for taxes to apply to Spain's situation in 2012 to see if we can predict how much Spain's GDP was affected by the different parts of its so-called austerity program.

Let's start with the government spending multiplier. Research published by the Federal Reserve in January 2013 finds that the fiscal multiplier for government spending is somewhere between +0.6 and +0.7, which applies when unemployment rates are high (above 7.5%).

Here, having a fiscal multiplier with a value of less than 1 means that changes in government spending have a muted impact on a nation's GDP. For a fiscal multiplier of 0.6 to 0.7, if government spending were increased by 1 billion dollars, the nation's GDP would only rise by somewhere between 600 to 700 million dollars. Likewise, if government spending were cut by $1 billion, GDP would only fall by $600-$700 million.

By contrast, the tax multiplier has a much greater impact on GDP. Here, Christina Romer and David Romer (Christina Romer was formerly the chair of President Obama's Council of Economic Advisers, which is oddly omitted from her official academic biography) have found that the fiscal multiplier that applies for taxes is approximately -3.0, which as you notice, is both rather large in magnitude and negative.

What being large in magnitude means is that changes in tax levels will have an outsized effect upon GDP. What being negative means is that is changes in a nation's tax policy have an opposite effect upon its GDP. So, for example, if a nation were to cut its taxes by 1 billion dollars, it could expect to see its GDP grow by 3 billion dollars. Conversely, if a nation were to hike its taxes by $1 billion, it would expect to see its GDP fall by $3 billion.

Now let's apply these multipliers to Spain's situation in 2012. Starting with the spending cuts, we find in using data from Eurostat along with GDP reported in the World Economic Outlook for 2013 that Spain's spending was $668.8 billion (in terms of U.S. dollars) in 2011 and $635.5 billion in 2012, as Spain cut its spending from the previous year by $33.3 billion.

The tax data is more difficult to come by, because here, we must use the estimated amounts by which Spain's government expected to increase its revenue by increasing its tax rates and through other means. We do this because while a nation has full control over how much it spends, there is no guarantee that it will actually be able to collect as much revenue as it expects or plans, especially as those being taxed often make adjustments to avoid the full burden of new or higher taxes being imposed upon them.

The tax data is more difficult to come by, because here, we must use the estimated amounts by which Spain's government expected to increase its revenue by increasing its tax rates and through other means. We do this because while a nation has full control over how much it spends, there is no guarantee that it will actually be able to collect as much revenue as it expects or plans, especially as those being taxed often make adjustments to avoid the full burden of new or higher taxes being imposed upon them.

Early in 2012, the Rajoy government imposed higher taxes on both wage and salary income as well as investment income, expecting to increase its tax collections by 4.3% over the $528.2 billion USD it collected in 2011, or rather, by approximately $22.71 billion USD. In addition, the Rajoy government also planned to crack down on Spain's tax evaders, expecting to collect an additional 8.2 billion euros ($10.67 billion USD) through their increased enforcement measures.

However, by September 2012, it was clear that these measures would not be sufficient to close Spain's budget gap as much as the European Commission demanded. As the EC threatened to end its bailout of the Spanish government as Spain's debt crisis escalated, Rajoy's government finally consented to also increase Spain's value added tax rate, which took effect after September. This measure was expected to increase Spain's tax collections by an annual amount of 7.5 billion euros ($9.8 billion USD), but for our purposes, this tax increase only applied in the final quarter of 2012, so the expected additional tax collections from this source in 2012 is one-fourth that amount, or $2.45 billion USD.

Adding all those government revenue increasing amounts that apply for 2012 together gives us a total of $35.82 billion, for which the tax multiplier of -3 will apply.

We'll take these values and enter them in our tool below, which will do the fiscal multiplier math!

In the tool above, we used the lower end of the range of possible values that would apply for the government spending multiplier in obtaining the result using our default data of a GDP decline of $127.5 billion for Spain, which would be predicted using the Spanish government's actual level of spending cuts and our static analysis-produced expected increase in Spain's revenues from the government's tax-hiking frenzy in 2012.

The actual value that Spain's GDP fell in 2012 from 2011's level was $127.5 billion. The fiscal multipliers that seem to apply in the United States would therefore appear to be very effective in predicting how much other nation's GDPs might change in response to changes in their government's fiscal policies.

The actual value that Spain's GDP fell in 2012 from 2011's level was $127.5 billion. The fiscal multipliers that seem to apply in the United States would therefore appear to be very effective in predicting how much other nation's GDPs might change in response to changes in their government's fiscal policies.

We should note at this point that these figures are likely to be revised in the future, which means that the actual fiscal multipliers that apply in Spain may need to be tweaked from this preliminary analysis. Which is, of course, why we made it very easy to alter them in our tool above!

Consequently, we find that the Spanish government's attempt to increase its revenues, driven by the EC's demands to impose higher taxes on Spanish businesses and high income-earning individuals, is responsible for about 84% of the nation's decline in GDP, while its spending cuts were only responsible for 16% of the decline in Spain's national income from 2011 to 2012.

And that is a prime example of austerity done wrong.

References

Knoema. World Economic Outlook, April 2013. [Online Database]. Accessed 15 May 2013.

Knoema. World Economic Outlook, April 2013. GDP per Capita - Spain. Accessed 15 May 2013.

Knoema. World Economic Outlook, April 2013. GDP - Spain. Accessed 15 May 2013.

Eurostat. Government Finance Statistics. [Online Database]. Accessed 15 May 2013.

Owyang, Michael T., Ramey, Valerie A. and Zubairy, Sarah. Are Government Spending Multipliers Greater During Periods of Slack? Evidence from 20th Century Historical Data. [PDF Document]. Federal Reserve Bank of St. Louis, Economic Research Division. Working Paper 2013-004A. January 2013.

Romer, Christina and Romer, David. The Macroeconomic Effects of Tax Changes: Estimates Based on a New Measure of Fiscal Shocks. [PDF document]. March 2007.

LibreMercado. The government shuffle a new tax increase to reduce the deficit. [Google Translation]. 20 August 2012.

EuroNews. Spanish VAT Rise: A Backward Plunge. 6 September 2012. Accessed 15 May 2013.

Angloinfo. Tax Rises in Spain for 2012. January 2012. Accessed 15 May 2013.

Image Credits

Trading Economics. Spain GDP Growth Rates. Accessed 16 May 2013.

Ryan, Rebecca. The Multiplier Effect of Local Investing. Lion Investing. 20 February 2011.

Ammons, David. Income tax on high-wage earners? WA Secretary of State Blogs: From Our Corner. 21 April 2010.

Ammons, David. House D Budget: Cuts, delays, but no sales tax hike. WA Secretary of State Blogs: From Our Corner. 21 February 2012.

Labels: economics, taxes, tool

In 2012, after Spain's government had run up an extraordinary budget deficit in the previous year, the newly elected government of Spain's new prime minister, Mariano Rajoy, committed to both increase the government's revenue and to decrease its spending to put the Spain on a more sound financial footing. Those changes had been demanded by the European Central Bank as a requirement for its continuing to lend money to bail out Spain's fiscally distressed government, which had been put at risk by its bailout of that nation's banks following the collapse of the Spanish housing bubble.

To help put Spain's fiscal situation going into 2012 into context, we're presenting an updated version of the chart we first featured nearly a year ago when we first examined how Spain arrived at that state. The chart shows the relationship between Spain's GDP per capita and its annual government tax collections and expenditures per capita for each year from 2000 through 2011:

Today, we're going to focus on the revenue side of what happened in Spain in 2012, using data just published within the past month. Starting with Spain's 2012 GDP per capita of $29,288.70 (in terms of U.S. dollars), let's first see how much the Spanish government could have hoped to collect in revenue for that level of GDP if they had kept the same tax rates as Spain had from 2000 through 2011:

Using our tool with Spain's data, we find that if Spain made no changes in its tax rates, the Spanish government could have expected to collect the equivalent of $10,556.48 USD per capita, given its actual 2012 GDP per capita figure. We'll revisit this estimate, based upon Spain's non-economic bubble-related government revenue figures from 2000 to 2003 and 2009 through 2011, shortly....

Now, let's consider just what Spain did with its tax rates in 2012. The Wall Street Journal's Real Time Brussels blog reports:

Soon after it took office, the new government of Prime Minister Mariano Rajoy raised income taxes to curb a swelling budget deficit. We have written before that the by-now conventional wisdom, supported by the International Monetary Fund and others, is that cutting government spending is a more effective way to squeeze budget deficits than raising taxes. Mr. Rajoy's right-leaning government nonetheless chose to raise taxes "temporarily," apparently because it was viewed as socially more equitable than the alternatives.

The tax increases, write Spanish economists Juan Ramón Rallo, Ángel Martín Oro and Adrià Pérez Martí in a paper published today for the free-market Cato Institute, have left Spaniards paying among the highest income tax rates in Europe.

Our second chart shows how Spain's individual income tax rates changed from 2011 to 2012, which should result in increasing the nation's tax collections by anywhere from 3.0% to 13.5%, depending upon income bracket, where high income earners face much more dramatic tax hikes:

In addition, Spain also increased its tax rates on investment income from 19% to 21% (for investment income under 6,000 Euros), and from 21% to either 25% or 27%, with the higher rate applying on investment income greater than 24,000 Euros). These taxes should have increased the Spanish government's revenue from taxes on investment income by anywhere from 9.5% to 22.2%.

Later in 2012, Spain also implemented a surprise rate hike in its value-added tax, from 18% to 21%, which would be sufficient increase the government's take from this source of revenue by 16.7%.

So the range of increases in the government's revenue from these various taxes runs from 3.0% to 22.2%, with the actual net increase in the government's tax collections then depending largely upon the distribution of income in Spain. As you can see from the very progressive nature of most of these tax hikes, the government of Mariano Rajoy went very much out of its way to impose higher taxes on high income earning individuals as part of the "tax the rich" portion of its deficit reduction strategy. And in fact, the Rajoy government predicted that it would collect 4.3% more revenue than the Spanish government collected in 2011.

That 4.3% increase over its 2011 collections would have given Spain an expected tax revenue of $11,943.94 USD per capita for 2012.

Our final chart reveals how 2012 actually played out for those expectations:

In 2012, Spain's government revenue per capita was actually $10,661.09 USD. Only $104.61 more per person than our estimate of what would be reasonably expected if Spain had not hiked its taxes at all given how Spain's economy performed during the year.

Given the magnitude of the tax hikes that Spain targeted to most affect the country's highest income earners, what this outcome demonstrates is Hauser's Law at work in Spain. Once a government has maximized its revenue collecting capability, it is unable to change how much it collects by imposing higher and higher tax rates on its highest income earning citizens, who generally respond to the increased tax burden placed upon them by no longer generating the same economic activity they did when they were subject to lower tax rates.

That has major consequences, as these individuals are the most capable of generating the kind of economic activity that grows a nation's GDP. Without any ability to affect the European Union's monetary policy to offset the negative effects of Spain's contractionary fiscal policy, Spain paid a very large price to learn that lesson the hard way, as the country became a highly undesirable place to invest time, effort or money for its most productive residents and businesses. Consequently, Spain's economy has crashed to the point where it might reasonably be considered to be in a full economic depression in 2012, which is where it still stands today.

All in all, a pretty clear example of austerity done wrong.

Previously on Political Calculations

- The Greek Budget Identity (2012)

- Spain: A Very Different Fiscal Crisis (2012)

- President Obama's Unsustainable Fiscal Path (2012)

- Austerity, Done Right, Part 1 (2012)

- Austerity, Done Right, Part 2 (2012)

- Hauser's Law (2009)

- Is Hauser's Law Still Valid? (2011)

- Taxes at the Margin (2012)

- Hauser's Law at Work Today (2012)

Labels: economics, taxes, tool

And then, suddenly, the future for the S&P 500 snapped into clear focus:

It would appear that investors have shifted their forward-looking focus to 2014-Q1 in setting the pace of change for U.S. stock prices. Following the period after the fiscal cliff reaction of 15 November through 20 December 2012, they had been focused mainly on 2013-Q2.

Now that the transition in focus from 2013-Q2 to 2014-Q1 seems assured, we can expect the recent rapid run-up of stock prices to taper off, as the change in the growth rate of stock prices will converge with that expected for the S&P 500's dividends per share in 2014-Q1. Since that pace is positive, we can expect stock prices to continue generally rising, although at a slower pace.

However, anything that might shift the focus of investors to the less distant future quarters of 2013-Q3 or Q4 will send stock prices crashing.

Other factors that might cause the acceleration rate of stock prices to deviate from the 2014-Q1's expected trailing year dividends per share are the Fed's quantitative easing (QE) policies, where the Fed has recently indicated it could amp up its purchases of U.S. Treasuries or could begin tapering them off altogether. Beyond that, random noise events could temporarily send stock prices off track.

From our perspective, perhaps the most surprising thing about the rally in the stock market since 15 November 2012 is that it has been extremely driven by underlying fundamentals. The one thing that ended the recent uncertainty we had in which alternate future investors would select to focus their forward-looking attention upon was the sudden decline in the 2014-Q1's expected dividends per share, which dropped from $9.37 per share to $9.11 per share on Monday, 13 May 2013 - coinciding with the end of the period for establishing the shareholders of record for the biggest two stocks in the S&P 500, Apple and Exxon Mobil.

That change brought the level of the change for the growth rate of expected trailing year dividends per share into easy reach for today's stock prices. With that being the case, they are more likely to be able to hold that level outside changes in the Fed's QE policies, which if the Fed is targeting stock prices as it has in the past, means that they can get away with doing less as there is a fundamental reason for stock prices to continue growing.

Welcome to the blogosphere's toolchest! Here, unlike other blogs dedicated to analyzing current events, we create easy-to-use, simple tools to do the math related to them so you can get in on the action too! If you would like to learn more about these tools, or if you would like to contribute ideas to develop for this blog, please e-mail us at:

ironman at politicalcalculations

Thanks in advance!

Closing values for previous trading day.

This site is primarily powered by:

CSS Validation

RSS Site Feed

JavaScript

The tools on this site are built using JavaScript. If you would like to learn more, one of the best free resources on the web is available at W3Schools.com.

Other Cool Resources

Blog Roll