In April 2009, we began keeping track of how accurate all of our predictions have been since January 2008, providing updates for our readers once a quarter ever since.

In April 2009, we began keeping track of how accurate all of our predictions have been since January 2008, providing updates for our readers once a quarter ever since.

Today, it's time once again to update our prediction accuracy score, in which we make use the most unforgiving metric ever developed for measuring performance: the plus-minus statistic from hockey and basketball!

Using this system, we gain a point if we're right, lose a point when we're wrong, and score a zero for when the outcome of a prediction either cannot yet be determined or, in the case where we make multiple predictions, when we have contrary results that cancel each other out. Like a game of horseshoes, close doesn't count where near misses are involved!

Ultimately, our plus-minus score will reveal the number of times we scored hits rather than misses in making predictions of the future. If we're no better at predicting the future than a coin toss, our plus-minus score will gravitate toward zero. If we're better at predicting the future than that, our score will rise over time, and if we're really bad, our score will surely fall.

Three months ago, our plus-minus score was +35. Here's how we stand today:

- Number of Predictions Made Since January 2008: 113

- Number of Correct Predictions: 72

- Number of Incorrect Predictions: 34

- Number of Outcomes Not Yet Determined or No Decisions: 7

Overall, for the predictions where we've been able to establish the outcomes to date, our plus-minus score has risen to +38. Measured as a percentage, our prediction accuracy rate is 67.9%.

The table below updates the status of all the predictions that we've successfully determined the outcomes during the last three months, as well as those for which we are still waiting for the outcome. The blow-by-blow commentary is just a bonus that you'll hopefully find to be entertaining!

| Political Calculations' Predictions Plus-Minus Score Update, 31 January 2011 | |||

|---|---|---|---|

| Date | Prediction | Outcome | +/- Score |

| 21 December 2009 | Using incomplete data for the month of December 2009, economy would dip in the second quarter of 2010, with a slow recovery afterward. We anticipate that meaningful growth in the number of jobs would likely begin with the third and fourth quarters of 2010. We anticipate that the NBER will declare the recession they found to have begun in December 2007 to have ended in the third quarter of 2009, but we make a case for 2010Q2 as a more realistic alternate. | Too soon to tell. It will be a while before we get a full confirmation for these predictions. On the potential plus side for us, different branches of the Federal Reserve have used their own models for predicting what the NBER will do to find that July 2009 is the month they will most likely declare to be the ending date for the recession. Update: We were a bit off in calling July 2009 as the end of the recession, since the NBER declared June 2009 as the bottom, but we nailed 2010Q2 as being exceptionally slow, making this batch of predictions a split decision so far. We're still waiting to see if meaningful growth in the number of jobs happens through the fourth quarter, but so far, we're on track with that last part of the prediction as the number of people counted has having jobs has risen since July 2010. Update: There was no meaningful improvement in the number of employed Americans after March 2010. That final part of our prediction now counts as a miss. | -1 |

| 30 July 2010 | When we updated our forecast for where the finalized GDP for 2010Q2, we snuck in a prediction for 2010Q3 in our chart. Although we expect our greatest accuracy when we used the newest, finalized GDP data for the preceding quarter, we're testing out how well projecting the next quarter's GDP based on the advance release data works out! | We'll see if we're anywhere close in October 2010, and won't know for sure until December 2010. We'll also offer a more routine prediction when the 2010Q2 data is finalized in September 2010. Update: The clock is still ticking with the advance release GDP data coming out on Friday, 29 October 2010. Update: Our forecast was for GDP to be $13,317.7 billion - the advance release data put GDP at $13,260.7 billion, an error of 0.4%, which falls within our typical 2% target range for scoring a correct prediction for GDP. | +1 |

| 25 August 2010 | Can we predict what average health insurance premiums will turn out to have been in 2010? If single coverage falls between $5,098 and $5,265 and family coverage falls between $14,166 and $14,452, then yes, we can! | We won't know until next year when the Kaiser Family Foundation releases its 2010 Annual Survey of Employer Health Benefits. Update: It turns out we should only have waited a month! The KFF's 2010 Annual Survey of Employer Health Benefits was released in September 2010, putting the average health insurance premiums for single coverage at $5,049 (a miss, even if just $49 below our target range) and for family coverage at $14,038 (a more substantial miss), as it appears the recession took a bigger bite out of the growth rate of health insurance premiums than we anticipated. | -2 |

| 28 September 2010 | We create a tool that predicts that the average cost of tuition and required fees at a four-year institution of higher learning (aka "college") will rise to $14,541 in 2009, $15,394 in 2010, $15,869 in 2011, $15,538 in 2012 and $16,212 in 2013. We modify these predictions for 2009, 2010 and 2011, taking the "under" for each of these years. We would anticipate being within 2% of the values for 2012 and 2013. | These predictions will take some time to play out. The confirmation will be provided by the annual Digest of Education Statistics produced by the U.S. Education Department. | +0 |

| 5 October 2010 | Using the finalized GDP data for the second quarter of 2010, we project GDP for the third quarter of 2010 will be within 2% of $13,284.3 billion chained 2005 U.S. dollars, giving nearly 70% odds that real GDP will actually be between $13,115 and $13,424. | This is our "official" prediction for where real GDP will be in 2010-Q3, which we'll "officially" find out on 22 December 2010. Our first indication of how close we are will come as early as Friday, 29 October 2010 when the advance estimate of GDP is released by the BEA. Update: Officially, the third GDP estimate for the third quarter of 2010 came in at $13,278.5 billion, 0.44% away from the center of our target range! | +1 |

| 8 October 2010 | Applying our tool that relates the rate of economic growth to the rate of unemployment in the U.S., we project that real GDP will be about $13,272.3 billion for 2010-Q3. Assuming that figure is correct (or nearly so), we use that result with our "official" method to project that the GDP growth rate for 2010-Q4 will fall from about 2.4% in the third quarter to 2.0%. | To be determined. It's pretty interesting to have an entirely different method of projecting future GDP give such close results to our "official" approach, where we've consistently been within 2% of our target value. Update: Officially, the final GDP estimate for the third quarter of 2010 came in at $13,278.5 billion, 0.05% away from what we forecast here using unemployment data - we may be onto something here! Unfortunately for us, the advance estimate of GDP for the fourth quarter of 2010 came in at 3.6%, which hopefully means the economy is turning the corner in a more positive direction. Altogether, we net a zero on this combination of predictions. | +0 |

| 25 October 2010 | A week before the month to which it will apply even arrives, we forecast that the average of daily closing stock prices in November 2010 will be in a range between 1182 and 1218. | With October 2010 very much on track to hit our target range for that month, this change would mark an upward move in stock prices. We went back over the data for the S&P 500 since January 1871 and found that on a month-to-monthy basis, "up" has happened some 56.1% of the time. Of course, that figure also means there's a 43.9% chance stocks will fall, so there's plenty of opportunity to be wrong. Right now, we're at the cusp for what direction the market will have moved a month from now, so here's hoping for a not-so-noisy month!... Update: The average daily closing value of the S&P 500 in November 2010 was 1198.89 - score! | +1 |

| 1 November 2010 | Using tax receipt data, we anticipate that U.S. household median income fell in 2010. We estimate it fell to a level around $47,211 from $49,777 in 2009. | We won't officially know until the U.S. Census releases the data for 2010 in September 2011, but we should have an early indication in March 2011 when it releases its Current Population Survey income data. | +0 |

| 2 November 2010 | We forecast that the number of new jobless claims for the week of 30 October 2010 will be between 411,000 and 508,000. | The actual number of initial unemployment insurance claim filings was finalized at 459,000! | +1 |

| 4 January 2011 | We recount the story of the most challenging prediction we've ever made (for where the S&P would be in December 2010), before cryptically hinting that the S&P 500 would go somewhere between 1268 and 1313, "in the absence of an excessive amount of noise or a change of fundamental outlook." | We pull off the impossible for December 2011, having predicted that the average of the S&P 500's daily closing value would fall between 1225 and 1257 "next" at Barry Ritholtz' site in early November 2011 (it averaged 1241.53 in December 2011.) As for the 1268-1313 range, there's no question that we'll hit this value for January 2011, with the S&P 500 having averaged 1282.43 through 28 January 2011. | +2 |

| 21 January 2011 | After seeing the price-dividend growth rate ratio spike in December 2010, we anticipate that we'll see a trough in stock prices by the end of February 2011. | While the 1.8% dip in stock prices on Friday, 28 January 2011 suggests a correction may be in the offing, we won't know if the S&P 500 will have passed through a trough in February 2011 until March 2011. | +0 |

We're coming up on the end of this project, which we'll terminate with our two-year predictions plus-minus score accounting anniversary in April 2011. As part of the grand finale, we'll unveil just how we rank among the community of financial and economic analysts and gurus!

Previously on Political Calculations

The following links will take you to our previous prediction outcome reports, which we've presented below in the order they've appeared here approximately every three months beginning with April 2009. You can get the most recent status updates by clicking the "track record" tag at the bottom of the post.

- Plus-Minus for Predictions - 16 April 2009

- Our Plus-Minus Is Now Seventeen! - 16 July 2009

- Predictions Plus-Minus Update - 15 October 2009

- Predictions Plus-Minus Update - 21 January 2010

- Predictions Plus-Minus Update - 26 April 2010

- Predictions Plus-Minus Update - 30 July 2010

- Predictions Plus-Minus Update - 29 October 2010

- Predictions Plus-Minus Update - 31 January 2011

Labels: forecasting, track record

W.C. Varones solved a math problem with the U.S. national debt that had been troubling the econoblogosphere since September 2010. At the end of the U.S. federal government's fiscal year in 2008, the total public debt outstanding for the United States was $10,024,724,896,912 (or more simply, over 10 trillion dollars). In 2009 and 2010, the U.S. government ran annual budget deficits of $1.416 trillion and $1.294 trillion respectively. During that time, the amount of money the government "borrowed" from itself (mainly from Social Security) rose by $141.9 billion (in 2009) and $180.8 billion (in 2010).

If you add those numbers together then, the amount of the full U.S. public debt outstanding at the end of the government's 2010 fiscal year should total $13,057,320,272,842. Instead, the total public debt outstanding for the United States was $13,561,623,030,892, over $504 billion more than what the combination of the federal government's annual budget deficits and "intragovernmental" borrowing should put it.

That more than $504 billion would then account for 14.3% of the total increase in the United States' national debt from 2008 through 2010, or roughly 1 out of each 7 dollars that the government borrowed during those two years.

Finally getting to the bottom of the matter with Econbrowser's Menzie Chinn's assistance, W.C. discovered that much of the 504 billion dollar disparity could be accounted for by the government's direct loan financing activities, where the U.S. Treasury directs money it borrows for the purpose of loaning it out to individuals and organizations in support of government-backed or subsidized loan programs operated by other government agencies.

The biggest portion of those programs are run through the Department of Education, in the form of the government's student loan programs. We thought we'd go back through the U.S. Treasury's historic data to see just how much the Federal Direct Student Loan program has grown since 1997.

The results are presented in the chart below, which shows the net outflows, which increase the national debt, or net inflows, which reduce the national debt, resulting from the federal government direct student loan program:

What we find is that since 2008, the net outflow of money the federal government borrowed to provide direct student loans has exploded, rising by $89.7 billion dollars, or 17.8% of the $504 billion discrepancy. In terms of the total increase in the national debt from FY2008 to FY2010, the explosion in student loans would account for 2.5% of the entire increase above and beyond the deficits the government ran in those years, both with the public and with itself.

We should also note that this explosion in the Federal Direct Student Loan program is not a recession-driven phenomenon. There is no similar spike, or for that matter, there's not any spike, corresponding to the recession year of 2001.

At first glance, it might seem as if the U.S. government is going to quite some extremes to keep a bubble in higher education going, but we don't think that's really what's behind the federal government's motivation for its actions. As for what we suspect might be the real motive for why the federal government has suddenly become so keen to loan money directly to U.S. students in recent years, well, we'll revisit the topic at greater length on a future date.

Update 9 May 2011: We've since revisited the topic in The Transformation of Student Loans Into Taxes!

Data Sources

U.S. Treasury. Monthly Statement of the Public Debt of the United States, September 30, 2008.

U.S. Treasury. Monthly Statement of the Public Debt of the United States, September 30, 2010.

Labels: education, national debt

Ethanol consumption in the United States has been rising exponentially for more than a decade. You might think then that U.S. ethanol producers are making money hand over fist. But are they?

At first glance, you would certainly think so, thanks to the especially generous assistance they've received from the U.S. federal government over that time. That assistance has come in the following forms:

- The government mandates that their product, ethanol, be added to the gasoline used by the overwhelming majority of motor vehicles in the United States. In 2011, the federal government will require oil companies to use over 12 billion gallons of ethanol, which will rise to 15 billion gallons in 2015 and 36 billion gallons per year in 2022.

- Their production costs are very generously subsidized. U.S. ethanol producers receive a tax credit of 45 cent per gallon for the fuel ethanol they produce. And that doesn't include the subsidies received by the agricultural interests for producing the crops, such as corn, that are used in domestic ethanol production.

- They are protected from international competition with foreign-based ethanol producers who are capable of producing ethanol more economically than U.S. producers through tariffs imposed by the U.S. government. The tariff adds 54 cents to the cost of each gallon of fuel ethanol that is be imported to the United States and sold to U.S. consumers.

Cole Gustafson, a biofuels economist at North Dakota State University, wondered just how profitable U.S. ethanol producers are. In doing that, he generated the following chart which estimates how profitable U.S.-based ethanol producers were throughout the years of 2008 and 2009:

Gustafson concludes that the fuel ethanol production industry is "close to operating breakeven." Note that "close to operating breakeven" really means "nearly or occasionally profitable."

But clearly, it isn't. Not really. After all, it takes the federal government raising the price of the fuel ethanol produced by non-U.S. producers by 54 cents per gallon and a gift from taxpayers to the tune of 45 cents per gallon to get U.S. ethanol producers "close to operating breakeven."

In 2011, that means that U.S. taxpayers will be required to give U.S. ethanol producers some 5.4 billion dollars, or if we assume there are 118 million households in the U.S., roughly $45.76 per household.

As an alternative measure, if we assume the annual burden of federal spending is $31,000 per household, eliminating the $5.4 billion in subsidies for ethanol producers would be the equivalent of freeing 174,193 American households entirely from the burden of the federal government's spending in 2011.

But then, it gets better. Because fuel ethanol could be obtained more cheaply, if the tariff on imported fuel ethanol were also eliminated, a total savings of $6.48 billion or $54.92 per household would be the result for American consumers for the 12 billion gallons of ethanol that the EPA will require to be used in the U.S. in 2011.

Those, of course, are all savings that could then be put toward more productive uses that would only help to enhance the United States' competitiveness in the world, rather than mandating that the nation's valuable resources be mired down in wasteful activities.

Sources

Environmental Protection Agency. EPA Finalizes 2011 Renewable Fuel Standards. November 2010. Accessed 24 January 2011.

Doggett, Tom and Abbott, Charles. Senate votes to extend ethanol subsidy for 2011. Reuters. 15 December 2010.

Gustafson, Cole. New Energy Economics: Are Ethanol Producers Making Money Now?. NDSU Agriculture Communication. Accessed 24 January 2011.

Rudolf, John Collins. End Ethanol Subsidies, Senators Say. New York Times' Green Blog. 30 November 2010.

Labels: gas consumption

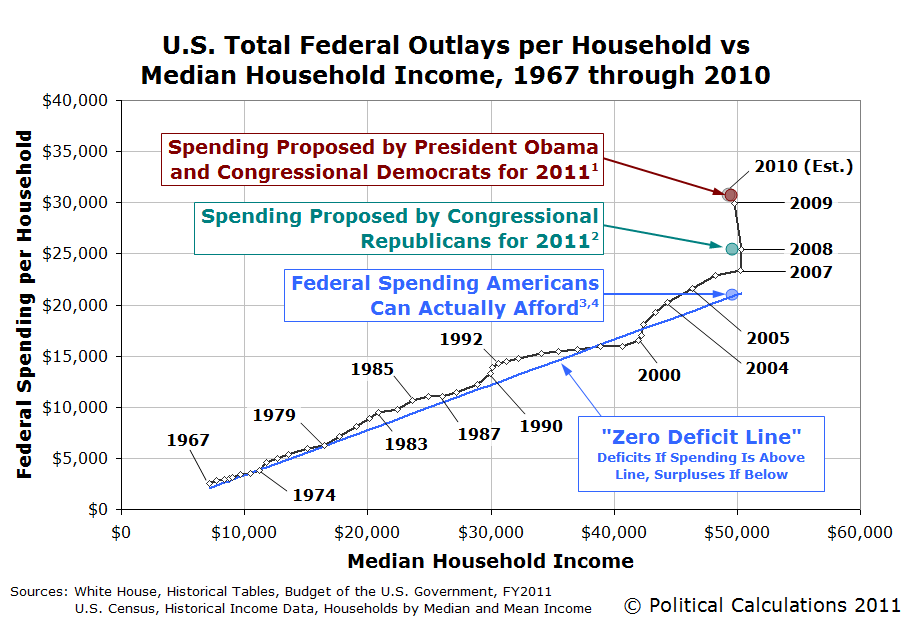

If you want to quickly see how President Barack Obama and the Congressional Democrats' federal government spending proposal for 2011 stacks up against what Congressional Republicans have in mind, shown against a background illustrating the trend in U.S. federal government spending since 1967, here you go!

References

1 Obama, Barack. The State of the Union 2011: Winning the Future. White House. 25 January 2011.

2 Sonmez, Felicia and Kane, Paul. House Votes to Cut Spending to 2008 Levels. Washington Post. 25 January 2011, 6:25 PM.

3 Independent Institute. Aim at the Zero Deficit Line. 13 January 2011.

4 Political Calculations. How Much Federal Spending Can Americans Afford? 7 December 2010.

Labels: data visualization

What happens to the amount of ethanol consumed by Americans when the federal government simultaneously mandates that an ever-increasing percentage of ethanol be added to gasoline while also subsidizing its production?

Well, perhaps unsurprisingly, what you get is what you see in the chart below happens:

The dividing line is 1993, following the Energy Policy Act of 1992, which required specified car fleets to purchase alternative fuel vehicles capable of operating with E-85, an 85%/15% blend of ethanol and gasoline. In addition, the Clean Air Act amendments of 1990 required the wintertime use of ethanol in 39 major metropolitan areas and full-year use in 9 others that had not satisfied the Environmental Protection Agency's imposed standards for carbon monoxide.

After that, it was off to the races for the ethanol-government industrial complex! Simply projecting a straight line from the trend between 1981 and 1993 would place 2010's ethanol consumption level below 5,000 thousand barrels per month. Instead, thanks to the federal government's subsidies and mandates benefiting ethanol producers, it has risen to be over 25,000 thousand barrels per month.

Data Sources

U.S. Energy Information Agency. Fuel Ethanol Overview. Accessed 24 January 2011.

U.S. Energy Information Agency. Energy Timelines - Ethanol. Accessed 24 January 2011.

Labels: gas consumption

As we write this at 12:00 PM Eastern Standard Time in the U.S., the S&P 500 is up a bit over three points from its previous day's closing value of 1,280.26, and has been up most of the morning. The market has been performing largely as expected over the past several months, rising 100 points in a very orderly fashion since the end of November 2010. And it's a really nice day outside, so we were going to spend some time there.

And yet, Barry Ritholtz's Spidey Sense is tingling (Why Cash Is King):

We think he's right. Here's how we see it.

In December 2010, our indicator of distress in the stock market, the price-dividend growth ratio, spiked:

It has since backed off, however a spike in the price dividend growth ratio is well correlated with short-term troughs in stock prices. Here are the updated statistics we have for that:

| Coincidence of Price Dividend Growth Rate Spikes with Market Troughs | ||

|---|---|---|

| Data Item | Number of Occurrences | Percentage of Total |

| Total Number of Spikes | 323 | 100.0% |

| Number of Spikes Exactly Coinciding with Trough | 78 | 24.1% |

| Number of Spikes Within One Month of Trough | 192 | 59.4% |

| Number of Spikes Within Two Months of Trough | 263 | 81.4% |

Since January 1871, whenever the price-dividend ratio has spiked in a given month, stock prices passed through a trough (a short term bottom) 24.1% of the time during the same month as the spike, 59.4% of the time within one month of the spike and 81.4% of the time within two months of a spike.

Because there is no trough in average monthly stock prices in the months leading up to December 2010, that correlation suggests that there is a very high likelihood of one occurring by the end of February 2011.

Meanwhile, we don't see any significant deterioration in the fundamentals underlying today's stock price valuations, which indicates to us that the market will soon go through a short term correction, with stock prices rebounding quickly afterward.

Consequently, we view today's upward movement in stock prices as a selling opportunity. We would expect a buying opportunity to follow in the near future.

And since we missed out on enjoying Friday to produce this post, we'll take Monday off and see you on Tuesday!

Labels: stock market

Strange Maps' Frank Jacobs sets the stage:

What if the world were rearranged so that the inhabitants of the country with the largest population would move to the country with the largest area? And the second-largest population would migrate to the second-largest country, and so on?

Here's the result:

Oddly enough, the people of four countries wouldn't have to pull up stakes and move if the world was reorganized this way: Brazil, Ireland, the United States and Yemen.

Labels: none really

Specifically, we were wrong when we speculated back on 29 November 2010 that the trend in new jobless claims that has existed since 21 November 2009 might be breaking down.

At the time, we were optimistic that the sudden decline in the number of weekly jobless claims that coincided with the first week that employers would have been able to alter their employee staffing and retention plans following the U.S. election results of 2 November 2010.

Using our "control chart" method of analyzing new jobless claims data, we would have recognized that to be the case if the weekly number of jobless claims had moved and stayed below the statistically-determined lower "control limit" line.

Instead, the data in subsequent weeks continued to fall within the boundaries of the statistical limits defined by the trend we've observed since November 2009, when the introduction of HR 3962, the legislative precursor of the Patient Protection and Affordable Care Act, derailed the then rapidly improving trend in the rate of layoffs in the U.S. as employers reacted to the increased likelihood of having higher costs imposed upon their businesses by the proposed health care reform law going forward.

What we find then is that the weekly number of new jobless claims are continuing to follow a slow, but positive downward trend, with the variation we observe being the result of what we would consider to be common causes - the kind of variation that we would likely see occurring naturally as employers respond to a variety of typical daily business events, such as weather conditions. These kinds of events may have a small impact from week to week, but not a large enough impact that can significantly affect an overall trend.

As for the overall trend that we do observe, the average rate at which the number of new unemployment insurance claims are being filed is falling is approximately 763 per week, which means that from the initial estimate of 404,000 new jobless claims that were filed this week, it will take an additional 110 weeks, or 2.1 years, for the amount of weekly new unemployment insurance claim filings claims to equal the average 319,711 per week that was typical for the U.S. economy prior to the 2007 recession.

That's a long time before the number of layoffs, the events that directly lead to the new unemployment insurance claim filings that the government tracks, would go back to levels that are consistent with a comparatively healthy U.S. economy.

Labels: jobs

The Associated Press thinks it's because gas prices are rising at the pump and because of bad weather:

Americans are driving less, with the holidays behind them and gasoline at two-year highs.

Gas costs around $3.10 a gallon, the highest price since mid-October 2008. Americans usually drive less in the winter, and recent bad weather across the country was further incentive to stay home. And money needs to go towards paying off holiday credit card bills.

But the AP seems to think that despite the views of an expert who, we couldn't help but notice, was the only named expert quoted in their entire article. Oddly enough, he doesn't seem to think that bad weather can be fingered as a culprit in what's behind what's driving Americans off the road, but is instead pointing the finger at low demand:

Drivers are "pulling back on gas right now but you can't tell whether it's weather-related," said Tom Kloza, publisher and chief oil analyst at Oil Price Information Service. "Unless you're in Boca Raton, Fla., or San Diego, you're seeing pretty sleepy midwinter demand."

We'll save you the trouble of reading the rest of the article to see if the AP ever bothered to back up their claim that bad weather was responsible for Americans driving less, because they didn't bother to do so. But that raises a good question: how has the demand for gasoline changed over time?

To find out, we've updated our chart tracking the approximate number of gallons Americans consume in oil products every day with the most recently available data which extends through October 2010 as of this writing.

What we see is that compared to the long term average of 2.56 equivalent gallons of oil products consumed per day for each U.S. resident, since late 2008, Americans are consuming an average of approximately 2.3 of oil products per person. That's approximately a 10% decline.

Which turns out to be something that even the Associated Press has noticed! In an article published in mid-December 2010, the AP reported that:

Americans are burning an average of 8.2 million barrels — 344 million gallons — of gasoline per day in 2010, a figure that excludes the ethanol blended into gasoline. That's 8 percent less than at the 2006 peak, according to government data.

Which, the AP reports, has made environmentalists very, very happy:

Environmentalists are looking at the trend with a mixture of disbelief and delight. A decade ago they thought demand would continue to grow 1-2 percent a year far into the future.

"Now you look and, wow, we've actually bent the curve," says Roland Hwang, transportation director at the Natural Resources Defense Council.

So could the AP in January 2011 be right about the price of oil having something to do with that?

As it happens, the average price of gasoline in the U.S. peaked during the summer of 2008 over $4 per gallon, when Americans were consuming more than the long term average of 2.56 gallons per day before falling to $1.75 per gallon by January 2009, before recovering and somewhat stabilizing at $2.75 per gallon through much of 2010. Prices began slowly rising again in October 2010 and are now over $3 per gallon in much of the nation.

But through most of those gyrations in the price per gallon of gas over the last few years, individuals Americans appear to have come to settle on consuming an average of 2.3 gallons of oil products per day. And from what we can tell, the price of oil only seems to be a minor factor affecting American oil consumption patterns - it has some effect, but not the effect the AP would have it claim. Especially if we go back and look how stable oil consumption has been in recent years (or at least up to 2008) with respect to how volatile gasoline prices have been over that time.

We do however have a more likely culprit for why Americans are consuming 8% less oil by the AP's measure which excludes added ethanol. Here is a chart from the U.S. Bureau of Labor Statistics indicating the percentage of American workers who are being counted as either unemployed or underemployed (the U-6 measure of unemployment) from January 2007 through December 2010.

What we see is that the percentage of unemployed and underemployed Americans has doubled from an annual average of 8.2% in 2006, when U.S. oil consumption peaked, to an annual average of 16.8% for 2010. Or rather, an increase of 8.6%.

We then observe that a sudden increase in the total unemployment and underemployment rate of 8.6% directly coincides with the period in which an 8% decrease in the actual amount of oil per person being consumed in the United States occurred.

That's because Americans who lost their jobs or who have had to accept employment at lower levels during the last few years are pretty unlikely to be out consuming the same levels of oil that they would if they had jobs or were working in jobs that pay what they are capable of earning in a healthy economy.

And that would seem to be the real reason why the environmentalists of the National Resources Defense Council are so unbelievably delighted. To them, that's a real unexpected success!

Elsewhere

Jim Hamilton quantifies the effect of rising gas prices on U.S. consumer sentiment.

Sources

Associated Press. Pump prices eyed as reason Americans driving less. 16 January 2011.

Associated Press. US Gas Demand Should Fall for Good After '06 Peak. 20 December 2010.

U.S. Bureau of Labor Statistics. Labor Force Statistics from the Current Population Survey. Table A-15. Alternative Measures of Labor Underutilization. U-6 Total unemployed, plus all marginally attached workers plus total employed part time for economic reasons, as a percent of all civilian labor force plus all marginally attached workers. Accessed 18 January 2011.

U.S. Energy Information Agency. U.S. Finished Petroleum Products Supplied (thousands of barrels per day). Accessed 18 January 2011.

U.S. Energy Information Agency. Weekly U.S. All Grades All Formulations Retail Gasoline Prices. Accessed 18 January 2010.

U.S. Census Bureau. Monthly Population Estimate, Resident Population. Accessed 18 January 2011.

Hansen, Ole S. The Economic Impact of Higher Oil Prices. Trading Floor. 17 January 2011.

Labels: environment, gas consumption

Between roads and light rail, which option would you suppose is the most cost effective for moving people into and through the downtown area of a major American city?

Now, let's add some more details. Let's say that major American city is Seattle, Washington where a major roadway, the seismically-challenged Alaskan Way Viaduct is reaching the end of its useful life.

To replace the existing elevated double-deck roadway, the Washington state government authorized a deep-bore underground tunnel project, which is set to begin construction this year. Seattle's mayor, Mike McGinn, is opposed to the project because of its high costs. So much so that he commissioned a chart comparing the cost of the project to the cost of existing throughways in Seattle, which is described by The Stranger's Eli Sanders:

The red [sic - it's really orange!] line that shows the cost of the tunnel runs almost off the chart, but the black line showing its predicted usage sat well under the present usage for the little old Ballard Bridge, and just above the predicted usage for the fixed-up South Park bridge. Said McGinn, pointing to his chart:

What their own preliminary [tunnel] studies show is that when you do [the planned tolling], you have 41,000 cars a day using the tunnel. I just want to put that in perspective, and I brought a little graph here... So the deep bore tunnel, it'll move a few more cars than the South Park Bridge, and a lot less than the Ballard Bridge, and cost... a couple billion.

Sounds outrageous, right? Now, what if we compare the cost of the proposed deep bore underground tunnel project to the cost of building a light rail system to operate over much of the same area? Specifically, the area Sound Transit's Central Link, which is similar in scale and scope to the proposed deep-bore tunnel and which Seattle has already built!

Something which the Washington Policy Center's Michael Ennis has already done, going to the trouble of modifying Mayor McGinn's chart to include it (HT: Sound Politics):

Seattle Mayor Mike McGinn loves to use this chart to show the apparent inefficiency of the Viaduct tunnel. If you follow transportation policy or the Viaduct issue, you have seen it many times. It compares cost to how many cars would use it with two other road projects in Seattle.

He then argues we should not replace the Viaduct with a tunnel because it costs too much and provides too little benefit.

McGinn's efficiency argument against the tunnel is hypocritical when the mayor also supports light rail, which is even more expensive and carries fewer people.

Washington Policy Center took McGinn's chart and added some context by including a comparison to Central Link light rail costs and ridership, which McGinn supports.

Sound Transit's Central Link light rail line cost $2.6 billion to build and, assuming that the 3,195,908 people who boarded the line during the first six months of 2010 are any indication, averages an equivalent 23,000 round trip commuters per day.

Meanwhile, Mayor McGinn's idea of a "wasteful" project, representing what perhaps is the most expensive way to build a road, would cost roughly 23% less (assuming it costs a full $2 billion) and would be capable of moving double the number of people that light rail currently does both into and through downtown Seattle.

We'll close with the Washington state's drive-through video simulation of the proposed tunnel:

Is it us or is that the nicest weather for a drive that Seattle's ever seen?

Labels: public transportation

Welcome to this special Friday, January 14, 2011 edition of On the Moneyed Midways, where we're celebrating the end of 2010 by featuring the best posts we found in the best of the past year's money and business-related blog carnivals!

Welcome to this special Friday, January 14, 2011 edition of On the Moneyed Midways, where we're celebrating the end of 2010 by featuring the best posts we found in the best of the past year's money and business-related blog carnivals!

Normally, we use the word "special" as a euphemism for the word "late", however this edition of On the Moneyed Midways is genuinely special. After five years of weekly editions, this is the last regular edition of OMM.

The reason why is that the world of money and business-related blog carnivals has changed. When we first launched OMM, it was the heyday of what might be called "Social Media 1.0," where communities of bloggers would self-organize to highlight each others' best stuff. Blog carnivals were a big deal - they were the gathering places for the growing blogging community.

Flash forward to today and we find that both search engines and Social Media 2.0 ventures like Facebook and Twitter have combined to largely replace the role of blog carnivals. To a large extent, the Social Media 1.0 phenomenon of blog carnivals have become obsolete because it's easier to find blogs and because it's easier to meet up and share information with like-minded people in the new online communities.

That's not to say there aren't good blog carnivals still around (the Cavalcade of Risk, Carnival of Personal Finance and Festival of Frugality come immediately to mind). There are, however, many fewer blog carnivals to review each week than there were just a year ago (and many fewer than two years ago), and still even fewer ones worth reviewing on a regular basis as the quality of the remaining blog carnivals themselves has diminished.

So this special edition marks the end of the line for OMM. But that's not what makes this issue special.

What makes this issue of OMM genuinely special is that we're celebrating the best posts we found among all the business and money related blog carnivals of 2010. To do that, we went back through our entire archive for the year, which appears below this special edition, and re-reviewed all the posts we marked as being either Absolutely essential reading or as The Best Post of the Week, Anywhere!.

We then systematically narrowed down the list to separate the excellent from the merely well done, and then further to distill the exceptional from the outstanding.

The results of that exercise, the best posts we found in 2010 and the post we've awarded the title of being The Best Post of the Year, Anywhere! are below. Thank you for joining us for our final regular edition of OMM!

| On the Moneyed Midways: The Best Posts of 2010 | ||||

|---|---|---|---|---|

| OMM Edition | Carnival | Post | Blog | Comments |

| January 15, 2010 | Carnival of the Capitalists | Are You Willing to Lose Your Best and Brightest Over a Bag of Pretzels? | KnowHR | Do you know how much your company spends on providing free sodas or snacks for employees? Do you appreciate how much the savings you might realize by stopping the employee freebies might actually cost your company through the higher turnover of talented staff who feel the company became a less pleasant place to work as a result? |

| April 2, 2010 | Carnival of Money Stories | I Went Homeless So You Don't Have To | Soul Acrobats | Alvin Tam wanted to confront his fears of becoming homeless by living like a vagrant for a day in Las Vegas. His experience was something else! |

| April 16, 2010 | Carnival of Trust | What Do You Sell? A Lesson in Personal Branding | The Sales Blog | S. Anthony Iannarino explores why Tiger Woods lost so many endorsement deals following a scandal in his personal life and why his "personal brand" risks sinking to the status of Lindsay Lohan's if he doesn't deliver off the golf course. |

| April 23, 2010 | Festival of Frugality | My Refrigerator Solar Cooker | Penniless Parenting | If you have an old fridge, aluminum foil, a clear plastic tablecloth, access to the sun and uncooked food, Penniless Parenting will tell you what you need to know to combine all these ingredients to make an energy-cost free dinner! |

| May 14, 2010 | Money Hacks Carnival | The Broke Person's Mantra | Miss Bankrupt | Christina identifies the thought behind the thinking that helps keep broke people, well, broke: "We think we need more, we think we deserve more, we spend money on things we didn't need before we had the money." |

| May 21, 2010 | Cavalcade of Risk | Anti-depressants and Fiscal Stimulus? | Healthcare Economist | Jason Shafrin compares government stimulus programs with what studies into anti-depressants are now revealing - they might originally have been intended for short term use, but over time, they become permanent fixtures, failing to cure the conditions for which they were prescribed. |

| May 28, 2010 | Festival of Frugality | The Wedding Gift as the Price of Admission | Surviving and Thriving | Donna Freedman reacts to J. Money's solution to the age-old dilemma of how much a wedding present should cost, while considering the potential fallout outcomes for the newlywed couple as she also argues against the rule of thumb that apparently says that the value of wedding gifts should be tied to the cost of the food provided for the guests at the reception. |

| June 25, 2010 | Carnival of HR | Establishing a Culture of Distributed Leadership | Great Leadership | Dan McCarthy explains just what it takes to have junior leaders ready to be able to take charge and get positive results without having to wait for their superiors in their organizations to act. |

| July 3, 2010 | Carnival of Money Stories | When Being Cheap Upfront Costs Big Bucks in the End | Frugal Confessions | Is parking on the street really a good idea compared to paying to park in a garage? That might depend on whether or not your car is likely to get towed away, as Amanda L. Grossman confesses. |

| August 6, 2010 | Carnival of Personal Finance | Your Big Fat Expensive Wedding: Stupid Is As Stupid Does | Len Penzo dot Com | Len Penzo offers future brides and grooms some of the best wedding planning advice available anywhere on the web by comparing the cost of Chelsea Clinton's wedding to his own. |

| August 20, 2010 | Best of Money | 5 Lessons from a Homeless Entrepreneur | Christian PF | Joe Plemon discusses what we can learn from the story of Travis Lloyd Kevie, who bought a six-pack, broke into a vacant bar, put up an "Open" sign and began serving customers, then kept his "business" going by using the money he made from that first six-pack to buy more. He had earned over $1,300 in cash and merchandise by the time he was arrested just four days later.... |

| September 17, 2010 | Carnival of Personal Finance | Spending Under Pressure | Richly Reasonable | Have you ever been "mariachi-banded?" You'll understand what that means as Lauren considers those situations where you end up paying for crazy things you'd never buy under normal circumstances in The Best Post of the Year, Anywhere! |

| October 15, 2010 | Carnival of Money Stories | Squirreling Gone Wild #16: The Crafty Waitress | Squirrelers | The Squirrelers delve into the twisted mind games a waitress inflicted upon them to try to "nudge" them into giving her a large tip. Who knew that simply eating out posed such moral dilemmas? |

| November 19, 2010 | Carnival of Money Stories | Is Gambling a Good Motivation for Students? | Faithful With a Few | Khaleef Crumbley weighs the moral implications of a web site that entices students at certain universities to gamble on whether they'll earn the grades they target for their classes at the beginning of each semester. |

| November 19, 2010 | Best of Money | Don't Become a Slave to the Rat Race | MoneyNing | Vered Deleeuw considers who the best sales people are, argues that choosing to be unpopular is a path to real freedom and extracts an extraordinarily meaningful insight from a Jennifer Aniston movie of all things in a wide ranging post that really has to be read through twice to be fully appreciated! |

| December 10, 2010 | Carnival of Money Stories | How We Slashed Our Rent in Half (and Why We're Not Crazy) | Daily Currency | Adam Baker needed to find a new place for his family to live after being overseas for two years. They could afford to choose between renting a house in a good neighborhood for $900 per month, a house in a great neighborhood for $1250 per month or a one bedroom apartment in an okay neighborhood for $450 per month. The Bakers chose the apartment and no, they're not crazy!... |

OMM's Full Index for 2010

Presented in reverse chronological order....

- On the Moneyed Midways - The Best Posts of 2010

- On the Moneyed Midways - The Best Blogs We Found in 2010

- On the Moneyed Midways - December 17, 2010

- On the Moneyed Midways - December 10, 2010

- On the Moneyed Midways - December 3, 2010

- On the Moneyed Midways - November 26, 2010

- On the Moneyed Midways - November 19, 2010

- On the Moneyed Midways - November 12, 2010

- On the Moneyed Midways - November 5, 2010

- On the Moneyed Midways - October 30, 2010

- On the Moneyed Midways - October 22, 2010

- On the Moneyed Midways - October 15, 2010

- On the Moneyed Midways - October 8, 2010

- On the Moneyed Midways - October 1, 2010

- On the Moneyed Midways - September 24, 2010

- On the Moneyed Midways - September 17, 2010

- On the Moneyed Midways - September 10, 2010

- On the Moneyed Midways - September 3, 2010

- On the Moneyed Midways - August 27, 2010

- On the Moneyed Midways - August 20, 2010

- On the Moneyed Midways - August 13, 2010

- On the Moneyed Midways - August 6, 2010

- On the Moneyed Midways - July 30, 2010

- On the Moneyed Midways - July 23, 2010

- On the Moneyed Midways - July 16, 2010

- On the Moneyed Midways - July 9, 2010

- On the Moneyed Midways - July 3, 2010

- On the Moneyed Midways - June 25, 2010

- On the Moneyed Midways - June 18, 2010

- On the Moneyed Midways - June 11, 2010

- On the Moneyed Midways - June 4, 2010

- On the Moneyed Midways - May 28, 2010

- On the Moneyed Midways - May 21, 2010

- On the Moneyed Midways - May 14, 2010

- On the Moneyed Midways - May 7, 2010

- On the Moneyed Midways - April 30, 2010

- On the Moneyed Midways - April 23, 2010

- On the Moneyed Midways - April 16, 2010

- On the Moneyed Midways - April 9, 2010

- On the Moneyed Midways - April 2, 2010

- On the Moneyed Midways - March 26, 2010

- On the Moneyed Midways - March 19, 2010

- On the Moneyed Midways - March 12, 2010

- On the Moneyed Midways - March 5, 2010

- On the Moneyed Midways - February 26, 2010

- On the Moneyed Midways - February 19, 2010

- On the Moneyed Midways - February 13, 2010

- On the Moneyed Midways - February 5, 2010

- On the Moneyed Midways - January 29, 2010

- On the Moneyed Midways - January 23, 2010

- On the Moneyed Midways - January 15, 2010

Older Editions

- OMM: The Best Posts of 2009 and our full index for the year!

- OMM's Running Index for 2008

- OMM's Running Index for 2007

- The Best Blogs Found in 2006 (and our full 2006 index)!

Labels: carnival

Welcome to the blogosphere's toolchest! Here, unlike other blogs dedicated to analyzing current events, we create easy-to-use, simple tools to do the math related to them so you can get in on the action too! If you would like to learn more about these tools, or if you would like to contribute ideas to develop for this blog, please e-mail us at:

ironman at politicalcalculations

Thanks in advance!

Closing values for previous trading day.

This site is primarily powered by:

CSS Validation

RSS Site Feed

JavaScript

The tools on this site are built using JavaScript. If you would like to learn more, one of the best free resources on the web is available at W3Schools.com.

Other Cool Resources

Blog Roll