In our previous analysis of the S&P 500, we indicated that we expected that stock prices might fall in the very near term in response to both profit-taking and the arrival of a new negative noise event associated with the possibility of a partial federal government shutdown in October 2013.

Sure enough, we can say we saw it coming! We'll squeeze just a little bit more information into the current version before we officially revise it to move past the third quarter of 2013 to show how these things have played out:

The profit-taking is pretty easy to understand, as the stock market enjoyed a run up in prices through much of September 2013 in anticipation that the Fed would not cut back on its current quantitative easing programs. But what about the possibility of a new negative noise event?

That's tougher to tell. Here, we're going to start our analysis today by looking at a bit of data being advanced by at least one uncritical left-wing economist that markets believe that the United States is at a sharply increasing risk of defaulting on its national debt.

Here's what the WSJ article he cites says:

President Barack Obama repeated Thursday that he won't negotiate on the debt ceiling and won't sign any bill that defunds or delays the health-care law. He lashed out at Republicans for what he said were moves endangering the full faith and credit of the country. "You don't mess with that," he said in a speech in Largo, Md.

The Congressional Budget Office has estimated that if the debt ceiling isn't raised, the government will be unable to pay all its obligations sometime in late October.

Investors appear to be eyeing the possibility that the issue won't be resolved, judging by the sixfold increase in the past week—to its highest level since 2011—of the annual cost of derivatives some investors use to hedge against the risk the U.S. will default on its debt.

The WSJ's chart shows how the value of the investment derivatives tied to the risk of a U.S. government debt default have changed since July 2013. But this bit of information is why we describe the left-wing economist as being uncritical, because he is taking it at face value without any apparent understanding of what it is really communicating.

Once upon a time, these kind of credit derivatives, or as they are more commonly known, Credit Default Swaps (CDS), were used by investors to hedge against the risk that an entity, say a firm or a sovereign nation, would default on its debt.

Back in 2011, they were very successful in communicating the risk that a number of European nations were increasingly at risk of defaulting on their debts. So much so that the people who run the European Union scapegoated the trading of credit derivatives for the problems of its failing nations and took steps to effectively ban them by starving them of the liquidity they would need to function as a tool that clearly communicates the risk of default.

This is significant because, as you'll note on the WSJ's chart, that risk is denominated in Euros, not U.S. dollars.

As a result of the EU's actions, credit default swaps are no longer capable of communicating the real risk of whether a nation might default on their debt. Reuters explains:

"Sovereign CDS volumes and liquidity are down massively," said Michael Hampden-Turner, credit strategist at Citigroup. "Part of that is because investors are more optimistic about risk generally, but the EU ban has also hurt liquidity."

"The market tends to be fairly one-way round, leaving it vulnerable to gapping spreads when there is activity. Dealers are not prepared to run big positions as there is nowhere to lay the risk off, which makes it worse. Every quarter volumes slide and CDS becomes less liquid, and that looks set to continue."

[...]

This is a marked change from the pre-ban era, when CDS trading would pick up when a sovereign became more stressed and it was viewed as an important pricing point.

So, if these kinds of credit derivatives are no longer effective communicators of the degree of risk that a nation might potentially default on its debt, what is? Reuters answers:

"People pricing sovereign risk now look at the bonds, so why would you look at the CDS if bonds are where the information lies? Back in the day it was the other way around, with CDS levels being the crucial signal - it's a fundamental change," said Paul McNamara, investment director at GAM.

So, let's look at the yields of U.S. government-issued bonds. Here, if the risk of the U.S. government really defaulting upon its debt had really increased, we would see a spike in bond yields - the interest rates that the U.S. government pays to its lenders. Our first chart shows the yield for the benchmark 10-Year U.S. Treasury for the past year through 27 September 2013:

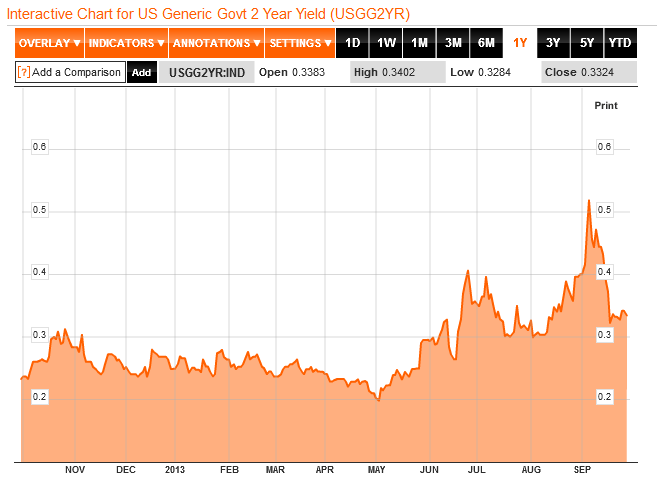

Let's next look at a shorter term bond - the 2-Year U.S. Treasury, which might show a more pronounced response to the near term risk of a U.S. default:

It doesn't do us much good to look at shorter-term U.S. Treasuries, because the Federal Reserve's Quantitative Easing (QE) program has pushed their yields down to near-zero levels. This outcome is specifically the result of what we describe as QE 4.0, which is the portion of the Fed's current QE programs that buys up U.S. Treasuries. QE 4.0 was announced back on 12 December 2012 to offset the imminent risk of a sharp contraction in the U.S. economy resulting from President Obama's desired tax hikes going into effect in 2013, and it has largely succeeded in keeping the U.S. economy out of a full-fledged recession.

In both these charts, we see the effect of the risk of the Fed cutting back on its purchases of U.S. Treasuries through its QE programs. From the beginning of May 2013, the yield on U.S. Treasuries rose in direct response to the likelihood that the Fed would begin tapering as early as September 2013, which was largely based on the perception of a strengthening U.S. economy. That probability peaked in early September, after which it became clearer that the Fed was less likely to act to taper its QE programs in September as the economy isn't recovering from being in microrecession as strongly as some data would indicate.

Through this period, both President Obama and the U.S. Treasury Secretary Jack Lew have made statements indicating that they would refuse to negotiate with congressional leaders to avoid a government shutdown or a default on the U.S. national debt, which they targeted to occur in mid-October 2013. The yields of U.S. Treasuries did not react meaningfully to their statements as we should expect if markets really believed that the risk of a U.S. default had increased.

Through this period, both President Obama and the U.S. Treasury Secretary Jack Lew have made statements indicating that they would refuse to negotiate with congressional leaders to avoid a government shutdown or a default on the U.S. national debt, which they targeted to occur in mid-October 2013. The yields of U.S. Treasuries did not react meaningfully to their statements as we should expect if markets really believed that the risk of a U.S. default had increased.

Their most recent statements came on Friday, 27 September 2013, once again emphasizing that President Obama would refuse to negotiate to avoid either a debt default or a partial shutdown of federal government operations. The yields for both the 2-Year and 10-Year U.S. Treasuries declined in response. If President Obama's claims had more credibility, yields on U.S. Treasuries would have risen in response.

But the spreads of the very lightly-traded CDS spreads for U.S. sovereign debt did, suddenly, within the last week - a jump so pronounced in the absence of any confirmation of a similar change in the yields of U.S. Treasuries that it is most likely attributable to a very small change the trading volume for it.

That kind of volatility is often a characteristic of low-volume trading activity in a market with low liquidity. It simply doesn't take very much money to create significant price changes.

It's kind of like how Intrade's prediction market for the 2012 U.S. Presidential election outcome was briefly manipulated to favor Mitt Romney following one of the presidential debates, only here, the manipulator of the market for U.S.' sovereign credit default swaps would appear to find President Obama's statements and policies to be credible.

The good news, if you can call it that, is that because of that fact, we know it wasn't the Russians, Iranians or Syrians. In this day and age, you have to take the good news where you can find it!

Labels: national debt, risk, SP 500

Here's an invention for all those of you who never outgrew the sandbox, or need to shop for somebody who didn't for Christmas: Kinetic Sand! (HT: Core77):

In case you're wondering what makes up the remaining 2% of this 98% sand invention, Core77 reports that it is polydimethylsiloxane (PDMS), which is also one of the key ingredients in Silly Putty, not to mention McDonald's Chicken McNuggets and french fries.

Ah, polydimethylsiloxane, is there nothing you can't do?

Other Stuff We Can't Believe Really Exists

- Inventions in Everything: Turning Cans Into Sippy Cups

- Inventions in Everything: Anatomical Lego Figures

- It's Not What You Think....

- Inventions in Everything: Soup Bowl Attraction

- Inventions in Everything: Making Life More Difficult

- Inventions in Everything: The Oreo Separator Machine

- Air Shark!

- Markets in Everything: Stormtrooper Motorcycle Suit

- The Bike That Rides You

- One Inventor's Stick-to-itiveness

- High Five!

- Inventions for Everything

- The Best Mousetrap Ever

- An Invention for the True Wine Connoisseur

- Three of Ten Things You Don't Need on St. Patrick's Day

- The Future Just Got a Lot Cooler Than It Used to Be

- The Worst Piece of Design Ever Done

- The Magic Marker of the Future

- Coming Soon, to a Gym Near You!

Labels: technology

We said that there was more to the story of Trader Joe's decision to dump its part-time employees into ObamaCare, and there is. What follows is our analysis of the statement that Trader Joe's provided to the Washington Post's Wonkblog over a week and a half ago, for which we're apparently the first media organization to produce any sort of serious analysis. We'll start at the top:

Thank you for writing to us. It's possible you have been misled, at least to some degree, by the headlines in some articles regarding our reasons for implementing the [Affordable Care Act] in January. We'd like to take this opportunity to clarify some facts.

For over 77% of our Crew Members there is absolutely no change to their healthcare coverage provided by Trader Joe's.

In January 2012, Trader Joe's was estimated to have approximately 5,500 employees nationwide, working at 365 stores, with half of these situated in the state of California. Today, we would estimate that figure is over 5,700, as the privately-held grocery store chain now has at least 380 locations.

According to the company's statement, of those estimated 5,700 employees, 23% are part-time employees that Trader Joe's will drop from their employer-provided health insurance program, which works out to be over 1,300 employees that will be affected by the change.

The ACA brings a new potential player into the arena for the acquisition of health care. Stated quite simply, the law is centered on providing low cost options to people who do not make a lot of money. Somewhat by definition, the law provides those people a pretty good deal for insurance ... a deal that can't be matched by us -- or any company. However, an individual employee (we call them Crew Member) is only able to receive the tax credit from the exchanges under the act if we do not offer them insurance under our company plan.

Since half of the company's employees are based in California, we can see just how "affordable" their insurance coverage will be after they are forced out of Trader Joe's employer-provided health insurance plans into the plans that will typically be available in that state. The table below reveals what we found when we used UC-Berkeley's "How Much Will a Family Save Under the New Federal Health Law? California Calculator" application to approximately determine what a single adult or a single adult parent with one child will have to pay for health insurance on the state's exchange:

| Estimated Full Cost of Monthly Premium for Second-Least Expensive "Silver" Health Insurance Plan in California in 2014 | ||||

|---|---|---|---|---|

| Household Description | Age 21 | Age 25 | Age 30 | Age 35 |

| Single Adult | $230 | $231 | $261 | $281 |

| One Adult, One Child (Under Age 21) | $376 | $377 | $407 | $427 |

| Source: University of California at Berkeley Labor Center | ||||

California's "Silver" plans are intended to cover roughly 70% of the health care expenses for the individual or family covered by the plan will have, with the remaining 30% of the costs being paid for by the insured. But that's after paying the premiums for the plan, the full cost of which would run anywhere from a minimum of $2,760 per year for a single, 21-year-old individual with no children to $5,124 per year for a 35-year-old single parent with just one child.

We know from a previous example that we considered that Trader Joe's employer-provided health insurance policies are much closer to what would qualify as being a "Gold"-level plan on the new exchanges being established under the Patient Protection and Affordable Care Act, which would cover roughly 80% of the costs for health care incurred by the insured. The costs associated with the "Silver" plans that we've listed above would therefore represent a downgrade in the quality of coverage, even though they would be considered to be more affordable because they cost less than what a "Gold"-level plan would cost. Basically, the savings result because you pay less to get less.

These numbers don't consider the role that the new ObamaCare subsidy tax credits might play in reducing the out-of-pocket costs that would be paid by Trader Joe's employees, but we'll need to know how much they earn to be able to approximate what their actual out-of-pocket costs for insurance will be after being kicked out of Trader Joe's employee plan into California's ObamaCare health insurance marketplaces.

Fortunately for us, Trader Joe's provided just such an example.

Perhaps an example will help. A Crew Member called in the other day and was quite unhappy that she was being dropped from our coverage unless she worked more hours. She is a single mom with one child who makes $18 per hour and works about 25 hours per week. We ran the numbers for her. She currently pays $166.50 per month for her coverage with Trader Joe's. Because of the tax credits under the ACA she can go to an exchange and purchase insurance that is almost identical to our plan for $69.59 per month. Accordingly, by going to the exchange she will save $1,175 each year ... and that is before counting the $500 we will give her in January.

Let's do some relevant math to get some insight into what's going on here:

- Assuming the single mother, parent of one child, works 52 weeks per year, at a wage of $18 per hour and working 25 hours per week, she will earn $23,400 in a year.

- Trader Joe's claims she has been paying $166.50 per month, or $1,998 per year, for health insurance through the company's health insurance program, which covers both herself and her child.

- If she buys insurance on California's ObamaCare exchange, Trader Joe's claims she will only pay $69.59 out of pocket each month, which works out to be $835.08 per year.

- The difference between $1,998 per year and $835.08 per year is $1,162.92, which would be the actual annual "savings" that she would have if Trader Joe's accurately represented these figures.

Trader Joe's states that the savings would be $1,175 per year, which is off by $12.08. That doesn't sound like much, but it was enough to get us to dig deeper into their numbers.

Using the tool we originally developed to determine whether it would be better to buy health insurance on your state's ObamaCare exchange or to pay the ObamaCare income tax instead, we reverse-engineered Trader Joe's numbers. Here's the adapted version of the tool with the relevant numbers so you can see what we found (the calculations below apply just for 2014):

Since the $377 figure in our tool represents the estimated second-lowest cost for a "Silver" plan for a 25-year year old single mother with one child, it appears that Trader Joe's would have their employee enroll in what the price for the monthly premium for the health insurance plan being considered suggests is the lowest-cost "Silver" plan for health insurance, which appears to run $367.81 per month.

Once again, since we've already established that the coverage of Trader Joe's employer-provided plan is more akin to a "Gold"-level plan in the new ObamaCare exchanges, this represents a downgrade in the quality of the single mother's health insurance coverage.

If the employee were willing to continue paying the same $166.50 per month, or $1,998 per year, for health insurance that she is today for a "Gold" or perhaps even a "Platinum"-level plan on California's ObamaCare exchange, she could afford a plan with a premium of $464.72 per month, or $5,576.64 per year, which would be more equivalent to the level of coverage she had through the plan that Trader Joe's previously provided to her family.

As such, we can work out how much Trader Joe's stands to gain from dumping their single mother employee onto the ObamaCare health insurance marketplaces. Here, assuming that our estimated ObamaCare "Gold" or "Platinum" health insurance cost is close in value to the full cost of the policy that Trader Joe's provides today for this particular employee, we find that since the employee is contributing $1,998 toward the cost of their health insurance premium, Trader Joe's must be paying about 64.2% of the full cost of the health insurance toward her family's coverage, or $3,578.64. Multiply a number like that by 1,300 part-time employees being dropped from good health insurance coverage into ObamaCare, and suddenly, we're talking about millions of dollars worth of reduced costs and savings for the company.

This is why Trader Joe's is able to provide the part-time employees that it's ousting from its employer-provided health insurance plans with $500 each. In reality, they would be reducing their costs and increasing the company's annual profit by $3,078.64, and that's just from dumping this single employee onto the ObamaCare exchange in California.

Let's resume going through Trader Joe's statement to the media:

While we understand her fear of change, at her income level this is a big benefit that we will help her achieve.

Hopefully, she won't recognize that in gaining this "big benefit" as Trader Joe's would have her do, she's putting herself into a situation where she has health insurance coverage of lesser quality than she did before, putting her at risk of higher out-of-pocket expenses.

Clearly, there are others who will go to the exchanges and will be required to pay more. That is usually because they have other income and typically a spouse who had a job with no benefits and they do not qualify for the subsidies under the ACA.

One example of that we had yesterday was the male Crew Member who worked an average of 20 hours per week but had a spouse who is a contract consultant who makes more than $200,000 per year. The Crew Member worked for the medical benefits and unfortunately for them they are likely to have to pay more because of their real income. We understand how important healthcare coverage is to our Crew Members and we are pleased to be able to provide and support this program.

Does this means that in addition to greedily profiting from pushing their part-time employees into lower quality health insurance by selling them on the phony "big benefits" they'll get if they do, they also oppose the idea of any of their employees being married to people who also work in jobs that don't provide the generous benefits that Trader Joe's has previously sought to provide, but would now appear to believe are too generous?

We do hope this information helps, and we appreciate your interest in Trader Joe's.

It helped quite a bit actually. It tells us exactly what Trader Joe's principles and priorities were and will be with respect to their employees, given the perverse incentives created for the company by the Obamacare law.

We must remember that before the law's provisions kicked in, the company was very willing to provide very generous benefits to all of its employees. We're just starting to find out how the law has changed their perspective on the value of their crew members so much that they're now willing to kick 23% of them to the curb. The company is being compelled by President Obama's Patient Protection and Affordable Care Act to break the trust they worked hard to build with their crew members.

And that's perhaps the biggest problem with Obamacare. ObamaCare breaks trust.

References

University of California at Berkeley Labor Center. How Much Will a Family Save Under the New Federal Health Law? California Calculator. [Online Application]. May 2013. Accessed 23 September 2013.

Oakner, Larry. Trader Joe's: The Chicken or the Egg? [Online Article]. CoreBrand. 10 January 2012. Accessed 23 September 2013.

Kliff, Sarah. Trader Joe's cut health benefits last week. Here's its side of the story. [Online Article]. Washington Post. 16 September 2013. Accessed 23 September 2013.

Labels: business, health care, personal finance, risk, tool

How much would the U.S. federal government need spend per household to even come close to balancing the annual U.S. federal budget?

The answer is presented in a single picture below:

Comparing the relative location of the Zero Deficit Line on the chart, which is based on the overall trend of the U.S. federal government's total receipts with respect to median household income from 1967 through 2008 (before President Obama was sworn into office), with the level of spending done by the U.S. federal government in 2012, we find that the federal government would have to reduce its spending by $7,690 per U.S. household to even get anywhere close to a balanced budget.

To get a sense of how much money that really is, please consider that in 2012, there were 122,438,420 U.S. households.

Also keep in mind that the U.S. national debt will only continue to rise if the amount of federal government spending keeps falling on the wrong side of the Zero Deficit Line.

References

White House Office of Management and Budget. The Budget for Fiscal Year 2014, Historical Tables. Table 1.1. - Summary of Receipts, Outlays, and Surpluses or Deficits (-): 1789-2017. [PDF Document]. 10 April 2013.

U.S. Census. Current Population Survey. Historical Income Tables: Households. Table H-5. Race and Hispanic Origin of Householder - Households by Median and Mean Income. [Excel Spreadsheet]. 17 September 2013.

Labels: data visualization, national debt

Last week, we introduced our tool that can help you choose which option is financially better for you: buying an Obamacare insurance plan in your state or paying the Obamacare income tax. When we did, we hinted that there was more to the story regarding the default values that we entered into our tool, and today we're following up that story: they are the numbers that apply to a young woman who just found out that her employer, Trader Joe's, is going to drop her and a large number of other part time employees from the company's health insurance program for employees.

Owned by Germany's Albrecht family, who also own the German-based Aldi international grocery store corporation, Trader Joe's previously had the reputation of providing above-market compensation and benefits for its employees, where it traded higher labor costs for higher productivity and lower employee turnover-related expenses for the firm.

Here are a number of key excerpts from the anonymous woman's story, which came out in response to a memo that the company issued to its staff on 30 August 2013:

A current Trader Joe's worker described the coverage she'll likely lose as "one of the best parts about the job." (The employee requested anonymity since she isn't authorized to speak to the media.) She said she pays only $35 per paycheck, or $70 per month, for a plan that generally covers 80 percent of her medical costs, carries a reasonable $500 deductible and includes prescription drug coverage.

"There are several folks I work with who are there for the insurance as much as anything, mostly folks with young families," she said. "I can say that when I opened and read the letter yesterday my reaction was pure panic, followed quickly by anger."

The employee said she averages about 28 hours per week and worries she won't make the cutoff for company-based coverage. Whether workers hit the 30-hour threshold and become eligible for the company plan will be determined by their work schedules over the course of the next three months, the memo explains. For those who may be on the cusp, the memo left little hope that they can pack in extra hours to meet the requirement.

"It is important to note ... we do not create our weekly schedules with healthcare eligibility in mind," Bane wrote. "Rather, we will continue to create weekly schedules that are solely focused on supporting the customer experience."

The worker, who took home less than $20,000 last year, might be able to find a similar plan at a comparable cost under Obamacare, judging from a subsidy calculator. But there's no guarantee, other than uncertainty.

Here's what we can work out from the information presented in the article with some straightforward economic detective work. The employee is relatively young and single, which we can determine from the relatively low values she provide for what she pays for her current health insurance coverage.

That employee benefit was very generous. Her health insurance plan was roughly equivalent to what would be considered to be the "Gold" level plans that are now being marketed through the new state health insurance marketplaces, which we can deduce from the fact that she indicates that it covers approximately 80% of her health care costs. While those plans would typically not have a deductible, she indicates that her deductible is $500, which is about one-fourth what would be typical for the next-lower tier "Silver" plan available through the state health insurance exchanges.

At $35 per paycheck, her annual out-of-pocket cost for her portion of the premiums that she pays for near-equivalent Gold plan is $910, assuming that she is paid on a biweekly basis. The article does not provide enough information to determine the full actual cost of her health insurance premiums.

The article also provides critical information about her income. It indicates she earns "under $20,000" per year, working an average of 28 hours per week. Assuming that she works 52 weeks per year, that would put her hourly wage at less than $13.74 per hour. For our purposes, we'll assume she actually earns $13.70 per hour, which would give her an annual income of $19,947.20, which is just "under $20,000".

Next, we'll consider what her health insurance costs might be if she chooses to buy a health insurance plan through her state's ObamaCare exchange. Since nearly half of all of Trader Joe's stores are located in California, we'll use that state's exchange information. That's where our assumption that she is relatively young comes into play, as the data we'll use in our tool is take from Covered California's average statewide rates that will apply for a 21-year old in that state in 2014.

In the chart above, the top value listed for each income level represents the "typical" out-of-pocket potion of the average monthly premium for each plan, while the lower green value that's listed represents the average subsidy that a single individual might receive, which is based upon the cost of the second-least expensive "Silver" plan. Adding the two values together gives us the full actual cost of an average health insurance premium for a 21-year old in California.

We'll use the cost differences between the "Bronze" plans listed in the chart above, where approximately 60% of the insured's health insurance costs are covered under the plan and the "Silver" plans, which cover around 70% of the insured's health care expenses, to estimate what the near-equivalent "Gold" plan would cost her. Taking the average of the second-least and third-least expensive plans listed, we estimate the typical average monthly cost of a "Gold" plan in California would be $283.

With all that data then, we can now establish what the real financial choice that will soon be faced by Trader Joe's part-time employee in the tool below. We'll find out how much she'll have to pay for health insurance plan that's nearly equivalent to the one that Trader Joe's is taking away from her, and whether she would simply be better off paying the tax, and only buying the insurance if and when she actually needs it. Update 18 November 2014: We updated the tool to do the math for 2015 and after - just select the year!

For the default values we've entered in the tool above, which doesn't factor in Trader Joe's $500 "go-away" payment, we find that if our heroine can reasonably expect to be healthy, it will be much less costly for her to hold off on buying any health insurance until she might actually need it and pay the additional tax on her income instead, as she will come out ahead by $1,551.01 per year. [Update: There was a small glitch in our original calculation - now fixed (HT: Sean Parnell)!]

We also find that she comes out behind if she chooses to buy into a health insurance plan in California that's nearly equivalent to what her previous employer-provided health insurance coverage was. At her $19,947.20 annual income, she could expect to pay $1,650.48 per year out of her own pocket for the "Gold" level plan that is most nearly equivalent to the coverage that Trader Joe's was previously providing her with an out-of-pocket cost to her of $910, which leaves her some $740.48 in the hole, even after she collects ObamaCare's subsidy tax credit.

Even with Trader Joe's promised extra check for $500, she would still find herself at least $240.48 in the hole compared to today, unless she accepts lesser health insurance coverage that requires her to pay a much larger percentage of her health care costs. And it only gets worse if we account for that extra $500 payment to our heroine's income, because it reduces her ObamaCare subsidy, but we'll leave that for you discover for yourself in our tool above.

The bottom line is that this is a clear example of a case where an individual is both not going to be able to keep the plan they have today where they also come out worse off than they were before, whether through being forced into lesser insurance coverage or through having less disposable income after taxes and health insurance costs.

Looking at Trader Joe's motives in dropping the health insurance it was providing to its part-time crew members, if our estimated full annual cost of $3,396 for a "Gold" plan in California's ObamaCare health insurance exchanges is a good indication of what the company was spending per employee to provide that coverage, reducing that figure by the $910 that the part-time employee was paying per year means that the company stands to reduce its costs for health insurance by $2,496 per previously-covered part-time employee before its $500 "don't bother us" payment, and $1,996 per previously-covered employee after it.

There's still more to the story, as Trader Joe's has both taken heat in the media and responded to the criticism that it has received for dumping its part-time employees out of its health insurance coverage program, but we'll cover that in an upcoming post.

References

Covered California. Health Plans & Rates for 2014: Making the Individual Market in California Affordable. [PDF Document]. 23 May 2013. Accessed 21 September 2013.

HealthPocket. Obamacare Metal Plans. [Online article]. 1 June 2013. Accessed 21 September 2013.

Labels: health care, personal finance, risk, taxes, tool

Occasionally, our readers keep us on our toes by asking really good questions. Today, we're going to share part of an e-mail exchange we recently had, in which we get into the nature of when, where, why and how the analytical methods we've developed to anticipate what stock prices will or should be will work. We reckon its a good time to fit that discussion into a regular post since we doubled up on our ongoing series of weekly observations on how the S&P 500 is behaving last week, and because its always a great time to identify and describe a phenomenon that many professional investors may not even know exists.

Here's the e-mail that kicked off the discussion, followed by our response, which we've enhanced by adding links and charts, as well as some text for clarification in boldface font. Enjoy!

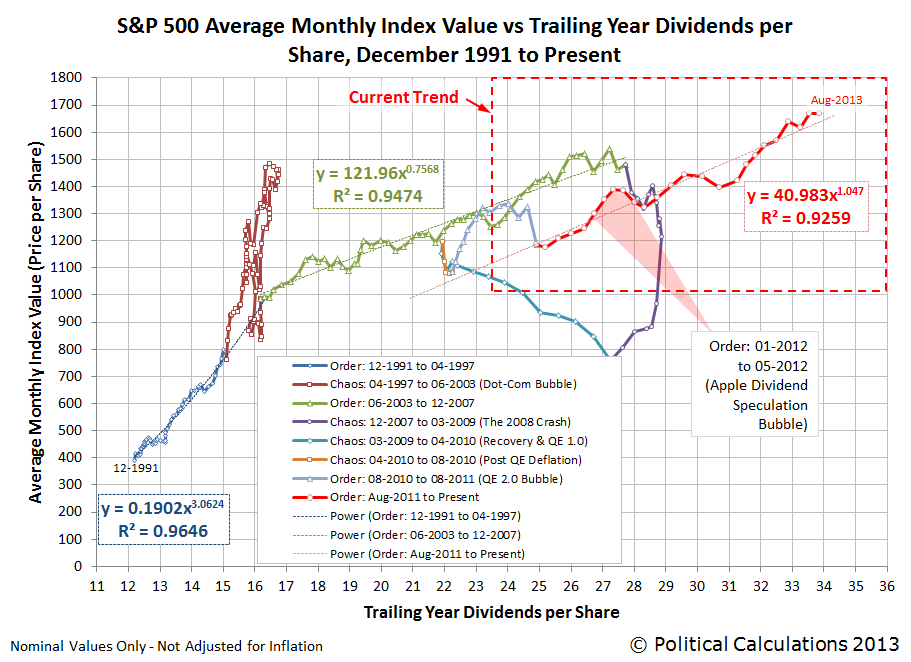

I have really been enjoying the S&P 500 posts lately concerning index value vs. trailing year dividends.

Not to make things more complicated than they need to be, but have you ever considered breaking it down into sectors? Would that help to explain even further what is going on in the market?

I ask this question because I think of things like the 2007-2009 market decline. If you just look at the S&P500 index value, you may not have realized the market was in a major decline until early to mid 2008. If you looked at the sectors (e.g., XLB, XLE, XLF, XLI, XLK, XLP, XLU, XLV, XLY) you would have seen that most of the market sectors were in decline since 2006 or 2007, except for energy and basic materials. They were keeping the index afloat. It would only be a matter of time before they collapsed, too.

I realize that looking at your index vs. trailing year dividends, it's much more obvious that something was up with the market, going from order, to disorder. I just wonder if it would be even more clear if it was broken down on a sector by sector basis.

Thanks for your comments and question!

The main challenge for what you describe is the available data. While it's easy to get the market-cap weighted values for each sector's stock prices, getting market-cap weighted dividend data for the various sectors is a little more difficult (we would have to take each component stock's projected future dividends per share for each sector and weight them according to their market cap within the sector, which would be pretty time consuming.)

Aside from that, we would also see greater volatility in the price portion of the data, since we would be looking at a smaller section of the market.

Apple provides a pretty good example of what we mean here. Individual stock prices, like Apple's, are really volatile over time, as there is often a lot of speculation (or noise) affecting them in addition to the more fundamental driver of their dividends (or signal). If you recall last year, Apple's stock price ran up considerably in the months and weeks leading up to their announcement that they would initiate a cash dividend on the speculation that they would do so.

After they announced it, Apple's stock price began to fall. But the S&P 500, of which it became the largest component, did not, even though it had been rising with it.

The reason why is because of an effect that we'll call "conveyance". Here, Apple's stock price rose on the speculation of investors who on having bought on the rumor, after their dividend announcement, sold on the news.

Much of that money stayed in the stock market, going to buy other stocks as investors sold off their shares of Apple as they rebalanced their portfolios. That rebalancing, in turn, allowed the S&P to keep rising (and sustain its value), keeping in tune with the index' increased level of dividends. In effect, Apple's dividend was conveyed throughout the entire index, supporting its (the index') valuation, even though Apple's stock price itself fell in the weeks and months that followed.

We capture that effect in looking at the entire index, but can lose the strong correlation when looking at sectors or individual stocks, where the conveyance effect can be affected by investors rotating into or out of particular sectors or stocks, making them much more volatile than the index as a whole.

Quick history: The starting and ending dates we selected for our charts above coincide with the date at which dividend futures contracts for 2011-Q4 and 2012-Q2 expired. The serious speculation that Apple would initiate a dividend began after the expiration of the 2011-Q4 futures contracts. Apple made the announcement that it would begin paying a dividend on Monday, 19 March 2013.

Its stock price was buoyed up for another three weeks as the speculative bubble inflated (see our third chart in this post), peaking on 9 April 2012 as investors finally began to realize that the company's stock price was getting too disconnected from where its own fundamentals would place it, after which the conveyance effect really kicked in.

You can see that in the second chart that we've added to our original exchange above, where most of the conveyance effect took place between 9 April 2012 and 30 April 2012, after which Apple's stock price and the rest of the S&P 500 resumed following mostly matching trajectories, which is what we should expect for the new 800-pound gorilla of the S&P 500.

Since the end of the Apple speculative bubble in May 2012, the S&P 500 has mostly followed a stable trajectory, as the market has largely continued in the period of relative order that began in August 2011.

Labels: dividends, SP 500, stock market

![Woman posed with stack of packages of $1 silver certificates at the Bureau of Engraving and Printing, Washington, D.C. [between ca. 1950 and ca. 1969] Source - loc.gov/rr/business/money/paper.html](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEhrVZsRdezoSYB-Bm08VZ-UZLb1rzZuCCjFvmd7ly7TK5HN2eQze48DW809qisWe2bMMVSfzm2Bep_50mm8RSFofnhefZr5oeBRgTNjOCYKKnAVbfxA7K5FkXKOuyvsxTeLHt44/s1600/a-money2_3b38767r-source-loc-gov.jpg)

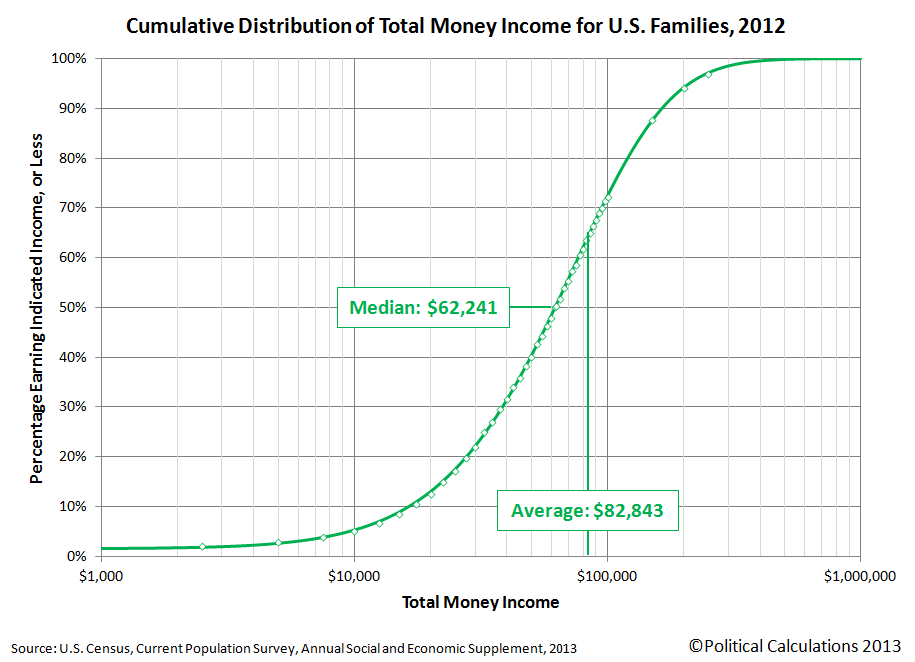

Where do you stack up in the distribution of income within the United States?

We can help you answer this question using the data that the U.S. Census Bureau has collected on the total money income earned by individual Americans, as well as for the families and households into which Americans gather themselves!

If you're a visual person, we'll first present the information graphically in chart form and then we'll present a tool where you can get a more precise estimate of what your percentile ranking is within each of these groups. In the charts below, first find the income that applies for you on the horizontal axis, then move directly upward to the curve that defines the cumulative distribution of income. Once you've found your place on S-shaped curve in each chart, look directly to the vertical scale on the left hand side of the chart to determine your approximate U.S. income percentile ranking.

The first chart applies for individual Americans, which includes all people Age 15 or older who received some kind of money income on a regular basis, say from full-time jobs or Social Security benefits, but not for things like food stamps, health benefits, housing assistance, capital gains, etc.. With that being the case, the Census Bureau's data tends to understate the amount of effective income that Americans have, especially at the lower end of the income spectrum:

Our second chart shows how the distribution of income changes when individual Americans are grouped into families, which the Census Bureau defines as being a "group of two people or more (one of whom is the householder) related by birth, marriage, or adoption and residing together":

Our third chart is similar to the families chart, but here, individual Americans have been grouped into households. Households are different from families in that they consist of "all the people who occupy a housing unit", regardless of whether they are related to each other by birth, marriage or adoption, or not, and even a single individual who lives alone is considered to be a distinct household.

So much for the pictures - let's see where you really fit in! To find out where you, your family or your household ranks among each of these categories, just enter your personal income, your family's income, which includes the incomes of your spouse and other family members who live with yout, and also the combined income of just the people who live within the walls of the same household that you do. We'll do some quick math and provide a more precise estimate of the percentage of all American individuals, families and households that you outrank given the incomes you enter.

And as a bonus, we'll also break down the numbers for your Individual income to tell you how you compare to your fellow male and female Americans.

It all starts below! (Unless you're accessing this article through a site that simply republishes our RSS news feed, in which case, you should click through to our site to access a working version of our tool....)

Update 13 September 2017: We have a more up-to-date tool available here!

Update 16 September 2014: You can now find your income percentile ranking for 2013 in our tool below - just change the year! And if you want to see the latest cumulative income distribution charts, click here!

For our readers who live outside of the United States, you can still get in on the action if you convert your income from your local currency into U.S. dollars first!

Notes

The default data we've presented in the tool above represents the average total money income of U.S. individuals, families and households for the year you select. Oh, and as a bonus, you can also see where you would have fit in the U.S. income distributions we've modeled going back to 2011 by selecting your year of interest (other years may appear in the future!...)

In the tool above, your percentile ranking indicates the percentage of Americans who either share your income or earn less than you do. As such, it tells you what percentage of the population you're above in the income-earning food chain.

For example, a percentile ranking of zero would indicate that you are at the very bottom end of the American income spectrum, while a percentile ranking of 100 indicates that you are effectively at the very top end. A percentile rank of 50.0 would indicate that you're within spitting range of being the middle of all Americans, as our tool should be able to place most people within 0.2% of their actual percentile ranking.

Finally, if you're looking for the income data for this year, please note that the U.S. Census Bureau will report the data it collects for this year sometime in September of next year. The delay isn't all bureaucratic - they send out the surveys for income in March of each year, just as or after most Americans fill out their income taxes for the previous year so their income figures are still fresh in their memories, and then it can take the Census Bureau's statisticians up to six months to sort it all out and make some kind of coherent sense of it all!

References for 2012 Incomes

U.S. Census Bureau. Current Population Survey. Annual Social and Economic (ASEC) Supplement.Table PINC-01. Selected Characteristics of People 15 Years and Over, by Total Money Income in 2012, Work Experience in 2012, Race, Hispanic Origin, and Sex. [Excel Spreadsheet]. 17 September 2013. Accessed 17 September 2013.

U.S. Census Bureau. Current Population Survey. Annual Social and Economic (ASEC) Supplement.Table PINC-11. Income Distribution to $250,000 or More for Males and Females: 2012. Male. [Excel Spreadsheet]. 17 September 2013. Accessed 17 September 2013.

U.S. Census Bureau. Current Population Survey. Annual Social and Economic (ASEC) Supplement.Table PINC-11. Income Distribution to $250,000 or More for Males and Females: 2012. Female. [Excel Spreadsheet]. 17 September 2013. Accessed 17 September 2013.

U.S. Census Bureau. Current Population Survey. Annual Social and Economic (ASEC) Supplement.Table FINC-07. Income Distribution to $250,000 or More for Families: 2012. [Excel Spreadsheet]. 17 September 2013. Accessed 17 September 2013.

U.S. Census Bureau. Current Population Survey. Annual Social and Economic (ASEC) Supplement.Table FINC-01. Selected Characteristics of Families by Total Money Income in: 2012. [Excel Spreadsheet]. 17 September 2013. Accessed 17 September 2013.

U.S. Census Bureau. Current Population Survey. Annual Social and Economic (ASEC) Supplement.Table HINC-06. Income Distribution to $250,000 or More for Households: 2012. [Excel Spreadsheet]. 17 September 2013. Accessed 17 September 2013.

U.S. Census Bureau. Current Population Survey. Annual Social and Economic (ASEC) Supplement.Table HINC-01. Selected Characteristics of Households by Total Money Income in: 2012. [Excel Spreadsheet]. 17 September 2013. Accessed 17 September 2013.

Labels: income, income distribution, tool

Welcome to the blogosphere's toolchest! Here, unlike other blogs dedicated to analyzing current events, we create easy-to-use, simple tools to do the math related to them so you can get in on the action too! If you would like to learn more about these tools, or if you would like to contribute ideas to develop for this blog, please e-mail us at:

ironman at politicalcalculations

Thanks in advance!

Closing values for previous trading day.

This site is primarily powered by:

CSS Validation

RSS Site Feed

JavaScript

The tools on this site are built using JavaScript. If you would like to learn more, one of the best free resources on the web is available at W3Schools.com.

Other Cool Resources

Blog Roll