Say what you might about the narrow breadth of the rally in the S&P 500 (Index: SPX), there's no denying that its carving out record highs on a daily basis.

After holding below the 3,400 level for no apparent reason in the preceding week, the index broke through and, five trading days later, has broken through the 3,500 threshold. More remarkably, the trajectory of the S&P 500 falls well within the redzone forecast range we added to the alternative futures chart several weeks ago.

- Snapshot on 28 Aug 2020")

The big news of the week that was came from the Fed's annual retreat in Jackson Hole, Wyoming, where Jerome Powell confirmed the Federal Reserve's inflation target would no longer be a ceiling, but instead be an average. Which is to say the Fed will tolerate inflation running higher than its official 2.0% target for sustained periods of time going forward.

That tolerance means the Fed will leave the Federal Funds Rate within its zero-range bound for the indefinite future. For investors, that equates to a relatively expansionary monetary policy compared to the Fed's previous framework. But not more expansionary than what they've been expecting since mid-July 2020, which is why the trajectory of the S&P 500 continues to track along with the redzone forecast.

There really wasn't much else in the way of market-moving news in the past week, where we scraped the following headlines from the week's newstream.

- Monday, 24 August 2020

- Daily signs and portents for the U.S. economy:

- Oil prices rise as storms cut U.S. production

- Republicans, Democrats trade blame for stalled U.S. coronavirus aid legislation

- Top U.S., Chinese official optimistic on Phase 1 trade deal after phone call: USTR

- Bigger trouble unfolding in Latin America:

- Brazil's GDP probably crumbled 9.4% in second quarter under coronavirus spread, Reuters poll shows

- Colombian businesses ask government for up to $13.1 billion to stave off collapses

- Bigger trouble, stimulus still developing in China:

- Chinese banks to post first first-half profit drop in over a decade amid pandemic pain

- China will step up technology innovation to drive growth: President Xi

- S&P, Nasdaq close at new highs as Wall Street rides bull momentum

- Tuesday, 25 August 2020

- Daily signs and portents for the U.S. economy:

- Oil hits five-month highs as U.S. producers cut output ahead of hurricane

- U.S., China reaffirm commitment to Phase 1 trade deal in phone call

- U.S. consumer confidence at six-year low; underscores concerns about economic recovery

- Trump says he will add $1 billion to food for families program

- Bigger trouble developing in Eurozone:

- S&P 500, Nasdaq close at record highs on trade, vaccine developments

- Wednesday, 26 August 2020

- Oil steadies; virus concerns weigh as hurricane heads to U.S.

- Bigger trouble developing in Mexico:

- Bigger stimulus developing in Eurozone, Japan, China:

- German coalition agrees 10 billion euro extension of coronavirus relief

- Top Japan government spokesman signals push to re-open economy, boost stimulus

- China will release funds to local governments more quickly to boost economy

- Fed minion has gloomy outlook, ECB minions ready to sit on hands again:

- Fed's Bowman sees slow, uneven recovery ahead

- ECB can wait for data as economy grows in line with projections: policymaker

- Wall Street closes higher as momentum stocks push S&P 500, Nasdaq to new highs

- Thursday, 27 August 2020

- Daily signs and portents for the U.S. economy:

- Oil prices slip as Hurricane Laura's blow unlikely to have sustained impact

- U.S. labor market recovery slowing; economists urge more fiscal stimulus

- Bigger trouble developing in India, South Korea, China:

- Recovery hopes dashed for India's recession-hit economy: Reuters poll

- South Korea's August exports seen falling for sixth month on fewer working days: Reuters poll

- We share workers: Chinese factories redeploy staff to weather pandemic blow

- Signs of bigger stimulus gaining traction in China:

- Fed minions announce change in inflation target policy:

- Fed to target 2% average inflation, elevates focus on jobs

- In landmark shift, Fed rewrites approach to inflation, labor market

- What is the Fed's new policy framework, and why does it matter?

- U.S. inflation seen rising but still below target after speech by Fed's Powell

- Powell: Jobs recovery faces 'long tail' of a couple of years

- S&P, Dow close higher on new Fed inflation stance, COVID test hopes

- Friday, 28 August 2020

- Daily signs and portents for the U.S. economy:

- Oil prices dip as producers, refiners avoid worst of hurricane

- U.S. consumer spending rises strongly; outlook uncertain as fiscal stimulus fades

- White House suggests $1.3 trln coronavirus aid bill; Pelosi says not enough

- After changing inflation target, Fed minions not sure what target will be:

- Fed policymakers do their own math on 'average' inflation

- Fed's targeting of higher inflation could backfire, paper suggests

- Fed minions also not sure what U.S. economic recovery will look like:

- Fed's Harker sees shape of recovery as 'bumpy swoosh'

- Fed's Mester says U.S. economy could end 2020 down 6% for the year

- Fed's Mester: Recovery will be slow and require more fiscal and monetary support

- Tech powers S&P 500 to record closing high, Dow now positive for the year

Those were what we thought the market moving headlines of the past week were, but other stuff happened too. Check out Barry Ritholtz' succinct summary of positives and negatives he found in the rest of the week's economics and markets news!

There's a fun project going on among math bloggers and vloggers, who are presenting their favorite big numbers that are larger than one million, tagging their contributions with the #megafavnumbers hashtag.

Since we periodically cover math stories, our contribution is 602,214,076,000,000,000,000,000, which if you've had chemistry, you'll probably recognize more quickly in its scientific notation format: 6.02214076 x 10²³. It's Avogadro's constant, which tells us approximately how many atoms or molecules there are in a mole of a substance. A mole is the number of grams of a substance that is equal to its molecular weight, or rather, the number of protons and neutrons in its component atoms or molecules.

It was originally indexed to the mass of Carbon-12, which has 6 protons and 6 neutrons. One mole of carbon-12 therefore weighs 12 grams.

It used to be that the number of atoms in a mole wasn't exactly known, because counting the number of atoms in 12 grams of carbon-12 isn't as easy as it sounds. Scientists had narrowed the range of potential values down to fall within 100 quadrillion atoms of 602,214,150,000,000,000,000,000 (602.21415 sextillion), but on 20 May 2019, the International System of Units (SI) body arbitrarily fixed the value of Avogadro's number to exactly 6.02214076 x 10²³. We still don't know exactly how many atoms there are in an actual mole of a substance, but we now have a close approximation that the world's measurement experts have officially endorsed.

Avogadro's constant can be found in more places than just chemistry. Astrophysicst Alex Howe's #megafavnumbers contribution points to where it is used in statistical mechanics.

At this writing, there are over 153 entries in the #megafavnumbers video list, which take on illegal primes, the monster, and the case of too many lottery winners, among others! If you've run out of binge-able videos to watch during the pandemic, why not add a bunch of videos about really big numbers to your playlist? We'll award extra points if you watch them in order from lowest to largest....

Labels: #megafavnumbers, math

We're going to tell a story about the history of the market for new homes in the U.S. almost entirely in pictures today. While all the charts we'll present cover the period from January 1976 through July 2020, most of the focus will be on the last several months of that timespan.

Let's start with the history of 30-year conventional mortgage rates:

The lower the interest rates, the more affordable a higher sale price for new homes can be, which can contribute to rising sale prices. Remember, home buyers aren't just buying a house - most are also buying a monthly mortgage payment they believe they can afford. With mortgage rates at all time lows, both average and median new home sale prices are rising toward all time highs.

With the Federal Reserve acting to lower interest rates to help stimulate the U.S. economy during the coronavirus recession, the number of new home sales has been rising. The following chart shows the trailing twelve month average of those sales, which smooths out seasonal volatility in the data.

The combination of higher average prices and rising number of sales means that the market capitalization of the new home market in the U.S. is rising.

The new home market in the U.S. is showing surprising strength during the Coronavirus Recession. The data presented in these four charts confirms that observation and helps explain why.

Labels: real estate

Arizona's situation with the coronavirus has continued to improve dramatically over the last four weeks. Arizona's rate of new infections has greatly slowed while deaths attributed to the coronavirus has begun falling rapidly.

These improvements can be seen in a trifecta of charts showing key trends in the daily progression of coronavirus infections in Arizona from 10 March 2020 through 25 August 2020. The first chart presents the state's daily progression tower chart that communicates the overall trends in the amount of testing, the incidence of newly confirmed cases of COVID-19, the number of hospitalized Arizonans and also the number of deaths in the state. The second chart shows the trend for the state's test positivity rate, which dropped below the 5% threshold in recent days, and the third chart shows the number of cases and deaths reported in the state each day. (Click here to see a full-size version of Arizona's trifecta of COVID-19 charts!)

We've been following the progression of COVID-19 in Arizona since the state became an epicenter for COVID-19, rivaling the state of New York for its share of population affected as it experienced a delayed first wave of SARS-CoV-2 coronavirus infections. While Arizona has seen a similar share of its population affected by COVID-19 infections, the state has been much more successful in limiting the number of associated deaths.

See for yourself in this chart!

Even though Arizona experienced a similar number of coronavirus cases per 100,000 residents as New York, it experienced a much lower rate of deaths, as the state did a much better job in protecting nursing home and long term care facility residents from exposure to coronavirus infections.

Arizona is experiencing a rapid reduction in the number of newly reported cases, thanks largely to the expansion of testing capacity at the labs conducting the vast majority of coronavirus testing in the state. That capacity came on line in early August, contributing to a plunge in newly reported confirmed cases as a large backlog was cleared. The effects of that expanded test capacity can be seen in a chart showing the daily number of newly reported confirmed COVID-19 cases in Arizona.

More significantly, Arizona is also seeing a rapid reduction in its number of deaths attributed to COVID-19. That reduction is confirmed a chart revealing the daily number of COVID-19 deaths in Arizona.

This chart confirms the effects of two actions taken by the state in responding to its surge in coronavirus cases and deaths in June 2020. Arizona turned the first corner to beating the spread of the coronavirus in the period corresponding to when a change might be expected to be seen following Governor Ducey's executive order allowing county officials to require masks be worn inside public venues. This action appears to have contributed to halting the upward trend in deaths that had been underway since Arizona lifted its statewide lockdown order in mid-May 2020, which accelerated in June thanks to the anti-police protests that occurred in the state from 28 May 2020 through 15 June 2020.

More significantly, Arizona Governor Doug Ducey's 29 June 2020 order to close public venues associated with a high risk of spreading coronavirus infections such as gyms, bars, movie theaters, and water parks appears to have contributed to the reduction in deaths that begins in the period that would be expected following that order. The governor later extended the order to continue into mid-August.

Governor Ducey also acted on 9 July 2020 to restrict Arizona restaurants to serving 50% of their dining capacity, but that action doesn't appear to have been as impactful as the governor's 29 June 2020 order.

The following table summarizes the major events indicated in these charts.

| Timeline of Events Affecting Rate of Spread of COVID-19 Coronavirus in Arizona | |||

|---|---|---|---|

| Event/Date | Description | Observed Change in Trends for Hospitalizations 11-13 Days Later | |

| A 19 Mar 2020 | California imposes statewide lockdown order | Significant change from rising to steady (bounded range) rate of hospitalizations. We think Arizonans effectively implemented practices to minimize their exposure risk to potential coronavirus infections, which then happened to show up as a change in trend immediately after Arizona implemented its own statewide lockdown order. | |

| B 31 Mar 2020 | Arizona imposes statewide lockdown order through April 2020 | Minimal change, new COVID-19 hospitalizations continue within bounded range. We think the main effect of the lockdown order was to standardize how Arizonans minimized their coronavirus exposure risks, which allowed the benefits to extend until the order was lifted, although that came at great economic cost. The lockdown would later be extended to 15 May 2020. | |

| C 15 May 2020 | Arizona lifts statewide lockdown order | Significant change from steady to rising rate of new cases, hospitalizations, and deaths. | |

| D 28 May 2020 to 15 Jun 2020 | Large scale political protests (Black Lives Matter/George Floyd/Anti-Police) | Change in rate of growth in rate of new hospital admissions as the protests greatly increased the risk and rate of exposure to the coronavirus for younger Arizonans, who are less likely to require hospitalization. Sharp increase in number of cases not requiring hospital admission. | |

| E 19 Jun 2020 | Governor Ducey's executive order allowing counties to require wearing masks in public venues begins to be implemented. | Significant change as new COVID-19 hospital admissions peak and begin to decline. Upward trend in deaths stop as state turns first corner toward improvement. | |

| F 30 Jun 2020 | Arizona imposes 'mini-lockdown' order | Significant change, with acceleration in decline of number of cases. Deaths peak before turning a corner and beginning a rapid decline. | |

| G 1 Aug 2020 | Expanded testing capacity comes online | Significant reduction in number of reported confirmed cases, as test labs speed processing and eliminate backlog. Continued downward trend. | |

One thing we haven't yet addressed is hospitalizations, where the purpose of these policies is to avoid the situation where the available capacity to care for coronavirus-infected patients might be exceeded. This final chart is taken from the Arizona Department of Health Service's COVID-19 data dashboard site, which confirms that state succeeded in flattening the curve of infections to keep it within manageable levels, as measured by the number of intensive care unit beds being used in the state.

Beds Available and In Use at Arizona Hospitals")

Data on the site confirms a similar story for all inpatient beds in Arizona, as well as emergency department beds. Arizona succeeded in flattening the curve for coronavirus infections and avoided the excess COVID-19 deaths that resulted from poor policy choices made by elected officials in other states.

Previously on Political Calculations

- Arizona's Coronavirus Crest in Rear View Mirror

- The Coronavirus Turns a Corner in Arizona

- A Delayed First Wave Crests in the U.S. and a Second COVID-19 Wave Arrives

- The Coronavirus in Arizona

- A Closer Look at COVID-19 Deaths in Arizona

- The New Epicenter of COVID-19 in the U.S.

- How Long Does a Serious COVID Infection Typically Last?

- How Deadly is the COVID-19 Coronavirus?

- Governor Cuomo and the Coronavirus Models

- How Do False Test Outcomes Affect Estimates of the True Incidence of Coronavirus Infections?

- How Fast Could China's Coronavirus Spread?

References

Arizona Department of Health Services. COVID-19 Data Dashboard. [Online Application/Database].

Maricopa County Coronavirus Disease (COVID-19). COVID-19 Data Archive. Maricopa County Daily Data Reports. [PDF Document Directory, Daily Dashboard].

Stephen A. Lauer, Kyra H. Grantz, Qifang Bi, Forrest K. Jones, Qulu Zheng, Hannah R. Meredith, Andrew S. Azman, Nicholas G. Reich, Justin Lessler. The Incubation Period of Coronavirus Disease 2019 (COVID-19) From Publicly Reported Confirmed Cases: Estimation and Application. Annals of Internal Medicine, 5 May 2020. https://doi.org/10.7326/M20-0504.

U.S. Centers for Disease Control and Prevention. COVID-19 Pandemic Planning Scenarios. [PDF Document]. Updated 10 July 2020.

Labels: coronavirus, data visualization, disaster planning

Apple (NASDAQ: AAPL) has been on a tear. It was almost two years ago that the company became the first trillion-dollar company in the S&P 500. Then, last week, it became the first $2-trillion company in the index.

As of the market close on Monday, 24 August 2020, Apple's market capitalization has reached $2.13 trillion, with the company accounting for over 7.2% of the total valuation of the S&P 500.

But here's the thing. It's not the only S&P 500 component with a market cap of $2 trillion or more. Because if you pay closer attention than the mainstream business media, the combination of the Class A (NASDAQ: GOOGL) and Class C (NASDAQ: GOOG shares of Alphabet, which is still better known as Google, has also surpassed $2 trillion. If you go by what MarketWatch reported for both classes of shares as of the close of business yesterday, the firm has attained a market cap of $2.14 trillion, making Alphabet just ever so slightly bigger than Apple.

These are estimates based on the reported float, or number of shares of both companies available to be traded by the public, at the end of their last business quarters. The number of shares is subject to change as companies may either issue new stock or, as in the case of Apple, may engage in share buybacks. (Apple has also announced plans for a 4-for-1 stock split that will take effect soon, but that will not affect its market cap estimate.)

Because of its aggressive stock buyback policy, Apple's market cap is almost certainly less than Alphabet's. It may also be less than $2 trillion, though we won't know until after Apple reports its next quarterly earnings.

Finally, if you're wondering how much $2 trillion is, if you could stack $2 trillion worth of $1 bills as high as you can imagine, they would reach nearly 120,000 miles into the sky, or a little over halfway to the moon.Previously on Political Calculations

Labels: data visualization, market cap, SP 500

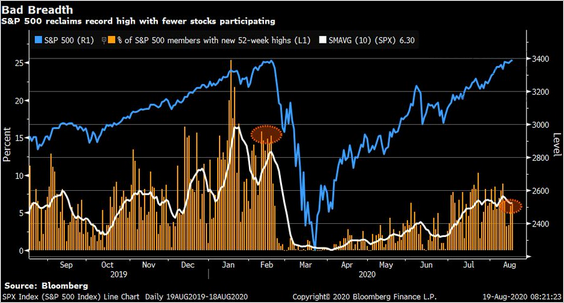

The S&P 500 (Index: SPX) closed at a new record high of 3,397.16 on Friday, 21 August 2020, the second time it set a new record during the week that was.

Which puts it in the lower half of the redzone forecast range in the alternative future chart, with the index' trajectory holding it just under the 3,400 level.

- Snapshot on 21 Aug 2020")

Despite setting new record highs, the rally the Fed has wrought has been remarkable for its lack of breadth, with just a single handful of stocks carrying the index to its new high. Or as Lance Roberts puts it, "the market has 'bad breadth'":

One of our primary concerns relating to the current elevation in the market has been extremely narrow participation. As Bob Farrell once quipped:

“Markets are strongest when broad, and weakest when narrow.”

There is little doubt that markets reek of “bad breadth.” As shown below, the market has achieved new highs with only a small percentage of the S&P 500 index participating.

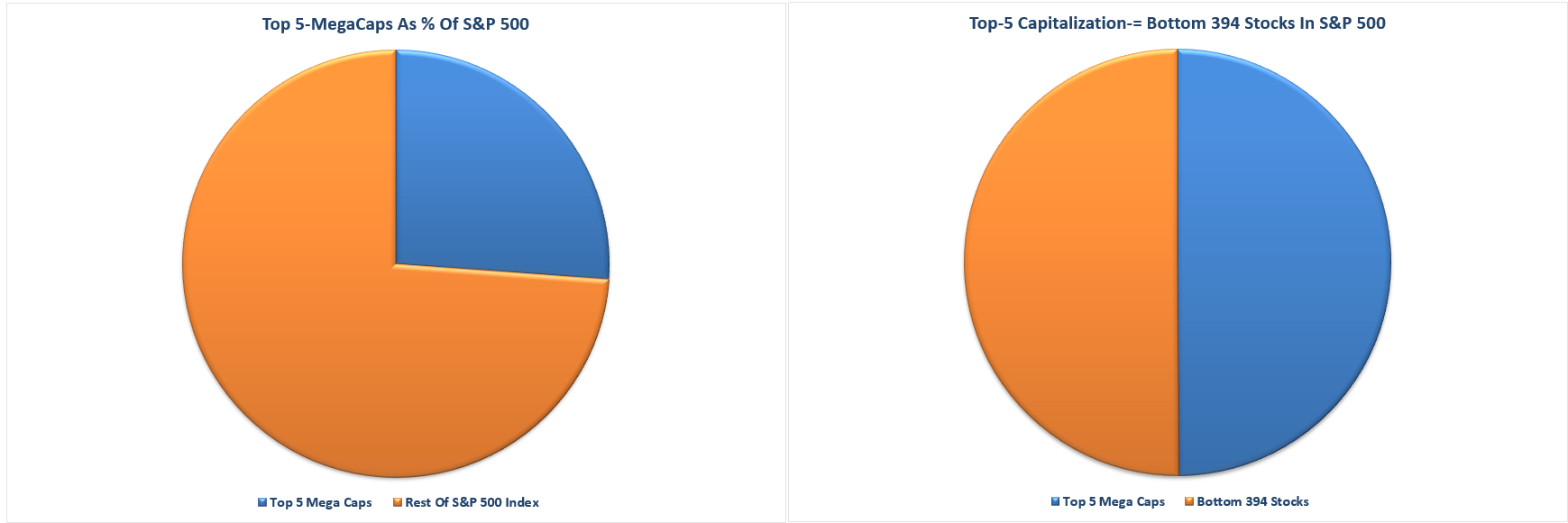

This “narrowness” is a result of the “passive indexing” effect on the markets which I explained in “Bulls Chant Into A Megaphone:”

“Currently, the top-5 S&P stocks by market capitalization (AAPL, AMZN, GOOG, FB, and MSFT) make up the same amount of the S&P 500 as the bottom 394 stocks. Those same five also comprise 26% of the index alone.”

“What investors are missing is that the top-5 stocks are distorting the movements in the overall index.

For each $1 put into each of those top-5 stocks, the impact on the index is the same as putting $1 into each of the bottom 394 stocks. Such is clearly not a true representation of either the market or the economy.”

If you really want to find the darkness lurking within the silver lining, you need to turn to ZeroHedge's take, which ends with the following cheery observation about the ratio of advancing/declining (A/D) stocks in the market:

... the last time we had a cluster of such negative A/D days with the S&P closing at all time highs was just days before the dot-com bubble burst.

But which you really need to click through to appreciate in all its gloomy glory. As for other gloom in the news, the week's headlines were somewhat short of imminent doom.

- Monday, 17 August 2020

- Daily signs and portents for the U.S. economy:

- Oil edges lower as suppliers try to hold line on output cuts

- As U.S. homebuilder confidence matches record high, mortgage delinquencies rise

- Bigger trouble still developing in Japan, Thailand:

- Instant View: Japan's economy shrinks at record pace as pandemic hits spending

- Thailand suffers biggest economic slump since 1998, government announces more stimulus

- Bigger stimulus still developing in China:

- China approves 11 fixed-asset investment projects worth $5.5 billion in July

- China central bank injects 700 billion yuan of MLF loans, rates steady for fourth month

- Nasdaq hits record high close due to tech rally

- Tuesday, 18 August 2020

- Daily signs and portents for the U.S. economy:

- Bigger trouble still developing in China, Eurozone:

- S&P warns of rising real rates risk to China's recovery

- German engineering exports plunge in second-quarter as pandemic takes toll: VDMA

- ECB minion has dark view of Eurozone bank health:

- https://www.reuters.com/article/us-usa-stocks-s-p500-graphic/big-tech-drives-sp-500-to-record-high-in-coronavirus-rally-idUSKCN25E2BO

- Wednesday, 19 August 2020

- Daily signs and portents for the U.S. economy:

- Oil slips as demand worries outweigh U.S. stocks draw

- Japan's exports tumble as U.S. demand collapses, order books shrink

- U.S. official sees 'real desire' for smaller coronavirus relief bill

- Fed minion promotes useful diversity at central bank, other minions anticipate more easing ahead, but Fed minutes seem to close door on Yield Curve Control for now:

- Fed's Bowman says diversity helps central bank policy

- Several Fed policymakers see more easing ahead to help brace economy

- Fed's Barkin says uncertainty is weighing on U.S. outlook

- Exclusive: Fed's Bullard - Wall Street 'about right' as U.S. muddles through virus risk

- Yield curve control: even less likely, for now

- Wall Street ends lower after Fed minutes highlight tough recovery

- Thursday, 20 August 2020

- Daily signs and portents for the U.S. economy:

- Oil falls 1% on OPEC+ oversupply, U.S. jobless data

- China, United States agree to hold trade talks, Chinese commerce ministry says

- Rise in U.S. weekly jobless claims clouds labor market recovery

- Bigger trouble brewing, bigger stimulus quantified in China:

- China's Supreme Court slashes ceiling of legal private lending rate

- China's outstanding loans to small businesses up 27.5% year-on-year by end-July

- Fed minion fixing to speak on Fed's future:

- Nasdaq closes at all-time high as strong tech sector offsets jobless data

- Friday, 21 August 2020

- Daily signs and portents for the U.S. economy:

- Oil falls 1% on sluggish coronavirus recovery, supply concerns

- China promised to follow Phase One trade deal, Pompeo says

- U.S. business activity surges to early 2019 levels: Markit flash PMI

- Congressional panel urges Fed and Treasury to take more risk with Main Street program

- Bigger trouble developing in the Eurozone:

- Euro zone economic recovery falters in August

- France delays launch of COVID-19 economic reboot plan to September

- S&P 500, Nasdaq end at records after upbeat business surveys

But wait, that's not all! Don't miss Barry Ritholtz' latest list of positives and negatives he found in the week's economics and markets news!

Emperor penguins have developed a unique strategy to cope with the bone-chilling cold winds of winter in Antarctica. They huddle together for warmth.

That may sound trivial, but it is how they huddle together that provides a case study in how a complex order can emerge from the seemingly chaotic behavior of individual penguins who are just looking to get comfortable in the cold benefits the entire flock. In the words of mathematician François Blanchette, what penguins do is an example of "organized chaos", where "every penguin acts individually, but the end result is an equitable heat distribution for the whole community".

But that's not all. In creating that equitable heat distribution, the huddles of penguins also take on a geometric order. Over time, they form oblong hexagonal shapes as individual penguins adopt an optimal packing efficiency that helps them maintain their body temperatures.

Penguins seem to know what mathematicians learned long ago: The densest packing of shapes on a plane is a hexagonal grid. According to Blanchette’s model, the birds arrange themselves as if they were each standing on their own hexagon in a grid. Most huddles start off as misshapen blobs. Wind flow and temperature around the huddle prompt a first penguin — typically the coldest on the windward side — to relocate. This penguin, known as the mover, waddles in search of new neighbors in the relative warmth of the huddle’s leeward side.

The mover selects the leeward-side boundary penguins with the least heat loss as his new neighbors, assuming his new spot without disturbing others. (He may or may not choose a spot that maximizes his new number of neighbors — in this model, all that matters to him is finding the penguins with the least heat loss.) As he settles in, one or more of his new neighbors may now be situated in the huddle’s interior, without ever having moved. Meanwhile, on the windward side, the mover may have exposed a formerly interior penguin to the boundary by leaving his old spot vacant.

As more penguins embark on heat-seeking missions, the huddle’s boundary is in constant flux. Over time, rough shapes in the huddle become defined. The original blob transforms into a regular geometric object: an oblong shape with straight sides and rounded ends.

Here is an image from Blanchette's 2012 paper with Aaron Waters and Arnold D. Kim that shows how a penguin huddle evolves over time as individual penguins move to pack themselves together as efficiently together as possible to regulate their body temperatures to produce the geometric order.

. Figure 2. Time progression of a model huddle")

The wildest thing about this paper's results is the authors' model appears to match what Emperor penguins do in real life. A 2018 paper by a team of researchers developed a remote-controlled observatory for behavioral and ecological research on emperor penguins confirms the emergence of the geometric order in their huddles.

... Daniel Zitterbart, a physicist at Woods Hole Oceanographic Institution, helped develop and install high-resolution cameras to observe undisturbed huddling behavior. Zitterbart’s team recently discovered which conditions cause penguins to huddle, and they are investigating the possibility that the penguins’ mathematical behavior may reveal secrets about colony health over time.

To the extent the mathematical model of huddling penguin behavior accurately predicts how real-life penguins behave, it can be very useful for scientists studying the penguin colonies because it may make it possible to divine information like how well fed the average penguin member of a colony is. For example, if the penguins start forming huddles at higher temperatures than the model would predict, it may indicate their collective diet before winter started wasn't sufficient for them to gain enough body fat to withstand Antartica's brutally cold environment.

References

Waters, Aaron; Blanchette, Francois; and Kim, Arnold D. (2012). Modeling Huddling Penguins. PLoS ONE. 7(11): e50277. DOI: 10.1371/journal.pone.0050277. 16 November 2012.

Richter, Sebastian; Gerum, Ricard Carl; Schneider, Werner; Fabry, Ben; Le Bohec, Celine; and Zitterbart, Daniel P. A remote-controlled observatory for behavioural and ecological research: A case study on emperor penguins. Methods in Ecology and Evolution. DOI: 10.1111/2041-210X.12971. January 2018.

Image credit: Photo by Martin Wettstein on Unsplash.

Labels: environment, math

The impact of the coronavirus pandemic that began in China continues to take a toll on the world's economy.

We can estimate that impact using the trailing twelve month average of the year over year change in the atmospheric concentration of carbon dioxide measured at the remote Mauna Loa Observatory. Here, we find that the rate at which CO₂ is increasing in the Earth's air has fallen from a trailing year average of 2.91 parts per million in December 2019 to a preliminary estimate of 2.61 parts per million in July 2020.

That change can be seen in the latest update to a chart showing the history of this measure and the timing of major economic recessions in the world since January 1960.

That decline of just 0.3 parts per million of carbon dioxide in the atmosphere translates to nearly $10 trillion reduction in the world's Gross Domestic Product. The default values in the following tool confirm the results of the math we have previously confirmed provides estimates of lost GDP in the right ballpark. If you're accessing this article on a site that republishes our RSS news feed, please click through to our site to access a working version of the tool.

With an estimated loss of $9.97 trillion worth of global GDP, the reduction in the pace at which the level of carbon dioxide is changing within the atmosphere represents approximately a 7.0% decline from the International Monetary Fund's purchasing power parity estimate of $142.0 trillion for 2019.

In early June 2020, the World Bank estimated the global coronavirus pandemic would shrink the world's economy by 5.2%, which works out to be a reduction of roughly $7.4 trillion worth of international GDP.

Both these figures are of a similar order of magnitude, so our estimate is still very consistent with those of established sources. And for what it's worth, the World Bank's estimate would be based on data through May 2020, while ours is based on data through July 2020. If you're looking for a single value that captures the most current, best single estimate available today, our estimated $10 trillion loss in world GDP since the SARS-CoV-2 coronavirus made its debut in Wuhan, China is a good number to reference.

References

National Oceanographic and Atmospheric Administration. Earth System Research Laboratory. Mauna Loa Observatory CO2 Data. [File Transfer Protocol Text File]. Updated 5 August 2020. Accessed 5 August 2020.

Cederborg, Jenny and Snöbohm, Sara. Is there a relationship between economic growth and carbon dioxide emissions? Semantic Scholar. [PDF Document]. 2016.

Previously on Political Calculations

Labels: coronavirus, environment, gdp, recession, tool

During the early months of the coronavirus pandemic in the United States, four states implemented and sustained policies that forced nursing homes and other long term care facilities to blindly admit patients who had been treated for COVID-19 infections.

The four states that actively engaged in this practice include:

- Pennsylvania, where the policy was in effect from 18 March 2020 to 12 May 2020.

- New York, where the policy was in effect from 25 March 2020 to 10 May 2020.

- Michigan, where the policy went into effect on 26 March 2020. [Update 13 October 2020: Michigan 'officially' ended its policy on 30 September 2020, though we suspect its 'de facto' end came in late April or early May 2020.]

- New Jersey, where the policy was in effect from 31 March 2020 to 13 April 2020.

There was a fifth state that very briefly adopted a similar policy, California, but since it quickly terminated its policy within a few days, we've omitted it from consideration altogether in this analysis.

We've visualized the percentage of COVID-19 deaths with respect to positive test results for the entire U.S. in a unique chart, where we've indicated the periods in which the policies that forced the admission of coronavirus-infected patients into nursing homes was in effect for the states of Pennsylvania, New York, and New Jersey (omitting Michigan, where we could not confirm if it has altered the policy it adopted on 26 March 2020). The chart shows a unique coincidence between the excessive number of COVID-19 deaths that occurred and the timing of when these states' coronavirus nursing home policies were in effect.

It is also remarkable how the upward trend in COVID-19 deaths stops rising and begins to fall after Pennsylvania, New York, and New Jersey stopped forcing nursing homes and long term care facilities to admit coronavirus patients without testing to verify if they were still contagious.

With the share of cumulative deaths attributed to COVID-19 stabilizing at approximately three percent of the cumulative total of confirmed cases, we consider higher percentages as representing an excessive number of deaths with respect to confirmed cases.

The following chart, taken from the COVID Time Series site that visualizes state-level data from the COVID Tracking Project, shows how the cumulative number of deaths attributed to COVID-19 in these four states has racked up through the coronavirus pandemic to date. Here, we see that these four states were significant contributors to the excessive COVID-19 deaths that were recorded during the first three months of the coronavirus pandemic in the U.S.

That timing coincides with the excessive COVID-19 deaths accumulated during the period where these states conducted their forced COVID-19 nursing home admission policies.

These admission policies are significant because elderly, sick Americans have proven to be the most at-risk of death from coronavirus infections, which was already well known at the time each of these states implemented their policies.

That these policies were sustained for as long as they were goes a long way to explaining why the U.S. saw such a large number of COVID-19 deaths during the period where these policies were in effect, where these states made an outsized contribution to the nation's COVID-19 death total. That other states refused to copy these policies, even as the viral infection spread in a delayed first wave, also helps explain why the ratio of cumulative COVID-19 deaths to confirmed cases nationally has fallen to roughly half the peak level recorded while these policies were practiced in Pennsylvania, New York, New Jersey, and Michigan. Most the other states have done far better than these four states in protecting the most vulnerable portion of their populations from the coronavirus.

Previously on Political Calculations

- Governor Cuomo and the Coronavirus Models

-

We reconstruct the information Governor Andrew Cuomo acted upon in panic as he chose to dump thousands of coronavirus-infected patients into nursing homes throughout the state of New York, where the infections then spread like "wildfire" among the portion of the population most at risk from it, greatly contributing to the state's outsized COVID-19 death totals. Also, we've maintained a timeline to track breaking news as the scandal of the "Governor Who Kills Grandmas" plays out.

- What Happened in New Jersey's Nursing Homes?

-

A very similar story to what happened in New York, but far worse because of New Jersey Governor Phil Murphy's desire to play Governor Cuomo's "Mini-Me". Then again, it is New Jersey, so what do you expect?...

Labels: coronavirus, data visualization, risk

Every three months, we take a snapshot of the expectations for future earnings in the S&P 500 (Index: SPX) at approximately the midpoint of the current quarter, shortly after most U.S. firms have announced their previous quarter's earnings.

The latest forecast for S&P 500 earnings through the end of 2020 suggests a slightly deeper earnings recession than the forecast from the Spring 2020 snapshot, showing the continuing drag from the Coronavirus Recession. At the same time, S&P continues to optimistically project a robust recovery for earnings in 2021.

The earnings forecast data suggests that the last three months of the coronavirus recession in the United States has been much less damaging to the earnings prospects of the firms that make up the S&P 500 index than its first three months. This snapshot captures the positive development of the earnings recession getting worse at a much slower pace, which is a precursor to it bottoming out and beginning to recover.

As you can see in the historical expectations for the S&P 500's earnings per share that are shown in the chart, S&P has a history of making optimistic projections. Changes in S&P's projections for 2021 will be something to watch in the next few months.

Data Source

Silverblatt, Howard. Standard & Poor. S&P 500 Earnings and Estimates. [Excel Spreadsheet]. 13 August 2020. Accessed 15 August 2020.

Labels: earnings, forecasting, SP 500

Welcome to the blogosphere's toolchest! Here, unlike other blogs dedicated to analyzing current events, we create easy-to-use, simple tools to do the math related to them so you can get in on the action too! If you would like to learn more about these tools, or if you would like to contribute ideas to develop for this blog, please e-mail us at:

ironman at politicalcalculations

Thanks in advance!

Closing values for previous trading day.

This site is primarily powered by:

CSS Validation

RSS Site Feed

JavaScript

The tools on this site are built using JavaScript. If you would like to learn more, one of the best free resources on the web is available at W3Schools.com.

Other Cool Resources

Blog Roll