How would you react if you were enjoying a nice day at the park, when suddenly, you realized that the Grim Reaper was flying behind you, following your every move?

And for those who insist on knowing how the evil magic is done, here is the video again, but explained by its creator....

HT: Core77. Happy Halloween!

Labels: none really, technology

Now that we've had to go to some effort to work out how the median household income in the U.S. has evolved over the last several months from payroll tax collection data, we're going to put those estimates to work today to get a better insight into the U.S. real estate market for new homes.

What we found suggests that September 2014 wasn't as positive as some news reports have claimed. Here, reports that the number of new single family homes reached a six year high in September would suggest that things are going swimmingly for the new home market in the U.S.

The problem is that the median sales price for new homes in the U.S. would initially appear to have fallen to $259,000 in September 2014 from a revised level of $286,800 in August 2014, an apparent decline of $27,800. While that initial $259,000 figure will almost certainly be revised higher, as the sales of higher priced homes during a given month often take longer to be incorporated in the official data, the combination of falling price and increased quantity would suggest that the median sale price fell because new home builders were forced to make big discounts because they found that they needed to move a relatively higher level of inventory.

We would have to go back to October 2010 to find a similar magnitude month over month decline in the raw data for median new home sale prices.

That decline in the median sale prices for new homes shows up when we account for the seasonality of the U.S. real estate market by calculating their trailing twelve month average and projecting the value against median household income:

That sudden decline may account for the sudden momentum by the political cronies of government-supported home lenders to significantly loosen lending standards for mortgages - in a way, it's like fanning the flames of a fading fire in attempting to get it to burn brighter for a little longer. We're going to quote Warren Meyer's full reaction to that change in policy, simply because we can't make the point any better:

97% Mortgages are 100% Insane

I am not sure there was ever any excuse for considering a 97% loan-to-value mortgage as "sensible" or "responsible." After all, even without a drop in the market, the buyer is likely underwater on day one (net of real estate commissions). Perhaps for someone who is very wealthy, whose income is an order of magnitude or two higher than the payments, this might be justifiable, but in fact these loans tend to get targeted at the most marginal of buyers.

But how can this possibly make sense when just 5 years ago the financial markets collapsed in large part due to these risky mortgages? Quasi-public, now fully public guarantors Fannie and Freddie had to be bailed out by taxpayers with hundreds of billions of dollars. There are still a non-trivial number of people trapped deep underwater in such mortgages, still facing foreclosure or trying to engineer a short sale after seeing the small bits of equity they invested swamped by a falling housing market.

But, here they go again: Fannie and Freddie, now fully backed by the taxpayer, are ready to rush out and re-inflate a financial bubble by making what are effectively nothing-down loans:

Federal Housing Finance Agency Director Mel Watt has one heck of a sense of humor. How else to explain his choice of a Las Vegas casino as the venue for his Monday announcement that he’s revving up Fannie Mae and Freddie Mac to enable more risky mortgage loans? History says the joke will be on taxpayers when this federal gamble ends the same way previous ones did.

At his live appearance at Sin City’s Mandalay Bay, Mr. Watt told a crowd of mortgage bankers that “to increase access for creditworthy but lower-wealth borrowers,” his agency is working with Fan and Fred “to develop sensible and responsible guidelines for mortgages with loan-to-value ratios between 95 and 97%.”

The incredible part is that the Obama administration is justifying this based on all the people still underwater from the last time such loans were written. The logic, if one can call it that, is to try to re-inflate the housing market now, and worry about the consequences -- never, I guess. Politicians have an amazing capacity to mindlessly kick the can down the road, where short-term is the next morning's papers and unimaginably far in the distant future is after their next election.

On the bright side, the eventual failure that will be blamed on the market is not being left to chance, nor is the great personal wealth being quietly accumulated by political insiders and their family members.

So at least the full extent of the stupidity involved has been catalogued for future reference.

References

Political Calculations. Divining Median Household Income from Payroll Tax Data. 29 October 2014.

Political Calculations. Supply or Demand: What's Driving the Price?. 21 November 2007.

Sentier Research. Household Income Trends: July 2014. [PDF Document]. Accessed 3 September 2014. [Note: We have converted all the older inflation-adjusted values presented in this source to be in terms of their original, nominal values (a.k.a. "current U.S. dollars") for use in our charts, which means that we have a true apples-to-apples basis for pairing this data with the median new home sale price data reported by the U.S. Census Bureau.]

U.S. Census Bureau. Median and Average Sales Prices of New Homes Sold in the United States. [Excel Spreadsheet]. Accessed 25 October 2014.

Labels: real estate

Can we use monthly payroll tax collection data to reasonably approximate the median income being earned by U.S. households?

That's the problem we were really seeking to solve when we found that payroll tax collection data is a lagging indicator of recessions for the U.S. economy, but is perhaps a real-time indicator of positive growth conditions.

The reason that's a problem is because our primary source for monthly median household income data, Sentier Research, has temporarily suspended its monthly reports, on account of extensive changes the U.S. Census Bureau has made in its monthly collection of data for its ongoing Current Population Survey (CPS). Sentier indicates that the changes, in which the Census is updating its sampling of the U.S. population to reflect the more up-to-date geographic distribution of the population recorded in the 2010 Census, are generating quite a lot of noise in the Census' monthly CPS data, which will take them time to sort out.

Because that's useful data, we wondered if there might be an alternative way to divine the median household income of U.S. households using other sources of data that are also reported on a monthly basis.

We immediately thought of the U.S.' Federal Insurance Contributions Act (FICA) payroll tax collection data as a good potential alternative source, since it represents the flat-rate taxation of wage and salary income. We then narrowed our focus to just the portion of those taxes represented by Medicare's Hospital Insurance (HI) tax, which in addition to applying to all wage and salary income and which, unlike Social Security's portion of payroll taxes, has been maintained at the same 2.90% of income since the early 1990s.

Before we continue, we'll note that the Affordable Care Act (ACA, more popularly known as "Obamacare") imposed an additional 0.9% Medicare tax on the wages, salaries and investment income of high income earners beginning in 2013. However, since all of those additional tax collections go straight into the general fund of the U.S. Treasury rather than to Medicare, the data that the Social Security Administration reports for its collection of Medicare's HI tax is based only on the 1.45% of income it collects from individual wage and salary earners and the additional 1.45% of income it collects from their employers.

Our next step was to determine if there is any sort of relationship between the federal government's HI tax collections and median household income. Since the HI tax collection data is volatile from month-to-month and seasonal in nature, we calculated the trailing twelve month average of the HI's monthly tax collection data and plotted it against Sentier Research's monthly median household income data, which goes back to January 2000 and extends through July 2014. Our results are graphed below.

All data in the chart are presented in terms of nominal (current) U.S. dollars.

We see that there's a pretty strong correlation between Medicare HI tax collections and Median Household Income, which really shouldn't be all that surprising since wages and salaries make up such a very large portion of household income. That means that we can use the payroll tax data to estimate median household data.

But it's not quite as easy as just running a linear regression on the data to get to what might be considered a precise figure, thanks to things like recessions and their aftermath or sudden growth spurts can cause the relationship to deviate onto a roughly parallel trajectory for an extended period of time.

For projections in the current day, it's coping with the sudden organic growth spurt that occurred in the U.S. economy in the latter half of 2013 for which we need to specifically make adjustments. Here, we find the situation where median household income actually dipped in the months of October and November 2013 while the amount of Medicare HI payroll tax collections surged, setting the overall trajectory of median household income onto a new path.

What happened at that time came in response to the harvest of record bumper crops of nearly every major agricultural crop grown in the U.S. in 2013. Here, we observe that median household income fell, while payroll tax collections increased, as a very large number of previously idle and relatively low-paid agricultural workers became employed. And it would seem that many of them have stayed employed.

To account for that shift in the employment pattern in the U.S., we've drawn a new, parallel trajectory to the overall trend from January 2000 through July 2014, which we'll use to project the median household income for each month since for which we have Medicare HI payroll tax collection data.

Doing that math, we obtain the following estimates of monthly U.S. median household income for each of the indicated months for which we have actual or projected data provided by the Social Security Administration.

| Projected Median Household Income Values for Given Level of Medicare Hospital Insurance Tax Collections | ||

|---|---|---|

| Month | Trailing Twelve Month Average of Medicare Hospital Insurance Payroll Tax Collections | Projected Estimate of Median Household Income |

| August 2014 | $18,931,813,603 | $54,105 |

| September 2014 | $18,964,894,435 | $54,164 |

| October 2014 | $19,008,977,769 | $54,243 |

It will be months before we know how close or how far off our projections of median household income are, but at least we now have an independent method of divining this data in the absence of, and until the return of, the actual data!

Data Sources

Sentier Research. Household Income Trends: July 2014. [PDF Document]. Accessed 11 October 2014. [Note: We've converted all data to be in terms of current (nominal) U.S. dollars.]

U.S. Social Security Administration. Social Security and Medicare Tax Data. [Online Database]. Accessed 11 October 2014.

U.S. Social Security Administration. Social Security and Medicare Tax Rates. [Online Document]. Accessed 11 October 2014.

Labels: data visualization, income, math, taxes

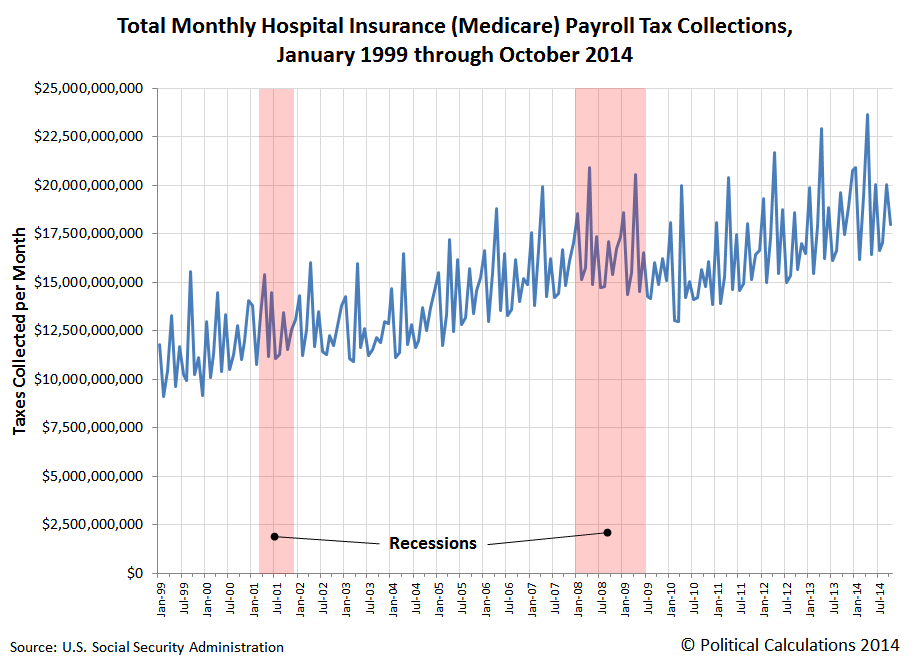

Can monthly tax collection data predict recessions?

That's a question we realized we could answer as we went about solving a different problem. In working on that other problem, we were looking at the U.S. Social Security Administration's data on the taxes it collects each month to fund Part A of the Medicare program (hospital insurance), where we noted that the amount of taxes collected showed a cyclical pattern - one that seemed to correspond to recessions.

That's significant because Medicare's Hospital Insurance tax is levied against all wage and salary income earned by Americans and has been fixed at a steady 2.90% (1.45% of total income paid by the individual wage or salary earner with another 1.45% paid by their employer as part of those FICA payroll taxes) since the early 1990s. And even though a there's a new 0.9% Medicare tax that has been imposed on the wage, salary and investment income of high income earners as part of Obamacare, unlike Medicare's hospital insurance tax, none of that money really goes to the Medicare program. It goes straight into the general fund of the U.S. Treasury instead.

That means that Social Security's data for its Medicare Hospital Insurance tax collections represents a simple, straight percentage of all the wage and salary income earned in the U.S. Which in turn means that we can perhaps use it as a decent indicator of the relative health of the U.S. economy.

Since there have only been two official periods of recession recorded since the early 1990s, which is all as far back as our data source goes, we focused just on the period since January 1999 to see if we can find any correlations between Medicare Hospital Insurance tax collections and the timing of recessions in the U.S. Here's our visualization of the raw data:

We see there's something there, but also that there's a lot of volatility from month to month, including seasonality in the data, with peaks in the data coinciding with quarterly and annual tax deadlines. To address those issues, we calculated the trailing twelve month average of the monthly Medicare Hospital Insurance payroll tax collections. The chart below shows what we found (the first data point, December 1999, reflects all the data from January through December of that year):

After this bit of analysis, we see that the payroll tax data for Medicare's Hospital Insurance tax is really a lagging indicator of the relative health of the U.S. economy when it falls into recession, which we see in the amount of taxes continuing to rise before stagnating and falling as recessions take hold. This observation is consistent with employers being slow to cut people from their payrolls or hours and pay during the early portion of official periods of recession.

But intriguingly, this data seems to also be a real time indicator of improving economic conditions, where employers act quickly to add staff when economic conditions demand it.

We can see that real time indicator at work in the latter half of 2013, when the U.S. economy experienced an organic growth spurt thanks to a record bumper crop of agricultural products, with the greatest growth occurring in the period from September through December, which corresponds to the harvest and export of major commercial crops in the U.S.

Through the projected tax collection data for October 2014, we don't see any similar sign of a surge in payroll tax collections, which suggests that there will not be a similar growth spurt in either incomes or jobs at the present time.

But also no sign of recession, which from what we can tell with the limited data available, wouldn't show up until well after a recession has officially begun.

Labels: recession forecast, taxes

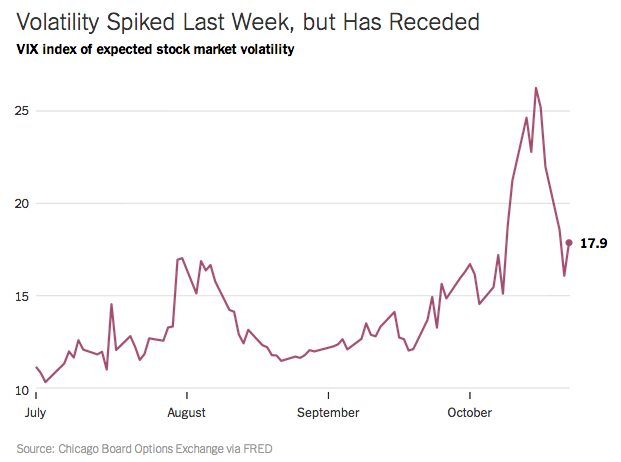

Last Friday, we had a bit of fun as we made a big deal out of our having correctly anticipated the course of the S&P 500 during the preceding week. The chart below, excerpted from The Upshot (via Barry Ritholtz), shows why that was such a big deal.

The ability to anticipate or cope with volatility is one of the major tests of any model of real world phenomena. In the case of our model of how stock prices work, there are two primary causes of volatility with which we're concerned:

- Special cause variation, where we observe changes in stock prices that are either consistent with identifiable shifts in the forward-looking attention of investors from one point of time in the future to another in setting their expectations of the future when making current day investment decisions, or that are the result of the reaction of investors to other identifiable factors that do not affect their fundamental expectations of the future, which we often describe as noise events.

- Common cause variation, where we observe variation, or typical levels of noise, that is driven by factors or frictions that are always present in the stock market.

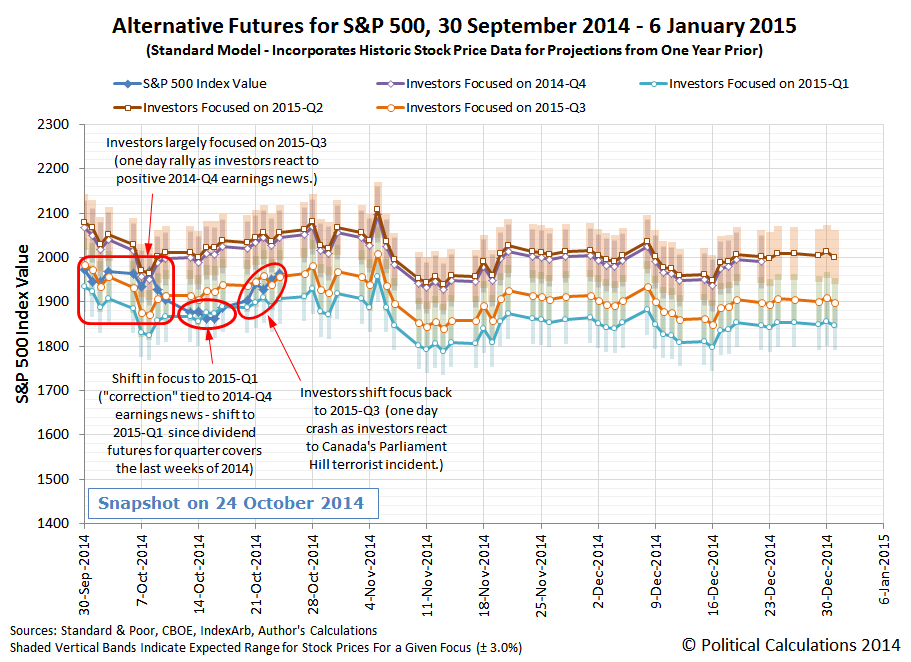

Our standard model has done well in addressing both kinds of variation, which we've observed in spades since October 2014 began.

Looking forward through the next two weeks, we would anticipate that in the absence of noise or an announcement from the Fed specifying that they will begin hiking short term interest rates in 2015-Q2, which would prompt a shift in focus, investors will remain primarily focused on 2015-Q3 in setting their expectations as they set stock prices.

Our model would appear to project a very short term dip in stock prices in this upcoming week, with a short rally in stock prices in the following week. These are actually artifacts of our use of historic stock price data as the baseline reference points from which we project the future trajectory of stock prices, which are the result of echoes from short term noise events of a year ago - much like the one day rally was on 8 October 2014 and also the one day dip of 22 October 2014. We would anticipate that the actual trajectory of stock prices will more closely connect the "dots" on the opposite sides of both projected "events".

Looking further forward, if the Federal Reserve were to more clearly indicate that 2015-Q2 will be the most likely future quarter in which it will begin hiking interest rates, it will have an advantage in doing so if it communicates that intent in early November 2014.

Here, we note that if investors have reason to remain focused on 2015-Q3, the most likely future trajectory for stock prices will be lower through the end of the 2014. But if the Federal Reserve succeds in shifting the forward looking focus of investors to 2015-Q2, stock prices will shift to a trajectory that is flat to higher than they are today, which is something that the Fed might desire if it wants to maintain the appearance that U.S. markets have confidence in its plans.

That would also be the worst possible thing that the Federal Reserve could do if economic conditions in the U.S. are such that delaying its plan to begin hiking short term interest rates is warranted. That could potentially set up the situation where stock prices would "correct" by at least 5% while costing the Fed a portion of its credibility.

It's going to be fun watching the Fed this month and next!

Analyst Notes

The main reason we've been taking such an apparently self-congratulatory tone lately is because we've nearly reached the successful end of the basic development work for our years-long stock price forecasting project. With the bulk of that work now behind us, we're going to be increasingly moving on to other things.

We plan to somewhat regularly post updates of our forecast model's performance through the end of 2014-Q4, but we would only periodically comment on the S&P 500's stock prices as events might warrant after that point.

We need you to watch the following video, in which Dave Hax describes how to freehand draw a perfect circle. Once you've seen how, we need you to duplicate his "target" pattern of the three concentric circles on a sheet of paper, making the innermost one as small as you can draw:

After you've drawn your target pattern, fill in the innermost circle to represent the eye of the target.

Then note that when it came to anticipating where stock prices were going this past volatile week, we hit all of our marks within that innermost circle. Again.

But then, it's been an easy week. As easy as drawing a perfect circle by hand.

Labels: none really

The unfortunate news of yesterday's Parliament Hill terrorist incident in Ottawa provides the background for a quick study of the impact that such events can have on the U.S. stock market. We classify these kinds of events as noise events, since they have no effect upon the fundamental drivers of stock prices, nor do they have any lasting impact upon stock prices.

But they can have a short term effect, which we'll attempt to quantify. To do that, we'll do an event analysis using the basic timeline that we've been able to put together from reports by The Globe and Mail, International Business Daily and CTV.

What we're looking for specifically in our event analysis is the point in time at which U.S. investors first came to appreciate the full seriousness of the incident, from which we can calculate the subsequent impact upon stock prices. Here, we'll be taking advantage of our previous observations that it only takes investors some two to four minutes to react to news that they were not previously expecting.

We've annotated the chart below showing the value of the S&P 500 stock market index on 22 October 2014 with the major news events documented by our timeline news sources.

The table below lists the major events indicated by the corresponding letters shown on the chart above.

| Timeline of Events for Canada's Parliament Hill Terrorist Incident on 22 October 2014 | ||

|---|---|---|

| Event | Time | Event Description |

| A | 9:52 AM EDT | First calls to Ottawa police in connection with the first shooting at Canada's National War Memorial, wounding Corporal Nathan Cirillo, who was guarding the Memorial's Cenotaph. The suspect then crossed the street to enter the Parliament Buildings. Reports of dozens of shots follow. |

| B | 10:12 AM EDT | Reports of shots fired in the Parliament Buildings. |

| C | 10:18 AM EDT | More reports of shots fired. Canadian MPs leave Parliament for safety. |

| D | 10:21 AM EDT | Male suspect, Michael Zehef-Bibeau, is reported deceased. Sergeant at Arms Kevin Vickers is later reported to have shot the assailant outside the MPs' caucus rooms. |

| E | 10:49 AM EDT | Rideau Centre shopping mall is reported to have been evacuated. |

| F | 11:00 AM EDT | Gunfire is reported near the Château Laurier hotel, near the Parliament Buildings. |

| G | 11:06 AM EDT | University of Ottawa is locked down. |

| H | 11:13 AM EDT | Château Laurier hotel is locked down. Parliamentary security locks down all Parliament Buildings. |

| I | 11:20 AM EDT | An 8-member police SWAT team enter Parliament's Centre Block on the run. |

| J | 11:50 AM EDT | Ottawa police confirm there were at least three separate shootings. |

| K | 12:10 PM EDT | International Business Daily posts the Globe and Mail's video of the exchange of gunfire between police and at least one suspect in the Parliament Buildings. This is likely the first venue through which U.S. investors were communicated the seriousness of the incident. |

| L | 12:12 PM EDT | U.S. markets begin falling in response to the incident (these changes are driven by speculation - not by changes in the fundamental driver of stock prices.) |

| M | 12:19 PM EDT | Victims injured in shooting incidents begin arriving at Ottawa Hospital. |

| N | 1:20 PM EDT | Corporal Nathan Cirillo is reported to have died. |

| O | 1:44 PM EDT | Rideau Centre shopping mall lockdown is lifted. |

| P | 3:45 PM EDT | University of Ottawa lockdown is lifted. |

The Parliamentary Buildings were still locked down when the market closed on Wednesday, 22 October 2014, with police continuing their investigation of the incident.

We see that it was the reporting of the exchange of gunfire in the Parliament Buildings at 12:10 PM EDT [K] that prompted the reaction in the U.S. stock market, as stock prices began falling as investors immediately adopted a more "safety"-oriented investing strategy - selling off stocks to capture recent gains. From 12:10 PM to the end of trading, the S&P 500 fell from 1946.16 to 1927.11 - a decline of 19.05 points, or just shy of 1% of the S&P 500's index value at the time U.S. investors learned of the seriousness of the event.

That's far less than the potential +/-3% range of the typical "noise" level that we expect for the daily variation in stock price prices that is built into our forecast model. Which is to say "hardly any impact at all." And because it's just noise, even that will quickly fade. Terrorism is the act of the impotent.

There has though been a very real loss. A much finer man than the Islamic terrorist assailant will no longer be among us, a man who died guarding a memorial to those who died in war long before him. And as did they, with honour.

Labels: SP 500, stock market

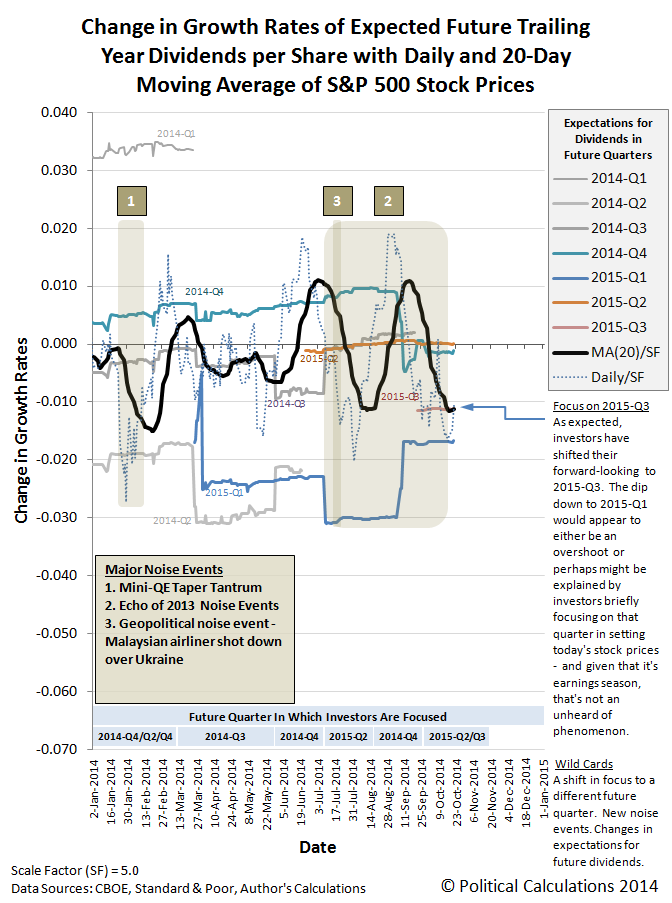

Since we're now outside of the anniversary period of 2013's U.S. debt ceiling crisis, the third and smallest of the major noise events of 2013, we're making the transition back to using our standard baseline model for use in forecasting and explaining changes in current day stock prices. Something that people like Catherine Rampell would not appear to believe is even possible.

Even though the period from 1 October through 17 October is somewhat affected by the echo effect's impact on our mathematical model of how stock prices work, it's pretty small in size. That's certainly true after we substitute the CBOE's dividend futures value for 2014-Q3 (of $9.895 per share) that we were previously using in our projections with S&P's final reported value for the quarter's dividends (of $10.023 per share). This change accounts for the upward shift in the trajectory associated with investors focused on the distant future quarter of 2015-Q3 compared to the version of this chart that we last posted nearly two weeks ago.

What we observe is consistent with stock prices either rebounding to the level that investors focused on 2015-Q3 would set them after having "overcorrected" for the misplaced rally of 8 October 2014, or perhaps more likely, briefly focusing on 2015-Q1, which could have been influenced by the earnings being reported by U.S. companies during the past week.

In both cases, to the dismay of the Rampells of the world, the current state of the U.S. economy carries no weight in the setting of stock prices, as investors are almost invariably looking beyond the present quarter as they make their investment decisions.

In fact, it's really pretty rare for investors to maintain any sort of focus on the current quarter in setting stock prices for any sustained period of time. There are really only two periods during the past six years where we've observed that sort of thing, which occurred when U.S. companies were either slashing their dividends in the current quarter, which played out as the crash from 26 September 2008 through 9 March 2009) or were acting to significantly boost their dividend payments to investors (15 November 2012 through 20 December 2012), where they were raiding the funds set aside to pay dividends in future quarters to beat the clock on the risk of major tax hikes as part of the Fiscal Cliff Crisis.

And since it's the changes in the growth rate of dividends that are directly proportional to the changes subsequently seen in the growth rate of stock prices as they respond to this fundamental signal as investors collectively focus on particular points of time in the future in making their investment decisions, let's take a look at what those expectations specifically are:

Looking forward, here is the level of dividends for the S&P 500 that investors are currently expecting to be paid in each of the following future quarters (according to the CBOE's dividend futures contracts as of 21 October 2014):

- 2014-Q4: $9.886 per share (*)

- 2015-Q1: $10.743 per share (*)

- 2015-Q2: $10.619 per share

- 2015-Q3: $10.712 per share

(*) All these values are based on dividend futures contracts, which run from the end of the preceding futures contract on the third Friday of the month ending the preceding quarter through the third Friday of the month ending the indicated quarter, and which project the dividends per share that will be paid out over that interval. These values will not match those reported by Standard and Poor for the S&P 500, since they report the dividends paid from the end of the month for one calendar quarter to the end of the next. Because of that difference, and because a lot of companies pay out their largest dividends before the end of the year, look for significant discrepancies between the CBOE's dividend futures and S&P's reported dividends for Q4 and Q1, with lesser adjustments for Q2's and Q3's dividends.

What these values do however tell us is that investors are expecting flat to lower dividend growth once we're in 2015. Which is why stock prices are most likely to head sideways or lower in the absence of an improving economic situation in the future that would prompt companies to boost their dividends in those future quarters.

What's more, the Federal Reserve shares our basic assessment, which we discovered in the reporting on the one topic that could suddenly cause investors to focus on the current quarter of 2014-Q4 in setting today's stock prices:

Mr. Bullard did not say he definitely wanted to extend the bond-buying program. No other Fed official has offered such speculation, and three—Boston Fed President Eric Rosengren, San Francisco Fed President John Williams and Dallas Fed President Richard Fisher—said in recent days they expect to end the purchases at their meeting Oct. 28-29.

The Fed’s policy committee has said recently the bond program would end this month. Barring a really tumultuous final 10 days of October, the panel “will almost certainly make that forecast come true,” analysts at Wrightson ICAP said.

More broadly, Fed officials routinely reject the idea they target stock prices in their policy deliberations. To the extent an equity fall would influence policy makers, it would have be very sharp and threaten to destabilize the financial system and the broader economy.

No comments from Fed officials over recent weeks have suggested officials are overly alarmed about what’s been happening in markets. Mr. Fisher even welcomed the declines as a sign markets are pricing equities in better alignment with the economy’s fundamentals.

WSJ reporter Michael Derby forgot to add the words "going forward" to the end of that last sentence, because those are the economic fundamentals that matter where stock prices are concerned. For people who pay attention to stock prices, the present is only where we live.

Labels: chaos, dividends, forecasting, SP 500, stock market

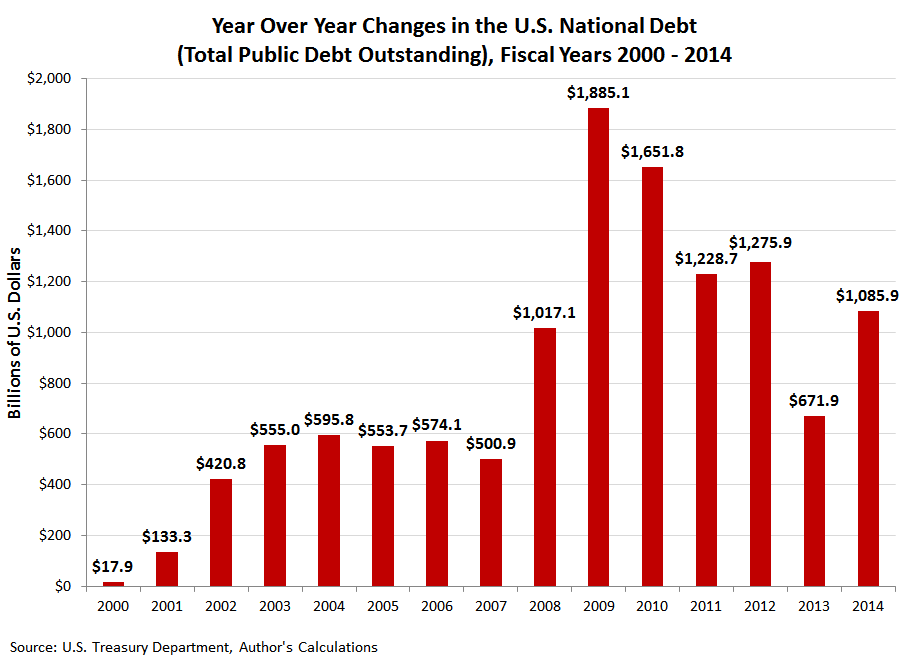

Who were the major holders of debt issued by the U.S. federal government as of the end of its 2014 fiscal year?

The preliminary answer of who owns the $17.860 trillion in debt issued by the U.S. federal government as of 30 September 2014 is presented graphically below:

The data for foreign holdings will be revised over the next six months. We anticipate that the holdings indicated for Belgium will be shifted to other foreign entities, given that nation's role as an international banking center.

Since FY2013

Since the end of the U.S. government's 2013 fiscal year on 30 September 2013, the total public debt outstanding for the U.S. government has increased by $1.086 trillion (or to agree with the units shown on our chart, $1,086 billion). That would mark the sixth time in the last seven years that the national debt of the United States has expanded by more than $1 trillion dollars per year - double the typical half trillion a year increases that were viewed as a major problem prior to Barack Obama's presidency.

The $1.086 trillion increase in the total national debt for Fiscal Year 2014 is all the more remarkable because the U.S. Treasury Department just bragged that the federal government's budget deficit for FY2014 was $483 billion.

Oct 15 (Reuters) - The U.S. budget deficit fell by nearly a third to $483 billion in fiscal 2014, the lowest level since 2008, as a quickening economic recovery boosted tax collections and spending grew only modestly, the Treasury Department said.

The deficit, down from $680 billion last year, was the lowest since a $459 billion budget gap in fiscal 2008, which was followed by four straight years of $1 trillion-plus deficits in the wake of the financial crisis.

U.S. Treasury Secretary Jack Lew and White House Budget Director Shaun Donovan hailed the data on Wednesday as a "return to fiscal normalcy" as the 2014 deficit fell to 2.8 percent of gross domestic product. That was the lowest since 2007 and a smaller share of the economy than the annual average for the last 40 years.

Somehow, the U.S. federal government managed to borrow and spend an additional $603 billion, above and beyond the official budget deficit of $483 billion claimed by the Obama administration, in order to cause the national debt to increase by more than one trillion dollars in one year.

How Could That Happen?

Part of the answer lies in the debt ceiling debate during 2013, which ultimately led to the partial federal government shut down for the first 17 days of the 2014 fiscal year, from 1 October 2014 through 17 October 2014.

Here, U.S. Treasury Secretary Jack Lew artificially kept the U.S.' total public debt outstanding from increasing above the statutory debt ceiling by shifting around the portion of debt held by U.S. government entities, such as Social Security's Trust Fund and the U.S. Civil Service Retirement Fund - giving them I.O.U.s as he redirected funds intended for them to instead allow the U.S. Treasury to continue rolling over the debt it owes to the public.

The reason the U.S. government had to go through a partial shut down is because those trust funds didn't have enough money to keep the shell game going until the debt ceiling was increased. When it finally was, the U.S. government "owed" some $328 billion to "itself". Which it promptly rushed out to borrow in Fiscal Year 2014.

That's also why the increase in the national debt for FY2013 seems so low. $328 billion of the debt that should have been recorded in that year was actually recorded in FY2014.

That means that the U.S. national debt increased by $758 billion in FY2014, $275 billion more than the official amount of the U.S. Treaury's claimed $483 billion budget deficit.

We're still waiting for the official explanation of that fiscal discrepancy.

Data Sources

Federal Reserve Statistical Release. H.4.1. Factors Affecting Reserve Balances. 1 October 2014. [Online Document]. Accessed 17 October 2014.

U.S. Treasury. Major Foreign Holders of Treasury Securities. Accessed 17 October 2014.

U.S. Treasury. Monthly Treasury Statement of Receipts and Outlays of the United States Government for Fiscal Year 2014 Through September 30, 2014. [PDF Document].

Labels: national debt

Since the S&P 500 is behaving so predictably, and because we just visited the topic on Thursday, 16 October 2014, we thought we'd take this opportunity to revisit how the stock prices of the S&P 500 behaved in the third quarter of 2014.

Our first animated chart shows how stock prices behaved with respect to our standard baseline model, in which we incorporate the historic stock prices of one year earlier as the base reference points from which we project stock prices in the near term future:

Since we knew coming into the quarter that our standard baseline model's projections would be skewed off as a result of what we call the echo effect, where the echoes of past noise events show up in our current day projections, we developed our rebaselined model, in which we exchanged the historic stock price data of a year ago for the historic stock data of two years ago - a period of time that was relatively free of the kind of noise events that can throw off our projections of future stock prices.

That simple change produced very good results, as demonstrated in the animated chart of our rebaselined model for the third quarter of 2014:

All in all, if you knew how far forward investors were looking in setting today's stock prices, and also when they were shifting their attention from one point of time in the future to another, 2014-Q3 was a pretty predictable quarter.

Speaking of which, let's look under the hood at the fundamental driver of stock prices: the changes in the rates of growth of dividends expected at discrete points of time in the upcoming future:

Mind the notes in the margin of our expectations chart.

On a final note, we'll observe that the projections of our rebaselined model will begin to skew off from the actual trajectory of stock prices as it will be affected by the echo effect beginning in November, thanks to the two year anniversary of the noise events that resulted from the outcome of the 2012 U.S. election. The cool thing is that we now have the ability to effectively work around that kind of challenge in using our analytical methods, which is really what we demonstrated during the third quarter of 2014.

To find out more, follow the links below....

Previously on Political Calculations

What if income inequality theorists got their way and stopped income inequality from ever increasing? What would be the result of that kind of achievement?

We came across the results of a unique experiment that was conducted nearly 100 years ago that answers the question, where a predefined level of income inequality was strictly enforced upon a small group of individual laborers with an outcome that permanently affected not just their jobs but also a national institution.

The experiment was unknowingly conducted by the professional baseball team owner Charles Comiskey, who after assembling "the best team money could buy", ultimately produced the most significant act of corruption in American sports history as a direct result of his strict enforcement of a policy of income equality upon his players regardless of their talent or individual contributions to the team's success: the Chicago Black Sox Scandal, in which a number of players on the 1919 Chicago White Sox deliberately lost the 1919 World Series to the Cincinnati Reds in return for payoffs from professional gamblers looking to gain from advance knowledge of the outcome.

Bruce Lowitt describes how the equality of income imposed by Charles Comiskey actually generated the worst possible outcome for everyone involved:

There was good reason the Sox were susceptible to the lure of quick money. They were among the American League's best players but Charles Comiskey paid most of them no more than the worst. The promised bonus for winning the 1917 pennant was a case of cheap champagne. Before the 1919 season, Comiskey promised Cicotte an extra $10,000 if he won 30 games. When Cicotte reached 29, Comiskey benched him. Player resentment was rampant.

Here, we see a prime example of the extreme penalty that Comiskey imposed upon one of his star players, pitcher Eddie Cicotte, to ensure that he would not ever be paid any more than any other player on the team, as Comiskey effectively imposed a 100% marginal income tax upon Cicotte as he came too close to becoming too successful in Comiskey's eyes.

What happened in response to that event would ultimately and permanently change America's national pastime as that achievement in preventing an increase in income inequality inspired acts of extreme corruption by eight players on the team, who wanted to have their pay reflect their real relative level of productivity and contribution to the team's success. And by "extreme corruption", we're not kidding. They threw the World Series, deliberately losing to the Cincinnati Reds in return for payoffs from professional gamblers.

But what's really curious is what happened after the World Series ended, because it was some time before the scandal was sorted out. Here, seven of the players involved in the scandal were signed to new contracts with the White Sox to play for the team in 1920, the year after the scandal, where they received anywhere from a 21% to a 100% increase in their previous year's salaries.

That's an especially curious thing because it is clear that Charles Comiskey was aware that the seven players had very likely deliberately lost the 1919 World Series before the contracts were negotiated. He could have refused to negotiate with the players suspected of corruption, but instead, he recognized that his previous policy for more equalized player pay was an abject failure and gave in to the greater level of income inequality demanded by the players in return for their real contributions to the team's success.

In 1919, the salaries for these seven players had ranged between a low of $2,750 to $6,000, a spread of $3,250, with the top income set at 218% of the income of the lowest paid player involved in the scandal. But in 1920, the player's incomes ranged from $3,200 to $10,000 (for Cicotte, who was paid $5,000 in 1919): a spread of $6,800, more than double what it had been in 1919, with the top income growing to be 312% of the lowest.

The Chicago White Sox went on to finish second in the American League in 1920, as the team's hitting and pitching was strong, finishing just two games behind the Cleveland Indians who had a stellar year. Increasing the income inequality among the team's players did not harm their performance as they achieved honest success - even winning eight more games than they had in the 1919 season (the 1920 season was 14 games longer than the 1919 season).

That's the benefit of increasing income inequality - a more honest system for rewarding the real contributions of the most productive members of a society. The penalties imposed by a system that rigorously imposes equality will almost invariably lead to corruption.

After the 1920 season, the news of the scandal broke break wide open, with the ultimate outcome that the eight Chicago White Sox players who had participated in the conspiracy to deliberately lose the 1919 World Series were banned from the sport of baseball for life, as the league's new, indepedent commissioner took actions to eliminate the potential influence that gambling could have in order to boost the sport's integrity.

But that is a whole separate issue from what really caused the scandal!

Labels: income inequality, sports

This may surprise a lot of people, mainly because it stands in such contrast to the work product of their journalistic peers, but a lot of financial reporting is pretty well done.

But even financial journalists don't quite get the stories they cover 100% right. We have a great example of that today, featuring some really good reporting by Michael S. Derby of the Wall Street Journal, in which he does an excellent job describing why the stock market is selling off, but ends up putting the cart before the horse.

A world-wide equities sell off is driving investors to expect the Federal Reserve will wait longer to start raising short-term interest rates from near zero.

Participants in the fed funds futures market, where investors go to bet on possible movements in the Fed’s benchmark federal funds rate, shifted on Wednesday to project the central bank will begin raising interest rates sometime in the late third quarter or perhaps the fourth quarter of 2015.

Markets now see almost no chance of a Fed increase in rates coming next September, down from even odds a few weeks ago, said TD Securities economist Millan Mulraine in a note to clients. He noted investors are now putting a 50-50 chance on the Fed raising rates in October, and a 63% chance the move comes at the 2015 December Fed policy meeting.

The shift in market expectations comes as Fed officials are debating when to start raising rates. Several Fed officials expect lift off by the summer of 2015. Some want to move sooner and others want to wait until 2016.

Good reporting, but Derby gets it completely backwards at the very beginning. The sell off in stock prices most certainly did not drive investors to start expecting that the Fed would delay hiking interest rates until later in 2015. Instead, it is completely the other way around. The change in expectations that the Fed would delay hiking interest rates in the U.S. is what has caused stock prices to fall.

More specifically, that shift in expectations started to take place on Monday, 13 October 2014, and may be fully attributed to a speech that Federal Reserve minion Charles Evans gave to the National Council on Teacher Retirement on the subject of Monetary Policy Normalization: If Not Now, When? The timing of Evans' speech, and the dissemination of its content among Wall Street traders throughout the afternoon, directly coincides with the sudden shift of investors from focusing on 2015-Q2 in setting today's stock prices, to instead focus their attention on the more distant future quarter of 2015-Q3.

Here is what we noted in the update to our regular Monday post on that sudden shift in expectations later that day:

Update 13 October 2014, 8:20 PM EDT: Today's market action is what a shift in focus looks like - where investors suddenly shift their focus from one point of time in the future to another. Or, in terms of our rebaselined chart, from 2015-Q2 to 2015-Q3:

As for why investors shifted their focus to 2015-Q3, well, that's easy. One of the minions at the Federal Reserve indicated that economic weakness would lead the Fed to delay those interest rate hikes, which for the Fed's game of expectations, had been set to occur in the middle of 2015. With evidence of a weakening economy in the present mounting, it wouldn't take much for investors to shift their attention further forward in time as they could reasonably believe the Fed will be forced to delay.

It's a small change, but one with an amplified impact upon stock prices given the nature of how they work.

Remarkably, stock prices are still within our forecast range for 13 October 2014 assuming that investors had been focused on 2015-Q2 in setting today's stock prices - we've gone from one extreme to the other in just a matter of days. Whether this change is just a temporary noise event or actually a sustained shift in focus will become evident over the next several days.

Update 14 October 2014 8:06 AM EDT: From the WSJ - Despite Mixed Risks in U.S., Rate Timing Hasn't Shifted Much. Indeed!

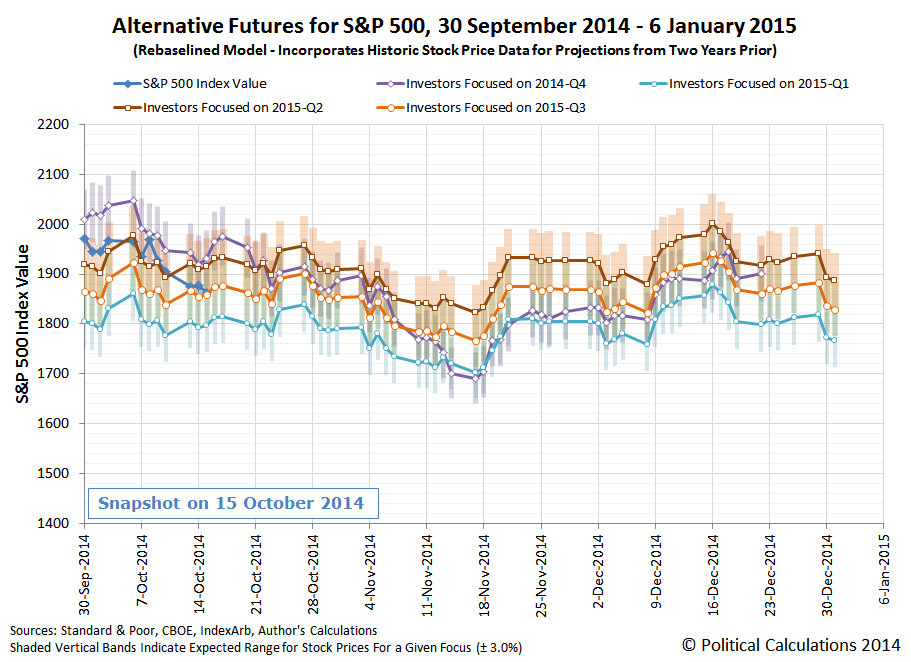

We've now had the next several days to see if that shift would be sustained. It has. In fact, despite one of the more volatile days in recent market history, the S&P 500 closed at a value that is fully consistent with investors having shifted their forward-looking focus to 2015-Q3. At least, according to our rebaselined model of how stock prices work:

Up until Monday, the S&P 500 was largely tracking along with the trajectory associated with the expectations for 2015-Q2. In the previous weeks, that had meant a relatively steady decline in stock prices, with the exception of a very short-lived positive noise event on Wednesday, 9 October 2014, when investors were briefly distracted by a bright shiny object.

And then, Chicago Fed minion Charles Evans gave his speech, basically giving investors permission to anticipate that the recent onset of negative economic news indicating a deteriorating situation for the U.S. economy would lead the Fed to delay hiking short term interest rates until 2015-Q3, and that was all it took for stock prices to fall to the level they have.

In case you're wondering, it's having to cope with events like this that inspired us to include each of the trajectories that the S&P 500's stock prices are most likely to follow given how far forward in time investors are looking as they make their investment decisions today on our forecast charts.

So yes. It's almost as if we predicted it! Because we did. Because we can.

What we can't do, except in certain limited circumstances, is to anticipate in advance when such shifts in focus will occur. That aspect of how stock prices behave actually is random. It's a good thing that those factors are such a small part of what really drives stock prices.

In the meantime, even though it wasn't always true on 15 October 2014, by the closing bell, order was maintained in the stock market.

But will that last for very long? The suspense is terrible. We hope it will last!

On a closing note, looking back at the trading day that was, we can't help but think of Chicago Federal Reserve President Charles Evans' role in unleashing all that volatility. It is as if he were the very reincarnation of Mrs. O'Leary's cow....

Something strange is going on with young adults in the U.S. job market.

In July 2014, the seasonally adjusted number of Americans between the ages of 20 and 24 reached 13,976,000, just 25,000 shy of the 14,001,000 figure recorded in November 2007, when the level of total employment in the U.S. peaked just ahead of the recession.

In the following two months, some 155,000 young adults have been squeezed out of the ranks of the employed in the U.S., reversing the trend of improvement for that particular age demographic. That stands in considerable contrast with the employment situation for U.S. teens, whose numbers have held steady since October 2009, and adults Age 25 or older, whose numbers have been increasing in recent months.

Hopefully, the jobs report for October 2014, which will be released next month, will shed more light on this situation. Until then, if you have any theories as to why the seasonally adjusted U.S. job market has turned south for this particular age group, now would be a good time to trot them out.

Labels: jobs

It's wrong to use direct statistical analysis to describe how stock prices behave for any really long period of time. Mostly because it is only valid to apply those methods when certain conditions exist, when the market might be described as being orderly, or if you really like mathematical puns, when the market is exhibiting "normal" behavior.

For the current stock market, those conditions have existed since 4 August 2011. Let's have a look.

Looking at the overall statistical trajectory of stock prices at this scale, and applying what we know about the fractal nature of stock price changes, the recent three standard deviation drop in stock prices since peaking on 19 September 2014 should be considered something of an early warning signal, as it suggests that the present state of order in the stock market is at a greatly increased risk of breaking down.

But there is no guarantee that it actually will, which is the curse of statistics-based analysis. You can simply observe the chart and see when similar early warning signals were sent without order breaking down, which would be indicated if stock prices either rose above or fell below the outermost (red dashed) statistical trend lines shown in the chart above, which are positioned at a distance of three standard deviations away from the central trend trajectory.

If you did want to make an investment decision related to the change in stock prices, you would wait until they definitively crossed one of those two curves to avoid the risk of acting too soon and losing out on potential gains while racking up unnecessary transaction costs.

For now, the more-than-two standard deviation shift is simply an indication that you ought to pay closer attention to what stock prices and doing and really ought to have some sort of strategy worked out for what you will do should the current state of order definitively break down (say if the S&P 500 suddenly dropped to close below 1850).

Because, when the conditions exist that make this kind of analysis appropriate, it can be an exceptionally valuable tool for making investment decisions when it matters most.

When you can still do something about it.

Update: 15 October 2014 9:41 AM EDT: You can't say you weren't warned. As Scooby Doo might say, "Ruh roh!"

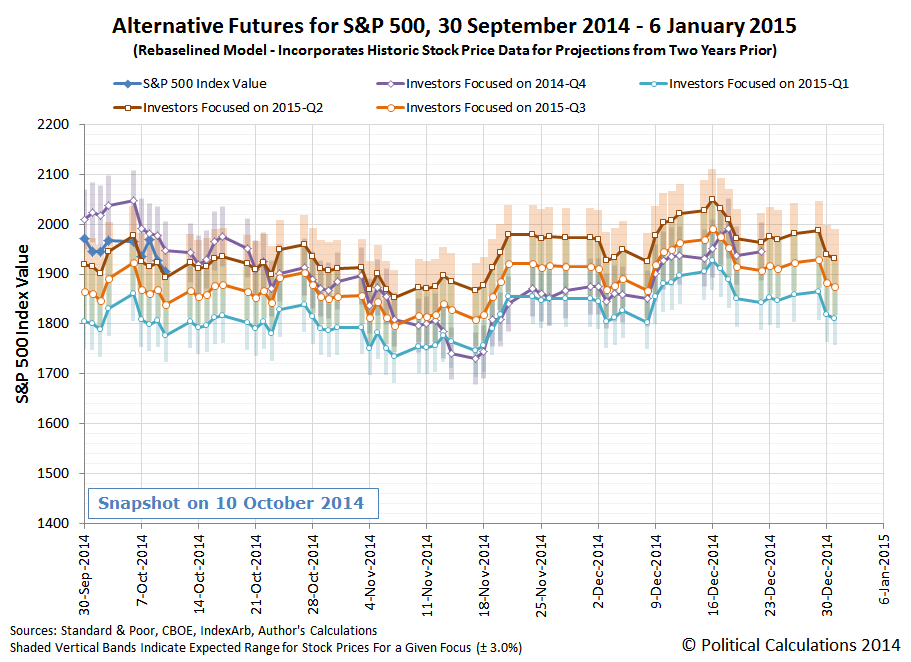

At the beginning of last week, many hours before the opening of the stock market on Monday, 7 October 2014, we did something that nobody else can do: we correctly anticipated where the S&P 500 would close on each and every day of the week within a narrow margin of error using our rebaselined model of how stock prices work. Here is how we closed that post:

Basically, in the absence of a shift in investor focus to a different point of time in the future or new noise events, the market is most likely to move sideways as stock prices largely keep pace with the expectations associated with the future associated with 2015-Q2. Which makes sense because that's the quarter in which the Federal Reserve is most likely to start messing around with short term interest rates.

Now, here's the updated version of the chart showing what our rebaselined chart forecasts for the likely trajectory of stock prices depending upon how far forward in time that investors are looking in setting their expectations:

What's important to know is that what we're really doing is forecasting the most likely range into which the S&P 500's stock prices will fall, which is indicated by the shaded, colored vertical bands shown on the chart for each of the future points of time to which investors might focus upon in setting their expectations. Although we have connected the midpoints of these ranges with colored lines, the ranges are what we are really forecasting.

And last week, we would appear to have nailed it. Again. Even with the surprise Fed September 2014 minutes rally on Wednesday, which was really just a very short duration noise event, which we recognized at the time, as stock prices remained within the typical level of noise that we can expect on a day-to-day basis. Let's take a closer look at the market action of the past two weeks:

What we do in charting the future trajectory of stock prices is complex, but not difficult. Which we point out now because we're about to make things a bit less complex for ourselves over the next couple of weeks.

The reason why is because we are finally coming up to the end of the series of large scale noise events that took place during the summer and early fall of 2013, for which we recognized ahead of the fact that our standard model, which incorporates the historic stock price data from a year ago in setting the baseline reference points from which we project future stock prices, would be ill-equipped to handle. The chart below illustrates each of the noise events that threatened to wreck our ability to accurately project the future trajectory of the S&P 500 (shown as the purple-shaded vertical bands shown on the chart):

Over the past year, we developed two different methods for coping with the echo effect in our projections. The first, where we attempted to filter out the echo effect, while having some initial success, ultimately turned out to be a failure. Our second attempt, where we rebaselined our historic stock price reference points, as the results above demonstrate, has proven to be much more successful.

And now, we're nearly to the end of the period of time for which we needed to develop it. Although we're still not quite out of the anniversary period for the third major noise event of 2013, we would anticpate that the following chart will become increasingly relevant over the next several weeks, as the actual trajectory of stock prices should converge with one of the alternative trajectories associated with the expectations for the sustainable portion of earnings (a.k.a. "dividends) at different points of time in the future.

If we had to interpret the chart based upon our standard model today, we would say that stock prices are largely keeping pace with the expectations that investors have for 2015-Q3, but that's without taking the echo effect into account. We'll have to see how things settle out over the next weeks to conclusively identify that future quarter as the focal point for investors.

That period of time is also consistent with the idea that the Federal Reserve will hold off until the middle of the next year to begin hiking short term interest rates, but will likely wait until the third quarter of 2015 to do so until the U.S. economy has had time to recover from the weakening economic situation at the present time.

Previously on Political Calculations

We've been working on how to crack the echo effect in our S&P 500 forecasting method since November 2013. The posts below, presented in reverse chronological order, describe our experience in that endeavor to date as we've worked out how to compensate for the echo effect in real time.*

- The S&P 500 Before the Echo Event Ends - 13 October 2014

- Almost Perfectly Predictible - 8 October 2014

- The Sideways S&P - 6 October 2014

- Split Expectations for the S&P 500 - 29 September 2014

- No Surprises for the S&P 500 - 22 September 2014

- Expectations Shift for the S&P 500 - 15 September 2014

- A Big Ball of Chaos - 4 September 2014

- Tracking Along wit the S&P 500 - 25 August 2014

- Echoes Off with the S&P 500 - 18 August 2014

- In Which We Take On a Pagan Religion - 11 August 2014

- Taking the Fork in the S&P 500's Future - 1 August 2014

- Compensating for the Echo Effect - 28 July 2014

- Shooting Down the Stock Market - 21 July 2014

- Are Investors Nearsighted or Farsighted? - 14 July 2014

- A Moment of Truth for the S&P 500 - 7 July 2014

- The Evolving Future of the S&P 500: 2014-Q2 1 July 2014

- Means, Motive and Opportunity with the S&P 500 - 26 June 2014

- RIP: Our S&P 500 Echo Filtering Technique - 23 June 2014

- Shifting the Future for the S&P 500 - 9 June 2014

- Time to Enter the Summer Doldrums - 2 June 2014

- Echoes, Aftershocks and the S&P 500 - 12 May 2014

- S&P 500: Nothing Much to See Here - 28 April 2014

- An Uneventful Week for the S&P 500 - 21 April 2014

- The Evolving Future of the S&P 500 - 7 April 2014

- Extending the Alternate Futures - 31 March 2014

- A Better Frame of Reference, Mean Reversion and the S&P 500 - 18 March 2014

- Rewriting the Alternate Futures - 10 March 2014

- The S&P 500 in February 2014 - 3 March 2014

- Calibrating the Futures of the S&P 500 - 18 February 2014

- With and Without the Echo - 10 February 2014

- S&P 500: Right About on Target - 20 January 2014

- The S&P 500 Behaving as Expected in the First Week of 2014 - 13 January 2014

- The S&P 500 As We Saw It in Real Time in 2013 - 7 January 2014

- A Last Look at the S&P 500's Future in 2013 and a First Look to 2014 - 16 December 2013

- The S&P 500's Echo-Adjusted Reverberations - 9 December 2013

- The S&P 500 After the Echo Arrives - 3 December 2013

- Filtering the S&P 500's Echoes of the Past, Part 2 - 20 November 2013

- Filtering the S&P 500's Echoes of the Past, Part 1 - 19 November 2013

- The Anniversary of the Great Dividend Raid of 2012 - 18 November 2013

- The S&P 500 Before the Echo Event Begins - 9 November 2013

* Note: To the best of our knowledge, we're the only stock market analysts who have made our work product fully transparent by developing it in public and sharing our observations and results in near-real time on the Internet. And we've been doing it since we announced our original discovery of what really drives stock prices on 6 December 2007.

Welcome back to the cutting edge!

Update 13 October 2014, 8:20 PM EDT: Today's market action is what a shift in focus looks like - where investors suddenly shift their focus from one point of time in the future to another. Or, in terms of our rebaselined chart, from 2015-Q2 to 2015-Q3:

As for why investors shifted their focus to 2015-Q3, well, that's easy. One of the minions at the Federal Reserve indicated that economic weakness would lead the Fed to delay those interest rate hikes, which for the Fed's game of expectations, had been set to occur in the middle of 2015. With evidence of a weakening economy in the present mounting, it wouldn't take much for investors to shift their attention further forward in time as they could reasonably believe the Fed will be forced to delay.

It's a small change, but one with an amplified impact upon stock prices given the nature of how they work.

Remarkably, stock prices are still within our forecast range for 13 October 2014 assuming that investors had been focused on 2015-Q2 in setting today's stock prices - we've gone from one extreme to the other in just a matter of days. Whether this change is just a temporary noise event or actually a sustained shift in focus will become evident over the next several days.

Update 14 October 2014 8:06 AM EDT: From the WSJ - Despite Mixed Risks in U.S., Rate Timing Hasn't Shifted Much. Indeed!

Welcome to the blogosphere's toolchest! Here, unlike other blogs dedicated to analyzing current events, we create easy-to-use, simple tools to do the math related to them so you can get in on the action too! If you would like to learn more about these tools, or if you would like to contribute ideas to develop for this blog, please e-mail us at:

ironman at politicalcalculations

Thanks in advance!

Closing values for previous trading day.

This site is primarily powered by:

CSS Validation

RSS Site Feed

JavaScript

The tools on this site are built using JavaScript. If you would like to learn more, one of the best free resources on the web is available at W3Schools.com.

Other Cool Resources

Blog Roll