Now that it's the day after Thanksgiving, when Americans are collectively digesting the turkeys that graced their family's dining tables, some are turning their attention toward planning the next year's feast. Perhaps, instead of dining on what might be called a farm-raised frankenbird, it might be better to hunt one a real one down in the wild, the way the original pilgrims did.

But that presents a problem, because while turkeys are found in many places throughout the country, they're notoriously difficult to hunt. It takes a lot of stealth to be successful at it, since turkeys in the wild are reported to be surprisingly intelligent.

Or perhaps not so much, if U.S. Patent 7,828,003 is any indication. The patent, which was issued to Tom Montecucco of Spokane, Washington on 9 November 2010, describes what we'll call the "ultimate turkey blind" as follows:

A combination decoy and hunting blind is provided in a portable and lightweight configuration to attract game animals while also concealing a hunter from the game animals. More particularly, a turkey decoy and hunting blind is provided by a portable structure....

... a hunter concealment device is provided having a canopy frame, a panel and an image of a game animal. The canopy frame has a shaft, a central hub, a plurality of ribs each pivotally coupled at a radial inner end to the hub, a sliding ring, and a radial array of stretchers each pivotally coupled at one end with the sliding ring and pivotally coupled at another end with a respective rib. The central hub is carried by the shaft. The sliding ring is mounted for movement along the shaft. Movement of the sliding ring along the shaft towards the central hub is operative to kinematically articulate the canopy frame between a folded orientation and an unfolded orientation. The panel has a front surface, a rear surface, and an outer periphery. The panel is supported by the canopy frame between stowed and deployed configurations. Then image of a game animal is provided on the front surface of the panel.

Sounds impressive, doesn't it? But if you take a moment and read through it closely, you'll realize that what the invention really is, is an umbrella that features a large picture of a turkey on it. And if words aren't enough, the following images from the patent should confirm it for you. The first patent image shows an intrepid turkey hunter demonstrating the portability of the collapsible hunting blind.

Our second patent image shows the invention deployed as the desired prey might see it.

And our third image from the patent shows the hunter concealed behind the collapsible hunting blind, where he awaits the opportunity to obtain next Thanksgiving's centerpiece.

The Collapsible Hunting Blind features peepholes allowing the hunter to see his prey, and we presume also has a feature allowing the hunter to extend his firearm through it as well. We can only imagine what goes through a wild turkey's mind when they encounter this invention in use:

"Hey, is that Big Larry?! Larry, is that you?! Why is Larry carrying a gun?! Nooo!"

We added all the exclamation marks because we suspect that this might actually be dialog from a Mark Trail comic strip someday.

We're not alone in our observations that the invention is rather absurd. Gene Quinn, a U.S. patent attorney also weighs in:

It is a bit difficult to take this invention too seriously for several reasons. First, according to Oregon State University poultry scientist Tom Savage, turkeys are “smart animals with personality and character, and keen awareness of their surroundings.” That being the case, exactly which turkeys are likely to be attracted by a 6 foot turkey plastered onto a giant umbrella laid on its side, as pictured in the main drawing in the patent? Furthermore, Figure 13 (see below) is exactly an umbrella with a turkey decoration, yet the patent describes Figure 13 as a “fully deployed configuration of a blind as as to illustrate turkey decoy image.” Really? A hunting blind? This is an old fashion umbrella.

And yet, officials of the U.S. Patent Office issued a patent for it. But then, they issued a patent for a stick once before too, so we suspect their standards are pretty low....

Other Stuff We Can't Believe Really Exists

- Inventions in Everything: The Ultimate Turkey Blind

- Inventions in Everything: Turning Cans Into Sippy Cups

- Inventions in Everything: Anatomical Lego Figures

- It's Not What You Think....

- Inventions in Everything: Soup Bowl Attraction

- Inventions in Everything: Making Life More Difficult

- Inventions in Everything: The Oreo Separator Machine

- Air Shark!

- Markets in Everything: Stormtrooper Motorcycle Suit

- The Bike That Rides You

- One Inventor's Stick-to-itiveness

- High Five!

- Inventions for Everything

- The Best Mousetrap Ever

- An Invention for the True Wine Connoisseur

- Three of Ten Things You Don't Need on St. Patrick's Day

- The Future Just Got a Lot Cooler Than It Used to Be

- The Worst Piece of Design Ever Done

- The Magic Marker of the Future

- Coming Soon, to a Gym Near You!

Previously on Political Calculations for Thanksgiving Week 2013

Labels: food, technology, thanksgiving

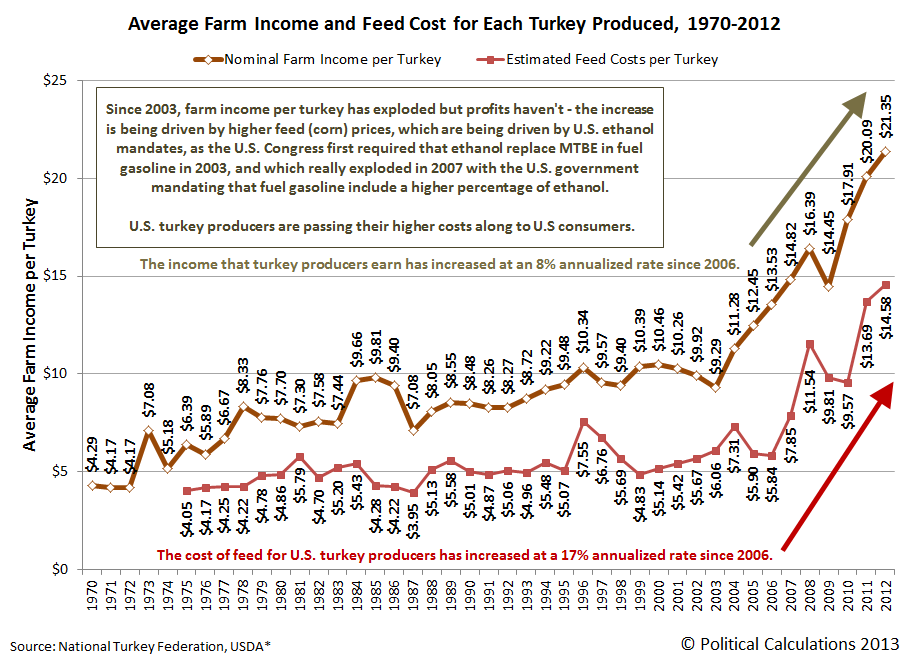

After showing the growing size of turkeys raised in the U.S. over the last 32 years, we wondered how much money U.S. turkey producers were making per bird.

After all, if they're producing more meat on each bird and are therefore satisfying consumer demand for turkey meat while raising fewer birds, the increase in productivity of U.S. turkey farmers should be putting some serious cash in their pockets.

But that doesn't consider their costs of doing business. Bigger birds likely eat a lot more, which means that they cost more to raise. Our chart below shows the average farm income per turkey from 1970 through 2012, and the average feed cost per turkey for each year from 1975 through 2012:

In this chart, we see that the trends in farm income per turkey and feed costs were rising fairly slowly from 1970 through 2002, but we see their income per turkey began rising rapidly beginning in 2003 and that their feed costs exploded beginning in 2007.

As it happens these are both key years for the federal government's subsidization of U.S. ethanol producers, who produce ethanol from corn, which is also the primary feed grain for farm-raised turkeys.

In 2003, the U.S. federal government acted to make ethanol the sole oxidation agent additive for fuel gasoline in the U.S. And in 2007, the federal government mandated that an increasing percentage of all fuel gasoline sold in the U.S. consist of corn-produced ethanol.

That affected the price of corn, the available supply of which was first drawn down after the government's 2003 action, which then became stuck in near shortage conditions once the 2007 mandate went into effect. The refusal the U.S. government to waive its ethanol mandate in the years since resulted in skyrocketing corn prices, which U.S. turkey farmers have been forced to pass along to their consumers in order to stay in business.

And that's why turkeys for Thanksgiving cost so much more today than what basic inflation would suggest they would, as they're getting back to the levels they cost during the stagnant '70s.

And the Number One factor driving them back to that level is the U.S. government's policies for ethanol.

Previously on Political Calculations

Labels: business, food, thanksgiving

The title of our post today is a twist on the series of posts that Marginal Revolution's Tyler Cowen has featuring the pro-and-con arguments that the U.S. economy is experiencing stagnation today.

Only here, we're going to consider the evidence provided right at the center of your Thanksgiving holiday: the not-so-humble American farm-raised turkey! Our chart below shows the trends that have shaped the farm-raised turkey from 1970 through 2012:

In the chart, we see that there has indeed been a Great Stagnation for turkeys raised in the U.S., which ran throughout the decade of the 1970s, at least as measured by their average live weight.

But since 1980, the average live weight of U.S. farm-raised turkeys has increased from 18.7 pounds to 29.8 pounds in 2012. Going by the trend, we project that the average live weight of turkeys produced in 2013 will be 30 pounds.

In terms of weight, today's turkeys are now 60% heavier than the average live weight of 18.7 pounds that was recorded by their forebearers in the stagnant '70s!

What that means, of course, is that today's turkey farmers are continuing to innovate ways of breeding larger birds, which allows them to bring more meat to market while raising fewer birds.

Now, we know what you're thinking - in breeding ever-bigger birds, today's turkey farmers have got to be pulling down some serious cha-ching! We'll look at how much money they're making per turkey in our next post (when this link goes live!)

Previously on Political Calculations

Labels: food, thanksgiving

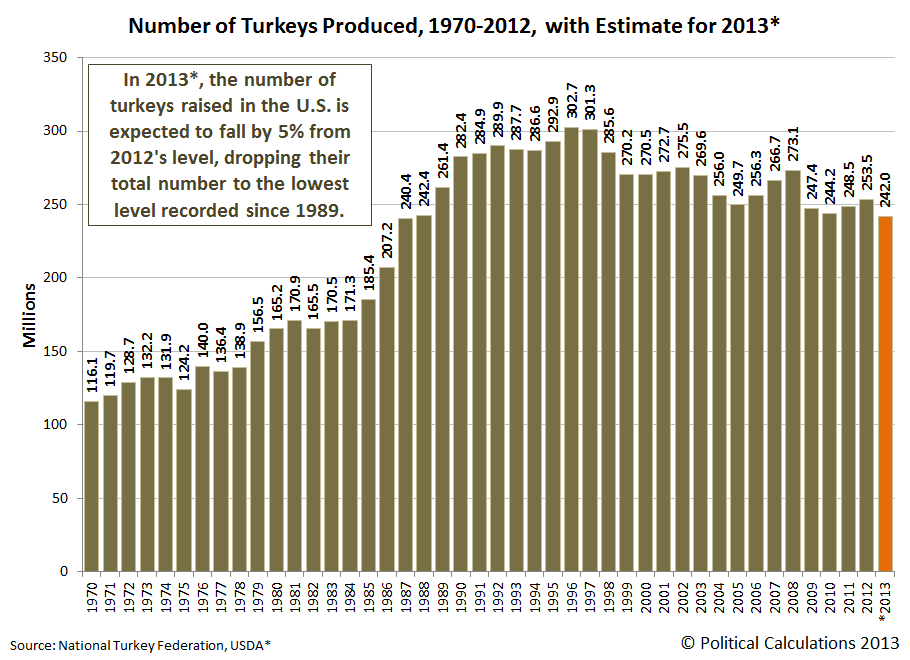

How much do 242 million turkeys weigh?

That's the question we're taking on today, as we gear up to celebrate the Thanksgiving holiday this week! Our chart below shows the total combined live weight of all turkeys raised in the United States from 1970 through 2012, with the best estimate we could determine for 2013 with the information we have:

In 2012, the 253.5 million turkeys raised in the U.S. collectively weighed 7.55 billion pounds [3.42 billion kg]. For 2013, with an estimated 11.5 million fewer turkeys raised during the year, we project that their combined weight will be about 7.26 billion pounds [3.29 billion kg].

At just over a 4% decline, that's a bit less than the 5% by which the population of turkeys has been estimated to decrease in 2013, as we expect that the average live weight of turkeys raised in the U.S. has increased since 2012.

But that doesn't give a good sense of how much turkey meat might reach the market. For that, we'll consider the Ready-To-Cook (RTC) weight of all the turkeys raised in the U.S. in our next chart:

Here, we find that the RTC weight of turkeys produced in the U.S. for 2013 is projected to be about 5.75 billion pounds [2.61 billion kg], down from the 5.97 billion pounds [2.71 billion kg] that was ready-to-cook in 2012.

Combined with the number of turkeys produced in the U.S., the data for the total live weight of all these turkeys is enough for us to determine the trends for the size of the average turkey raised in the U.S. since 1970. And that will be our next stop as we consider just how turkeys themselves have changed in 44 years of Thanksgivings (when that link will connect through!)

Data Sources

National Turkey Federation. Sourcebook. [PDF Document]. October 2013.

The Poultry Site. USDA Livestock, Dairy and Poultry Outlook - November 2013. [Online Article]. 15 November 2013.

U.S. Department of Agriculture. Turkeys Raised. [PDF Document]. 30 September 2013.

Labels: food, thanksgiving

It's Thanksgiving week once again, and here at Political Calculations, that means putting aside all our regular analysis to instead focus on the centerpiece of the meal that will grace more dining tables on one day than any other: turkey!

We're going to kick off this week's festivities by looking at how many turkeys have been raised in each year from 1970 through 2013, which we've visualized in our first chart:

In 2012, there were 253.5 million turkeys raised on farms across the United States. In 2013, the USDA estimates that number has fallen by about 5% to 242 million.

U.S. turkey production peaked in 1996 at 302.7 million. If the USDA's estimate of 11.5 million fewer turkeys produced in 2013 than in 2012 holds, that would be the lowest number of turkeys produced since 1988.

So what does 242 million turkeys mean in terms of the pounds of turkey headed for market? Stay tuned, as we'll weigh them all next! (Note: that link won't work until we get them on the scale sometime tomorrow!)

Data Sources

National Turkey Federation. Sourcebook. [PDF Document]. October 2013.

U.S. Department of Agriculture. Turkeys Raised. [PDF Document]. 30 September 2013.

Labels: food, thanksgiving

It's the week before Thanksgiving, which means its time for consumers to gear up for the Christmas holiday shopping season that retailers began gearing up for back in June. But if the person you're shopping for works in the financial industry, or perhaps is simply some sort of strange economics wonk, that can be especially tough. After all, what can you possibly buy that would be genuinely fun for someone whose idea of fun revolves around banking or monetary policy?

We here at Political Calculations are happy to help you solve this problem! After watching Despicable Me 2 in the theaters earlier this year, it dawned on us that many of the animated characters in the movie are actually modeled after real life people. Specifically, the officials of the U.S. Federal Reserve.

For example, here's a side-by-side comparison between Minnesota Fed president Narayana Kocherlakota and the minion Dave:

|  |

Next, here's is Philly Fed chief Charles Plosser and the minion Stewart:

|  |

It gets even more uncanny. Next, we have Chicago Fed president Charles Evans and his doppleganger, the minion Tim:

|  |

Finally, what Federal Reserve action figure set would be completed without the big guy himself, Fed Chairman Ben Bernanke (a.k.a. Gru):

|  |

We're pretty sure that a Janet Yellen action figure is in the works for either the Minions or Despicable Me 3 movie projects now in development.

And as far as the connection between the minions of the Despicable Me movies and the officials of the Federal Reserve, well, here it is....

Labels: none really

The expectations of investors for S&P 500 earnings continued to fall in the three months since our last snapshot of them.

Since peaking ahead of Summer 2013 at $108.18, the collective amount of earnings per share now expected to be earned by S&P 500 companies through the end of 2013 has fallen to $97.82 per share.

This is the lowest level that investors have projected for trailing twelve month earnings per share for 2013 since S&P's forecast for 2013 was first projected in January 2012.

Data Source

Silverblatt, Howard. S&P Indices Market Attribute Series. S&P 500 Monthly Performance Data. S&P 500 Earnings and Estimate Report. [Excel Spreadsheet]. Last Updated 14 November 2013. Accessed 20 November 2013.

In Part 1, we explored the challenges associated with filtering out the noise of the past in calculating the change in growth rates of stock prices. We left off by identifying a period of time in the stock market, some 10 months ago, that might work as a good base reference point from which we can quantify the amount of echo effect present in our regular year-over-year growth rate data.

Let's get straight to the results. Our first chart shows the change in the annualized growth rate for stock prices using that 10-month base reference period against our usual change in the year-over-year dividend growth rates:

That red bracket gives an indication of the amount of the echo effect that is currently present in our regular model of stock prices. Speaking of which, the chart below shows what that looks like going into today:

Now, the reason we're going through this exercise is to work out how much do we need to take the echo effect into account in using our dividend futures-based model to project what today's stock prices in the absence of current-day noise. Is our model self-correcting, where we can simply use the year-over-year growth rate data, as we would seem to be able to do so far in using last year's stock prices along with the expectations for dividends to be paid in 2014-Q1? Or do we need to make some adjustments to account for the effect of long past noise in the market?

We don't know the answer yet. We're excited to find out as this all plays out!

Finally, before any of our readers at Seeking Alpha get all upset at whatever again, keep in mind that we're the only market analysts who do theoretical development and analysis in public view. We don't work with a safety net and there's a real potential that our previous thinking may turn out to be wrong.

For all our other readers, that we very rarely ever are is probably lost upon that group.

What exactly was happening one year ago and just six months ago in the stock market?

We're asking that question today is because of the two charts we featured yesterday that we're showing side-by-side below, which look very similar to one another except for the very recent trajectory of stock prices:

|  |

In the chart on the left, we're showing the change in the year-over-year growth rate of S&P stock prices with respect to the change in the year-over-year growth rate of expected future dividends per share. In the chart on the right, almost everything is the same as on the left, except for the change in stock prices, where we're instead showing the change in the annualized growth rate of stock prices over the preceding six months.

So why is there such a difference between the apparent trajectory of the change in the year-over-year growth rate of stock prices?

The answer has to do with the base reference point from which those growth rates are calculated. In the chart on the left, that base reference point was one year ago, which in the chart, coincides with the decline in stock prices that occurred as the stock market initially reacted to Barack Obama's re-election, just before the tax avoidance-inspired stock market rally that defined the Great Dividend Raid of 2012.

When calculating the year-over-year growth rate in stock prices, because the growth rate is very sensitive to both the starting and ending points of the period in question, the decline in stock prices a year ago combined with their current trend is showing up in the form of an elevated growth rate. We see that in the relatively elevated level that daily stock prices have taken, which are now above the level that the expectations associated with the level of dividends for 2014-Q1 would place them.

Meanwhile, six months ago, the stock market suddenly spiked upward on 14 May 2013, as stock prices were racing to catch up to the then recent shift in the forward-looking focus of investors, who were shifting away from focusing on the dividends they were expecting to earn in 2013-Q2 to instead focus on the more distant future of 2014-Q1.

With stock prices then suddenly elevated, that reduces the annualized growth rate between then and now, which shows up in the sudden decline in the change in the growth rate for stock prices in our chart on the right!

To help better understand the dynamics of what was going on six months ago, it might help to look at the trajectory that stock prices as represented by the value of the S&P 500 have taken with respect to our dividend future-based mathematical model of stock prices:

In the chart above, we observe that investors shifted their forward-looking focus away from 2013-Q2 toward 2014-Q1 in mid-April 2013.

Prior to that time, stock prices were largely moving in lockstep with the expectations associated with the future for 2013-Q2. Because stock prices are driven by expectations for the amount of dividends that will be paid in the future, the shift to the significantly higher level of dividends that were expected to be paid in the first quarter of 2014 sparked an investor-focus transition rally for stock prices at that time.

But then, something changed. What changed was the expectation for the level of dividends that would be paid in 2014-Q1, which dropped from $9.370 per share on 10 May 2013 to $9.113 per share on 13 May 2013, at least according to the CBOE's DVMR dividend futures.

Investors were slow to react to that fundamental shift in future expectations for dividends, and the sudden spike upward on 14 May 2013 was really a short-lived noise event as stock prices overshot the level that would be supported by 2014-Q1's expected dividends.

Consequently, the focus transition rally stalled out and stock prices drifted lower to converge with the newly adjusted future expectations for dividends in 2014-Q1. They finally moved below the level that our dividend futures model would set them, and were beginning to rally once again in mid-June 2013, which was interrupted by the market's reaction to Federal Reserve Chairman Ben Bernanke's comments on 19 June 2013, after which the trajectory of stock prices is more characterized by noise than fundamentals, at least up until the end of the debt ceiling crisis in mid-October 2013.

Getting back to the subject at hand, that dynamic from six-months ago makes this period a poor base reference from which to measure the growth rate of stock prices. To minimize the echo effect of past noise or fundamental shifts in focus in our math, we really want to choose a base reference period that is removed from these kinds of disruptive events, where stock prices were changing at a steady pace.

Looking at our third chart showing the trajectory of stock prices with respect to that suggested by our mathematical model, the obvious candidate that best fits these requirements is the period from approximately 17 January 2013 through 19 February 2013. Using this period as our base reference would allow us to work around the term of the Great Dividend Raid rally, which ended on 20 December 2012.

And that's where we'll pick things up next....

Labels: chaos, dividends, SP 500

One year ago, last Friday, the Great Dividend Raid of 2012 began.

The raid was the response of influential investors to President Obama's reelection, which ensured that higher tax rates on both income and investments would take effect on 1 January 2013, an event that is perhaps better known as the Fiscal Cliff. Most of the those tax hikes were tied to the expiration of President George W. Bush's 2001 and 2003 tax cuts and President Obama had made clear to U.S. CEOs on the afternoon of 14 November 2012 that he desired to end.

That set up the situation where the influential investors who own and manage the U.S.' public companies would have to act to beat the clock to avoid facing higher taxes. So they raided the funds that they were setting aside to pay dividends in the first three quarters of 2013 to instead pay out before the end of 2012, where they could avoid being taxed at the higher tax rates that would apply after 31 December 2012.

All that began on 15 November 2012. Prior to that day, stock prices had fallen sharply in response to President Obama's reelection. But that reversed quickly when U.S. companies began announcing they would be paying increased dividends before the end of the year, which sparked a major rally for stock prices.

Believe it or not, we're already seeing the echo of the events that lead up to the Great Dividend Raid and its corresponding stock market rally. Our favorite chart, in which we track the acceleration of stock prices, or rather, the change in the year over year growth rate of stock prices, has been reading much higher values than it should since 6 November 2013:

In the chart above, we see that as it would appear that daily stock prices are hovering around the level that the change in the expected year-over-year growth rate of dividends per share in 2014-Q1, which is the point in the future where we've identified that investors have largely been focused since mid-October 2013.

That's significant because it gets at something we were trying to describe last week, where we hypothesized that an echo effect might look like a fundamental shift in the forward-looking focus of investors.

Here, it looks exactly like investors are tightly focused on 2014-Q1, but that's only because stock prices had fallen so much in the week following President Obama's re-election in 2012.

Now, that pattern exists because we use the stock price and dividend data from a year earlier as the base from which we calculate the growth rates of both. To filter out that effect, we can shift that base reference point in our calculations to a different point in the past.

So we've done that. In the chart below, instead of using the year-over-year change in stock prices, we'll instead calculate the change in the annualized growth rates over the preceding six months:

Here, the major patterns and trends are basically the same for each of the major noise events we've tracked in our regular year-over-year chart, except perhaps a bit magnified. But then, during the past week, we see a major divergence develop, where instead of hovering around the level for dividends expected in 2014-Q1, we see that the change in the growth rate of stock prices is falling rather dramatically with respect to our six-month ago base of reference.

The difference between the two would represent the potential magnitude of the echo effect.

Before you panic, consider this - how much of that might be the echo of something that happened in the stock market six months ago, and how much might be due to the echo of something the events of one year ago? Perhaps we should be setting our reference point at a different point of time....

Labels: chaos, SP 500, stock market

Not long ago, we talked about the innovations in aluminum can technology being developed by craft brewers to improve the drinking experience of their consumers. Today, we're going to consider how winemakers are looking at cans as the potential preferred containment device for their products!

Specifically, we're going to consider the factors that Oregon's Union Wine Company are considering in bringing wine to consumers in aluminum cans. David Graver of Cool Hunting describes his recent experience with the winemaker's pinot noir and pinot gris canned wines:

What began as a promotional product for Portland's Feast 2013 food and wine festival, Union Wine Company's wine in 12oz cans will actually be making its way to shelves. Its initial limited edition release drew rave reviews, for both its pretenseless "pinkies down" philosophy and the quality of the wine within. The idea of wine in a can was inspired by Union's company mission to make wine more accessible, and this very well may do the trick.

We found the product to be novel and the experience enjoyable, but we were surprised by how great the wine was—causing us to rethink previous notions about bottling. The cans carry both Underwood Pinot Noir and Pinot Gris, with grapes from across Oregon. Reasonably priced and with the craftsman spirit of the region, the cans are just an added bonus. And if drinking wine from a can isn't your thing, pour it into a glass and let it breathe because the product is deeper than the packaging.

Core77's Rachel Swaby explains how canned wine came to be:

Ryan Harms, the owner of Union Wine Co., is a firm believer in the saying "it takes a lot of good beer to make good wine." He likes the way a beer can feels in your hand and its portability, but he didn't seriously think about canning wine until that rebranding meeting in June. He and his team talked about wanting their products to be accessible, both in the approachability of the varietals' flavors and the ease with which one could grab a drink. They wanted to see their wines included on a backcountry skiing trip or packed for an exploration of Mount Hood. All of a sudden, the can seemed like a viable wine-delivery option.

But the company also had a difficult set of parameters to work within. Wine production is regulated, and wine can only be sold in certain size containers. At the same time, Harms felt very strongly about keeping it in a can that looked and felt like a beer can. That size, he thought, just felt so much more satisfying in the hand than the skinny cans in the energy drink world, which he didn't have any emotional connection to. But the average 12-ounce beer can holds just under an amount that can be put on store shelves. If Union wants a beer can, those cans will actually have to hold 375 milliliters, or 12.68 ounces.

Right away, we see that government regulation provides a serious obstacle to economic development. Instead of being able to simply use the same 12oz cans used by soda and beer producers, winemakers are restricted from that option, which makes it more difficult for them to economically bring such a product to the market - and the product they ultimately do bring to the market will come with a higher cost to consumers as a result. This is a fantastic example of how regulations impose deadweight losses upon the economy, both in preventing a product from being able to easily come onto the market and needlessly making it more costly than it might otherwise be.

And that's on top of the actual considerations for the wine itself - not all wines lend themselves to being served in cans:

Harms is half businessman and half winemaker, and he didn't want the business idea to come at the expense of his craft. But he was also really tied to the everyday can. So he tailored the wine to suit the can instead of the other way around, discounting any varietal that wouldn't do well there. "The types of wine in cans don't need to be decanted or to age for five years to be accessible," says Harms. "That would be a real disservice to put products like that in a can." Wines that do better: "wines from the fresh and fruit-driven world, whether that's white or red."

Because it doesn't have a lot of tannins, the company's Oregon pinot noir fit the bill. For whites, it went with a pinot gris, which has a higher acid level, and is also fruit-driven. For these blends—and the newer-to-wine clientele Union Wine is trying to reach—the can is a fine delivery system, says Harms.

While much of the story revolves around the Union Wine Company's efforts to solve the technical problems of putting wine into aluminum cans, the best part of the story is that it would seem to meet a previously unexplored demand from consumers to have wine available in cans. We'll give the final word to the voice of the customer:

While they figure out the last few details, Harms is taking solace in a comment he overheard at the Feast festival. When a woman in her 70s was offered wine in a can or in a bottle, she chose the can: "I have to have this," she said. "It would be perfect for the golf course."

Image credit: Cool Hunting (Graham Hiemstra)

Labels: economics, food, technology

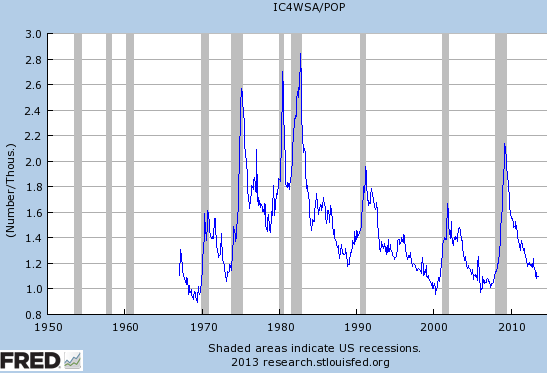

Several weeks ago, something was very wrong with the Department of Labor's reporting of new jobless claims, as it seemed the number of layoffs in the U.S. were consistent with a booming economy. Here is Scott Sumner's take on the data:

Six weeks ago I did a post on the puzzling fall in unemployment claims:

The new claims for unemployment this week was a shockingly low 320,000, bringing the 4 week average down to 332,000

335,000, which is the lowest since October 2007. This graph shows the ratio of the 4 weeks average to US population (times 1000 to make it easier to read.)

The most recent week on the graph is at about 1.1, but today’s figures are at 1.049

1.058, if they were added. This means the ratio of new claims to pop is roughly back to the boom levels of 1999-2000 and 2006-07. And yet the other indicators (total jobs, unemployment rate, etc), remain deeply depressed.I’m not going to redraw the graph, but with today’s numbers (308,000 on the 4 week average) we have fallen below the 0.1% level, meaning that fewer than 1/1000ths of Americans now file for unemployment comp each week. That’s not just boom conditions, it’s peak of boom conditions. The only other times this occurred since 1969 (when unemployment was 3.5%) were just a few weeks at the peak of the 2000 tech boom and a few weeks at the peak of the 2006 housing boom. In other words, the puzzle is now even greater than 6 weeks ago, as the unemployment rate is still at recession levels (7.3%.) Something very weird is going on in the labor markets.

I don’t have any good ideas. Perhaps employers are reluctant to add workers for some reason (Obamacare?) and instead work them overtime more. Then when demand falls instead of laying off workers, they cut overtime. But I don’t recall the average workweek numbers being all that unusual.

The solution to the mystery of the missing layoffs turned out to be a lot more mundane than an economy suddenly and unexpectedly operating at peak-of-boom performance or the pernicious influence of Obamacare. It turns out that the State of California's Employment Development Department, a government agency with a history of incompetence, was once again failing to process hundreds of thousands of new jobless claims in a timely manner, just as it did a year earlier. The difference this time is that government agency's management, who have never been disciplined for their incompetence, blamed their latest claims processing problems on the implementation of new software.

The bottom line is that California's failure to process new applications for unemployment insurance benefits for newly laid off workers in the state sharply skewed the national data downward. And then, because the state had to play catch up after it "belatedly" discovered its problems, those numbers were inflated in the weeks following the state agency's now annual display of ineptitude.

So, to cut through the noise, we treated all of the data from 7 September 2013 through 19 October 2013 as if it were outliers in the national data. The chart below shows the current trend for new jobless claims as best as we determine it:

Overall, we see the layoff situation in the United States as being flat-to-mildly improving since the current trend was established on 23 February 2013, as the number of new layoffs nationally is falling at an average rate between 300 and 500 per week.

We're just happy to say the mystery of new jobless claims is solved!

In 2010, the U.S. Department of Health and Human Services was set up with a slush fund of one billion dollars to support the implementation of Obamacare. If we go by the department's summary of its Fiscal Year 2014 budget proposal, it would appear to have already burned through $811 million through 30 September 2013, the end of the federal government's 2013 fiscal year:

That would leave the department with just $189 million left to spend. It was planning to spend $163 million in the federal government's Fiscal Year 2014, which began on 1 October 2013.

Instead, the problems that have plagued both the department's Healthcare.gov web site and the back end systems that support its operation are forcing the agency to spend this money on fixing its problems.

Keeping in mind that HHS was burning through money at an average rate of $871,233 per day during the federal government's 2013 fiscal year, it is very likely that it is now spending much more than that amount per day as the Obama administration is desperate to keep President Obama's signature achievement from becoming an unmitigated failure.

Something has to give, because they cannot both repair Obamacare's IT systems and web site and spend what they were planning to spend to do other things in FY2014. HHS is running out of money and cannot do both.

Oh, by the way, we described how we could have eliminated HHS' technical problems within a very short period of time for just $47 million back on 22 October 2013. And as far as we're concerned, the hardest part of implementing our solution is already done. And yet, the Obama administration would appear to be more concerned with funneling money to its crony corporate partners than it does in actually making it possible for regular Americans to shop for and buy health insurance as they might choose.

Perhaps a good question for a mainstream media reporter to ask is why does the Obama administration insist on doing those things? And a really good question for a skeptical U.S. Congress member to ask is why they should throw even more money to repair the Obamacare web site when our solution is already proving to be a much more viable and a much more affordable option?

Data Sources

U.S. Department of Health and Human Services. Fiscal Year 2012 Budget in Brief. Advancing the Health, Safety, and Well-Being of Our People. [PDF Document]. 2011.

U.S. Department of Health and Human Services. Fiscal Year 2013 Budget in Brief. Strengthening Health and Opportunity for All Americans. [PDF Document]. 2012.

U.S. Department of Health and Human Services. Fiscal Year 2014 Budget in Brief. Strengthening Health and Opportunity for All Americans. [PDF Document]. 2013.

Labels: business

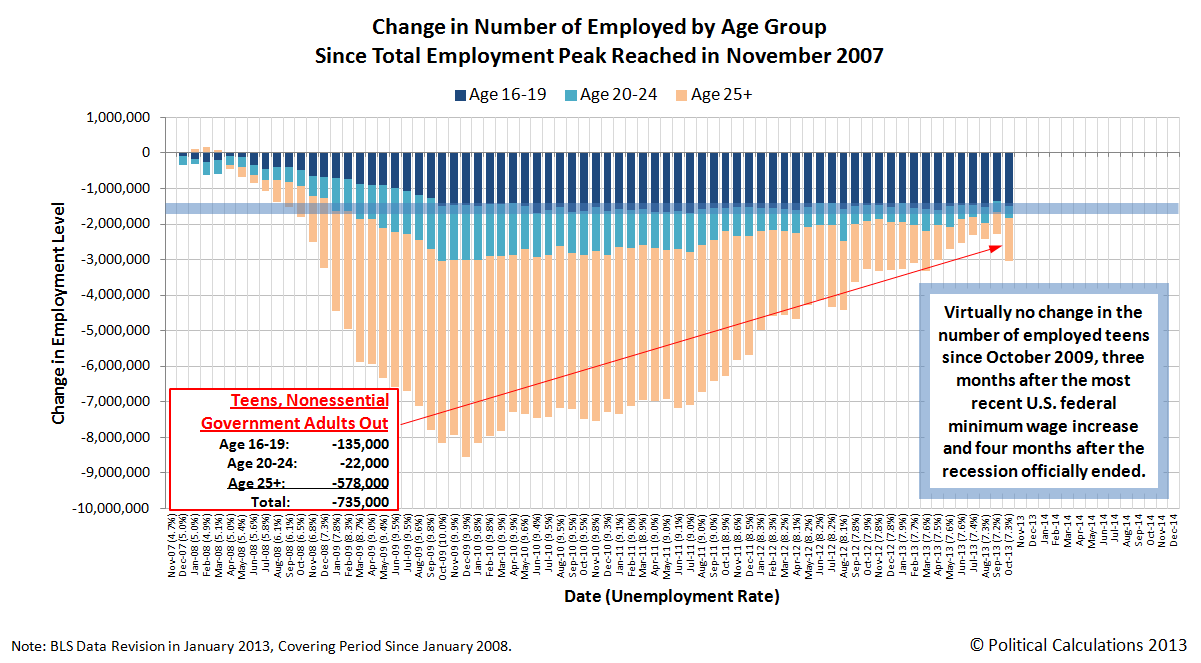

Going by age demographics, the October 2013 Employment Situation Report released last Friday revealed the following numbers.

- 578,000 fewer adults (Age 25 and above) were counted as having jobs in the household survey portion of the report.

- 22,000 fewer young adults (Age 20-24) were counted as being employed in October 2013.

- 135,000 fewer teens (Age 16-19) were working in October 2013.

The big story, of course, was the partial federal government shut down that saw 815,932 government workers be furloughed at the beginning of October 2013. Here though, that number was quickly cut nearly in half as the Defense department recalled most of the 400,000 civilian employees it furloughed on 4 October 2013 back to work, as they were employed in essential functions.

Since the household survey is taken during the week that includes the 12th day of the month, the recalled defense workers were counted as having jobs at the time the survey was taken, but as many as 415,932 other federal government employees who were considered to be genuinely nonessential remained furloughed, adding to the measured decline in the number of employed Americans for the month.

Given what we know of the federal government's civilian employees, almost all are Age 25 or older, which explains why such a large reduction was seen in that age group's employment figures, while there was virtually no impact upon the employment situation for teens or for young adults stemming from the partial government shut down.

Overall, there were 4,443,000 U.S. teens, 13,654,000 young adults and 125,471,000 adults counted as being employed during October 2013, for a total of 143,568,000, which was 735,000 below the previous months total of 144,303,000 working Americans.

Don't feel bad about the employment situation of the federal government's nonessential employees. All are receiving back pay for not working during the furlough. We suppose that's one way of saying that the U.S. Congress did not recognize any difference in their work output during that time.

Meanwhile, those federal government employees who filed for and collected unemployment benefits from their states during the furlough are being required to pay the government back, as the extra $300 to $500 payments that many furloughed nonessential federal government workers received while on unemployment is considered to be too excessively generous on top of what for them amounted to be a fully paid two-and-a-half-week vacation. That's on top of their regular accrued vacation paid-time off benefits.

No wonder U.S. federal government employees are more likely to die than leave their jobs for the private sector!

Labels: jobs

Nothing exciting happened from our perspective for the S&P 500 during the week ending 8 November 2013, as stock prices behaved almost exactly as we suggested they would a week ago, as our chart illustrates:

To save readers from excessive squinting, here are the notes that appear in the margin of the chart:

As Expected: Stock prices largely behaved as expected during the week ending Friday, 8 November 2013. In the relative absence of noise, the change of the growth rate of stock prices began bouncing about the level that is consistent with the change in the growth rate of dividends per share expected for 2014-Q1, where investors have maintained their forward-looking focus.

Wild Cards: Noise events. A shift in investor focus to 2013-Q4, 2014-Q2 would trigger a sharp fall in stock prices.

Overall, it was a boring week. But that might be about to change in the near future, for reasons we'll explore in the analyst notes for this week.

Analyst Notes

We're coming up on the one-year anniversary of the beginning of the Great Dividend Raid portion of the 2012-2013 Fiscal Cliff rally, which launched a major fundamental-driven upward movement in stock prices back on 15 November 2012 that lasted through 18 December 2012 (the second phase of the Fiscal Cliff rally began in January 2013). That's important today because we use the year-over-year growth rate of stock prices in our calculations.

Because stock prices sharply deviated from their previous trajectory as a direct response to that event, we expect that we'll see an echo of the event in the form of an apparent major deviation in our calculated change in the year-over-year growth rates. Since stock prices then rose then in response to that event, unless a similar noise event erupts today to maintain the relative year-over-year margin in stock prices, that echo would show up in our chart above like a large negative noise event.

Similarly, if stock prices had crashed a year ago, then subsequently recovered, we might see the echo of that crash show up in the form of a positive noise event for stock prices.

This might all be well and good, since the echo effect would eventually end and allow to get back to business as usual, just like in a real noise event, but that could create a problem in our doing this kind of analysis while it is ongoing because the deviation in the change in growth of stock prices would not actually be the result of present-day noise. It would instead seem like noise, without actually being noise.

This is something that we've always thought might be a possibility given our analytical methods, and this will provide an opportunity to test out the echo-filtering techniques we've been thinking about developing for some time.

But even without those techniques, we wonder if the unfiltered trajectory of the change in the year-over-year growth rate of stock prices might not drop down to the level that corresponds the change in the expected year-over-year growth rate of dividends per share for 2013-Q4.

Normally, we would interpret that kind of dramatic swing as a change where investors have refocused their forward-looking attention and expectations in setting today's stock prices, but we wonder if the echo effect with the unfiltered data would make that seem to be the case, even though investors would really be focused on a different quarter in the future. The echo would then appear as a shift in forward-looking expectations, and although it would be a phony shift, it would mean that our methods of projecting stock prices can still work even under that condition!

We're excited - we're going to find out how this works really soon!

On 22 October 2013, we described how the dysfunctional Healthcare.gov web site could be fixed within a very short period of time.

It turns out that three of our code-developer colleagues have put the shopping portion of our solution into effect:

Meet the Health Sherpa, the website HealthCare.gov probably should have been. George Kalogeropoulos, Ning Liang and Michael Wasser saw the troubled launch and decided they could do a better health care enrolment website better than the government and, by golly, they succeeded. The Health Sherpa makes it ridiculously easy for anyone to compare health care plans covered under Obamacare in 34 states. (They left out the 16 states with existing marketplace sites, though it seems support for those states is coming soon.) The result is a simple, beautiful, remarkably responsive website that anyone could use.

Here's what their site looks like today:

Here's the part of our plan that they executed:

Now, notice that we haven't specified just how the Healthcare.gov web site will itself be fixed. Well, all those tech surge troops can redesign the entire site after first throwing out about 5 million lines of useless code, to instead simply present a place where people can click their state and drill down to their county or city to find links to the sites of the government-approved health insurance providers serving their area, and nothing else.

No accounts to set up, no passwords to memorize, no multiple screens of denied access - none of that nonsense.

And they wouldn't even have to change the current launch screen for the Healthcare.gov site!

See! Transforming Healthcare.gov into a web site that actually works just isn't that hard - if the Obama administration is willing to be transparent how much their health insurance will cost and otherwise remove the federal government from the picture altogether.

Starting with your zip code, that's exactly what they do.

Since the information that consumers get about the plans (premiums, deductibles, what doctors are in-network, etc.) comes directly from the insurers themselves, health insurance shoppers are able to trust it far more than the government-run marketplaces. And they would be assured that their private, personal information would not be placed at risk, which it most certainly would be placed at extreme risk if it were entered in the Healthcare.gov web site.

Now, here's the really cool part - the people who have discovered The Health Sherpa would appear to be raving about it:

The remaining parts of our solution for fixing the Healthcare.gov web site fully takes the federal government out of the picture, since we don't need it to handle either income verification or the calculation of what a health insurance buyer's estimated tax credit subsidy might be. The only thing standing in the way of a functional web site is the incompetent Obama administration, which seems more interested in transferring even more taxpayer dollars to their crony corporate supporters and trying to distract attention away from its problems than it does in making a web site that's supposed to make it easy to shop for health insurance actually work.

The bottom line is that we have been proven right. Again. Our solution succeeds because of its transparent approach and because it takes the federal government's unnecessary bureaucracy and political corruption out of the picture.

Perhaps a good question for a mainstream media reporter to ask is why isn't the Obama administration willing to do those things? And a really good question for a skeptical U.S. Congress member to ask is why they should throw even more money to repair the Obamacare web site when our solution is already proving to be a much more viable and a much more affordable option?

Labels: health care, technology

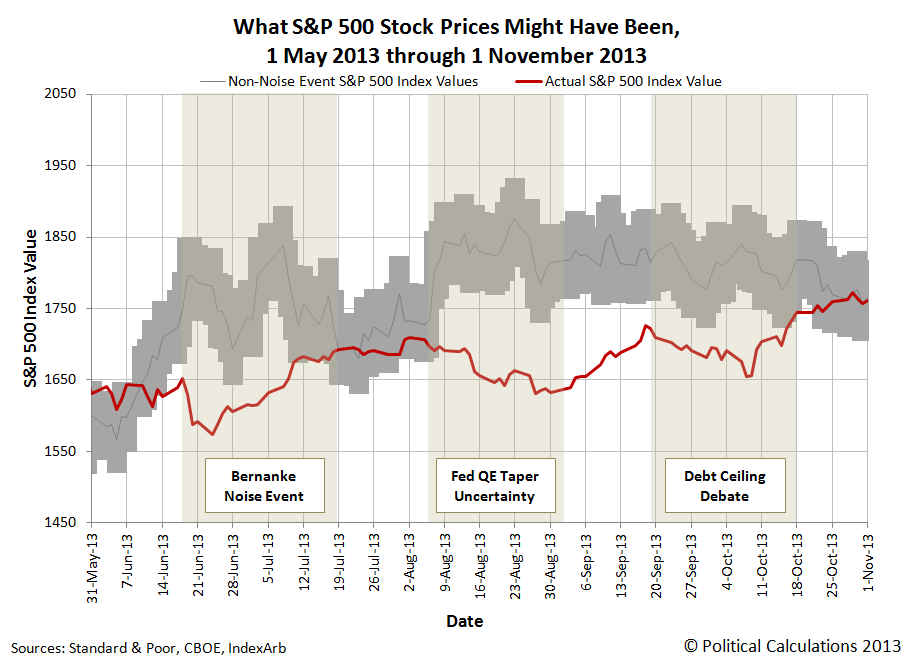

How would stock prices have behaved during the summer and fall of 2013 if the stock market didn't have such large noise events to contend with during that period of time?

Normally, we concern ourselves with the alternate futures where stock prices are concerned, but today, we're looking in the rear-view mirror because that's the natural question that arises from a casual throwaway line in our 4 November 2013 review of the previous week's S&P 500's performance.

So to answer that question, we thought we might visualize just what that alternative past would have looked like! Our results are presented in the chart below:

Here, we've taken our dividend futures data for 2014-Q1, which would appear to be where investors have collectively focused their forward-looking attention since early May 2013, and used it with our math linking dividends and stock prices to see what stock prices would have been if investors had not been distracted by those huge noise events.

Now, that doesn't mean that there wouldn't have been any noise at all in the stock market. With so many trading transactions and minor news events each day, stock prices would still bounce around their target level quite a bit. In the chart above, we've shown that "typical" level of noise as being within a plus-or-minus 3% range of our 2014-Q1 dividend futures target level for the S&P 500's index value.

The really odd thing is that stock prices have largely gotten to where they would otherwise have been despite the negative effect of all these big noise events - and that's what we mean when we say that all noise events end - it's only ever a question of when.

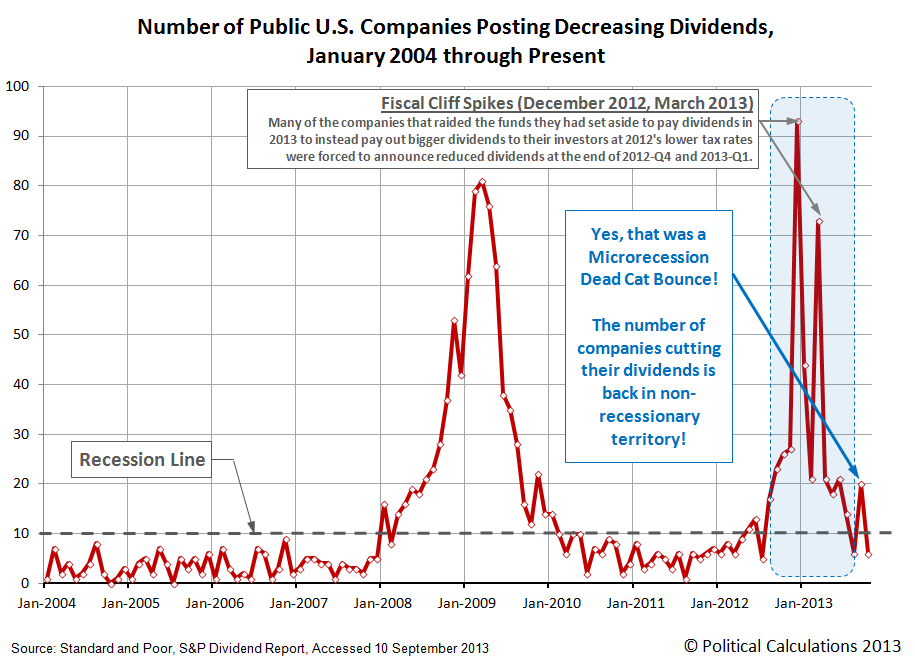

Last month, we speculated that the increase in U.S. companies announcing dividend cuts from six in August 2013 to 20 in September 2013 might must be a microrecession dead cat bounce. The numbers for October 2013 indicate that speculation was correct, as the number of public U.S. companies announcing cuts to their dividends fell back to six:

This low level is a positive indicator for the U.S. economy, and is worth noting that it occurred as anywhere from 17-18.5% of the U.S. federal government, depending upon how you measure it, was shut down during half that month.

What that result confirms is that the partial government shut down was largely a non-event for the U.S. economy as a whole. When when you consider that S&P estimated that the potential reduction in the nation's GDP might be as high as $24 billion, a figure that would seem to greatly distress lesser economists, it really only amounted to about 0.14% of the U.S.' estimated $16,764.5 billion GDP for the recently completed third quarter of 2013.

That "loss" is indistinguishable from noise. And since the federal government responded to the end of the partial government shut down by resuming all its planned spending, including giving nonessential federal employees full back pay for the time they were furloughed from work, while letting many keep the extra income they collected through unemployment benefits, there really wasn't any meaningful loss to the economy as a whole.

Labels: dividends, gdp, SP 500

What is the proper role of debt in public policy?

Most people would agree that when a government borrows money, it should be used to fund projects today that will provide positive benefits to the community for years to come. That mainly means things like investing in physical infrastructure to support not just projects that have high costs to create, such as roads, bridges, water treatment facilities, airports or schools, but also that will also last for decades while providing a positive return on investment through increased economic activity.

Under no circumstances however should governments borrow large amounts of money for the sake of sustaining their day-to-day operations that they cannot pay off with their direct tax collections within the course of a single year. These are not just expenses like the wages, salaries, and benefits of government employees and the office supplies they consume, but also for things that have relatively short life spans, which means that they will need to be replaced within in much less than ten years time. Things like library books, computer software, mobile phones, police cars, trash bins, et cetera.

The reason why it is such a bad thing to begin using large amounts of debt to finance short-term operational expenses is because of the mismatch it creates between the life span of the expense and the term of the debt. It makes absolutely no sense to pay principal and interest payments for a government-issued bond for thirty years for the sake of buying something like police cars today that will most likely be decommissioned in less than five years time. By the time the debt that supported these kinds of expenses will be paid off, the benefits provided to the public will have been long forgotten.

When that kind of mismatch develops between the term of government-issued debt and the lifespan of the things it funds or sustains, it is a clear indication that the government has crossed the event horizon for its debt, which can now spiral out of control and become a debt death trap. In this situation, a government must issue ever-increasing amounts of debt to sustain the excessive spending ambitions of its politicians, who often will be long gone or perhaps even in prison by the time the bills they racked up through their fiscal malfeasance might fully be paid.

Unfortunately, that is the story of many local governments and municipalities around the United States, which are increasingly turning to bankruptcy proceedings to escape the fiscal recklessness of their civic leaders. And while it has not yet reached that point, it is today's developing story for the City of Chicago. The Chicago Tribune's Jason Grotto, Heather Gillers, Patricia Callahan and Alex Richards report:

When municipal officials want to build for the future, they have a powerful financial tool at their disposal: general obligation bonds that yield millions of borrowed dollars. The money is meant to let cities move forward on costly projects that will serve the community for decades.

But in an unprecedented analysis of Chicago’s finances, a Tribune investigation found that city officials have long abused their borrowing privileges, spending funds meant for long-term initiatives on problematic short-term expenses from library books to legal settlements.

Residents know little about it, as Illinois law doesn’t require Chicago to ask voters’ permission before issuing bonds. And when the city can’t pay what it owes, it uses yet more borrowed money as leverage to push off payments on old bonds.

This pattern of fiscal recklessness, which started under former Mayor Richard M. Daley, created a mountain of debt that threatens the financial future of the city. Now Rahm Emanuel is groping for ways to deal with the problem along with a looming pension crisis and chronic budget deficits.

Once a debt death trap begins, an ever-increasing portion of a government's spending must go to support its debt obligations. The interest rates that the increasingly fiscally-distressed government must pay to its lenders for new debt to sustain its spending also increase at the same time, because the lenders recognize that the government is less capable of making its debt payments from its available tax collections, so they must protect themselves from an increased risk of default by charging a higher price for the money they lend.

That vicious cycle then repeats and becomes amplified over time, which makes it more and more difficult to escape from that situation as the government's debt situation spirals out of control and it becomes stuck in a debt trap of the politicians' own making.

Faced with that situation, many politicians increasingly turn to tax hikes to try to balance their government's books, but these measures invariably fail because of how adversely they affect the local economy that supplies the tax revenue that supports the government's operations. The negative impact of these tax hikes create a massive fiscal drag that far outstrips the impact of what simply cutting their government's unsustainable amount of spending to more fiscally-responsible levels would have been, if only they had been willing to reduce their spending.

So why don't the politicians do the fiscally-responsible thing and reduce the amount of their spending to a more sustainable level long before it even puts the government at risk of a debt crisis?

In many cases, the unsustainable level of spending that puts their government at risk is really what the politicians promised to deliver to their political backers in exchange for the endorsements and campaign contributions that help put them in power, which is why they resist taking that responsible action so strongly. It is far more important to them to meet their backers' needs than those of regular citizens, and particularly so when their political backers gain so much from the government's spending.

In the end, the only way out is to make the political sacrifice and cut government spending to sustainable levels, while at the same time defaulting on their debt obligations and seeking relief through bankruptcy. The people who get hurt the most as that process plays out are the regular citizens whose real interests were being ignored by the politicians all along.

And how that process will play out is the real story that is developing in Chicago today.

Image credits: Ohio Department of Aging and Federal Bureau of Investigation.

Labels: ideas, national debt

Welcome to the blogosphere's toolchest! Here, unlike other blogs dedicated to analyzing current events, we create easy-to-use, simple tools to do the math related to them so you can get in on the action too! If you would like to learn more about these tools, or if you would like to contribute ideas to develop for this blog, please e-mail us at:

ironman at politicalcalculations

Thanks in advance!

Closing values for previous trading day.

This site is primarily powered by:

CSS Validation

RSS Site Feed

JavaScript

The tools on this site are built using JavaScript. If you would like to learn more, one of the best free resources on the web is available at W3Schools.com.

Other Cool Resources

Blog Roll