Imagine if one of the following bad and unexpected things has just happened to you.

- Your car broke down and you can't get to work.

- You injured yourself and you need to go to the emergency room.

- Something broke at your house and you need to get it fixed right away.

We hope that none of these things is an everyday occurrence for you. After all, if any of them were, they wouldn't really be unexpected and would be something for which you could specifically plan. But not these kinds of events. When things like these events happen, their timing is random and they come as a surprise. Being what they are, that often also means dealing with large and unexpected bills for you to pay.

While they may not be the kinds of things for which you may have a specific plan to address, they are exactly the kinds of things for which many personal finance experts recommend you have emergency savings to pay for, whether in part or in full. Emergency savings are perhaps the cheapest insurance you can have to deal with the unexpected costs of a personal emergency.

But how much do these kinds of emergency expenses cost? In truth, that's something that will vary a lot from person to person and the nature of the unexpected events themselves. There is however some average cost data for each of the unexpected event scenarios we've outlined, which might be useful in plan out how much you need to have for your emergency savings. Or at least seeing if they can handle the cost of a "typical" unexpected emergency event.

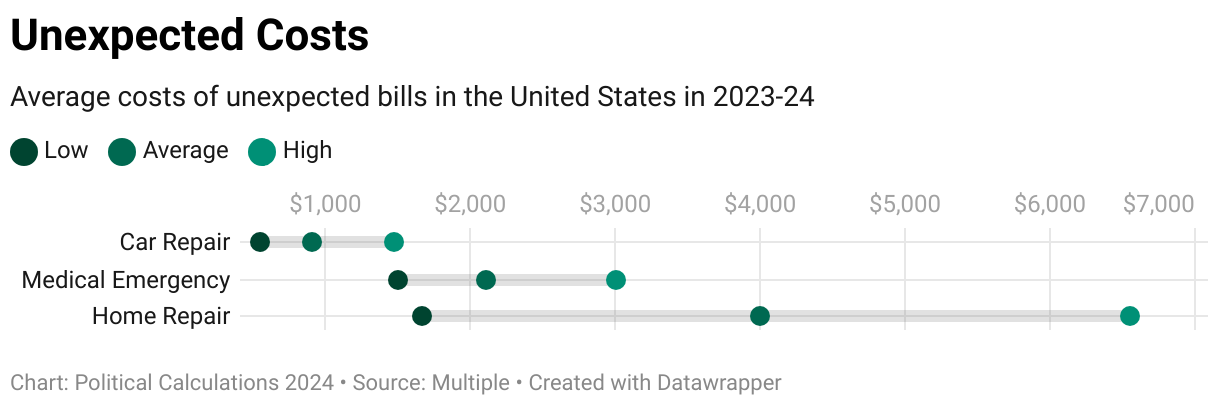

The following interactive chart presents a range of "average" costs for each of our unexpected scenarios. Please hover your cursor over the low, average, and high-end estimate to get the numbers for each scenario (if you've accessed this article on a site that republishes our RSS news feed, you may need to click through to our site to access a working version):

Here's where the numbers come from for each scenario:

- Car repair: The low estimate represents the average annual costs of car repairs from Cox Automotive, the parent of Kelley Blue Book, who also list the average costs for a variety of common car repairs in 2023. The "average" estimate is Consumer Affairs' 2024 estimate of the annual cost of maintaining and repairing a vehicle. The high estimate is from AAA and represents the average annual maintenance and repair bills reported by the insurer for 2023.

- Medical Emergency: The low, average, and high estimates are all taken from BetterCare's summary of the typical range for how much a visit to an Emergency Room costs in 2024. While other health insurance may cover part or all of the cost of bills you may have, you can still expect to have costs that it won't cover where this cost is a reasonable estimate for what those extra costs might be.

- Home repair: If you rent, these estimates may not apply. However, if you are or have aspirations of someday being a homeowner, the low estimate for an emergency home repair is from Angi's 2023 State of Home Spending report. The "average" estimate is provided from a 2022 survey conducted by Ipsos. The high estimate is from Thumbtack's 2023 estimate of the average annual cost of home maintenance and repairs.

A lot of these estimates are taken from the annual costs of "typical" maintenance and repair procedures. Since many of these unexpected events won't happen each year, you could aim at saving the "low" end estimates each year as your regular emergency savings plan or more if your income allows it, and build it up over time to where you can handle bigger emergencies. As for how much you might need to have altogether in any designated emergency savings you have, that's a different question for a different day.

Image credit: Car accident by shuets udono on Flickr. Creative Commons CC by-SA 2.0 Attribution-Sharealike 2.0 Generic Deed.

Labels: data visualization, ideas, personal finance

of white letters on a black surface photo by iridial on Unsplash")

If you spend any time working with the math of finance, you'll eventually encounter the Rule of 72. What is the Rule of 72? It is, quite simply, one of the most useful tools you can use to quickly approximate how long it will take to double your money in an investment that compounds annually. All you need is to take the percentage rate of return for your investment and divide it into the number 72. The result you get will be a good estimate of how many years it will take for the value of your investment to double.

Best of all, it's math you can do in your head. Which compared to the math formula you would need to use to get an exact answer otherwise, is lightning fast. Even if you were to use a calculator to do the exact math.

Sal Khan has a short video explainer describing the Rule of 72 that picks up after he uses the exact formula. What makes this video stand out from others is he goes the extra mile to answer the question of how good the Rule of 72 is at approximating the exact answer across a range of common rates of return that matter to investors.

Because the video picks up the discussion from examples of compounding interest, it might help to take a step back and start from the basic future value formula, which looks something like this for an investment that compounds annually:

Future Value = Present Value * (1 + Rate of Return)Time in Years

Since we want to find out how long it takes the value of the investment to double, we'll set "Future Value" to be equal to 2 times the "Present Value"

2*Present Value = Present Value * (1 + Rate of Return)Time in Years

At this point, since we now have "Present Value" on both sides of the equation, we can simplify the equation by dividing both sides by it. Doing that gives us the following result:

2 = (1 + Rate of Return)Time in Years

From here, if we want to solve this equation for "Time in Years", we'll need to deploy the magic of logarithms. Which for us, starts with taking the natural logarithm (ln) of both sizes of the equation:

ln(2) = ln[(1 + Rate of Return)Time in Years]

In this next step, we'll apply the power law of logarithms to transform the exponent math into simple multiplication on the right hand side of the equation:

ln(2) = Time in Years * ln(1 + Rate of Return)

We're almost there. We'll next solve for "Time in Years" by dividing both sides of the equation by ln(1 + Rate of Return). Here's the result:

ln(2)/ln(1 + Rate of Return) = Time in Years

In the final step, we'll swap the left and right hand side of the equation to make it easier to read by putting it into a more standard format:

Time in Years = ln(2)/ln(1 + Rate of Return)

To use this formula, the Rate of Return has to be written in a decimal format. For example, a rate of return of 6% would be written as 0.06 in the formula. And from here, you would be doing the same math Sal Khan was doing in the video, which we'll leave as an exercise for you if you really want to do it.

But why does the Rule of 72 work to closely approximate the exact result you get from the logarithm math we just showed? Steve Fiorino takes the explanation to the next level:

It may not be apparent at first glance how this exact equation is able to bring us to the rule of 72. For it to become clearer, input ln(2) into a calculator. It's an irrational number, but when you put it into the calculator by itself it will give you a number that it equals: 0.69314718056.

Or, phrased in another way, 69.3%.

That's how you get the rule of 69.3, but unless you're a math whiz who somehow memorized multiples of 69.3 it's still pretty difficult to do the equation. Thus, 70 and 72, which have more numbers that divide cleanly into them while still giving close approximations, became popular.

The Rule of 72 became the most popular version of this application because it has more whole number divisors that produce whole number results.

Perhaps more remarkably, the Rule of 72 for approximating the time it takes an investment to double in value predates the invention of logarithms! Here's WesBanco's description of its earliest use:

The Rule of 72 was first introduced in the late fifteenth century by the Franciscan friar and Italian mathematician Luca Pacioli. A contemporary of Leonardo da Vinci, Pacioli is considered by many to be the father of accounting. The Rule of 72 was introduced in his book Summa de arithmetica, geometria, proportioni et proportionalita, published in 1494 for use as a textbook for schools in what is now northern Italy.

Here's a link to Pacioli's 1494 book. Meanwhile, logarithms as we know them today weren't invented until John Napier developed them over a century later, publishing them in his 1614 book Mirifici logarithmorum canonis descriptio.

For what it's worth, the origin of the Rule of 72 can be attributed to earlier, unknown mathematicians who built it on a foundation of much older math that dates back centuries earlier, who recognized they could apply it to solve practical, real-world problems. However, it wasn't until after logarithms were invented that mathematicians could demonstrate why it works as well as it does.

Image credit: A number (72) of white letters on a black surface photo by iridial on Unsplash.

Labels: ideas, investing, math, personal finance

Hartford Funds has a fascinating white paper on the importance of dividends to the individual stocks that make up the S&P 500 (Index: SPX).

The paper builds on analysis done by Ned Davis Research, which considered how the stocks of dividend paying stocks performed when compared to non-dividend paying stocks within the index. What makes their analysis especially interesting is they also considered how changes in the firms' dividend policies affected the growth performance of their stocks, grouping them into several categories.

Before getting into more details, let's jump to perhaps their biggest finding. The following chart from the paper visualizes the stock performance for the various groups they defined over the fifty years from 1973 through 2023, as measured by how much $100 invested in 1973 in each grouping would have grown through the end of 2023.

")

In the following excerpt from the white paper, Hartford Funds describes how the companies of the S&P 500 were grouped according to their dividend policies and summarizes their most significant finding:

Do Dividend Policies Affect Stock Performance?

In an effort to learn more about the relative performance of companies according to their dividend policies, Ned Davis Research conducted a study in which it divided companies into two groups based on whether or not they paid a dividend during the previous 12 months. It named these two groups “dividend payers” and “dividend non-payers.”

The “dividend payers” were then divided further into three groups based on their dividend-payout behavior during the previous 12 months. Companies that kept their dividends per share at the same level were classified as “no change.” Companies that raised their dividends were classified as “dividend growers and initiators.” Companies that lowered or eliminated their dividends were classified as “dividend cutters or eliminators.” Companies that were classified as either “dividend growers and initiators” or “dividend cutters and eliminators” remained in these same categories for the next 12 months, or until there was another dividend change.

For each of the five categories (dividend payers, dividend non-payers, dividend growers and initiators, dividend non-payers, and no change in dividend policy) a total-return geometric average was calculated; monthly rebalancing was also employed.

It’s important to point out that our discussion is based on historical information regarding different stocks’ dividend-payout rates. Such past performance can’t be used to predict which stocks may initiate, increase, decrease, continue, or discontinue dividend payouts in the future.

Based on the Ned Davis study, it’s clear that companies that don’t pay dividends or cut their dividends suffered negative consequences. In FIGURE 7, dividend non-payers and dividend cutters and eliminators (e.g., companies that completely eliminated their dividends) were more volatile (as measured by beta5 and standard deviation)6 and fared worse than companies that maintained their dividend policy.

Lowest Risk and Highest Returns for Dividend Growers and Initiators

In contrast to companies that cut or eliminated their dividends, companies that grew or initiated a dividend have experienced the highest returns relative to other stocks since 1973—with significantly less volatility. This helps explain why so many financial professionals are now discussing the benefits of incorporating dividend-paying stocks as the core of an equity portfolio with their clients.

5 Beta is a measure of risk that indicates the price sensitivity of a security or a portfolio relative to a specified market index.

6 Standard deviation measures the portfolio's total-return volatility. A higher standard deviation indicates greater historical volatility.

Before going farther, it's also important to emphasize that these groupings are more dynamic than just companies changing groups whenever they changed their dividend policies. The membership of the S&P 500 has changed with the churn of firms being added and removed from the index over time, so there is survivor bias built into the results. The study is looking at how changes in dividend policy played out for this changing membership.

Let's look at the dynamics of changing dividend policy that applies for just one firm that has been part of the S&P 500 over the past 50 years: General Electric (NYSE: GE). Looking over its dividend history for a well-established company like GE, we see the firm would have been classified as a dividend grower during much of the period from 1973 through 2008 as the company became one of the largest components of the market capitalization-weighted S&P 500 index.

That status changed in 2009 as GE became a dividend cutter after the company became a basket case under its leadership in that era. Even though it remained poorly led for another decade, the company managed to rejoin the dividend grower list in 2010 and stayed on it until 2016 when it officially joined the "no change" group. In 2017, it rejoined the dividend cutter list and stayed on it until 2019, when its dividend bottomed and it once again rejoined the "no change" club. Since 2023, it has been a member of the dividend grower group in no small part because of improved management.

That recap of history brings us to a significant observation. Throughout much the period of the early 2000s during which GE was a member of the dividend grower group, its stock was underperforming. That underperformance occurred as investors looked ahead and anticipated the company that was becoming a basket case that would have to cut its dividend.

That means the growth of the dividend growers includes GE's underperformance in much of the early 2000s, which reduces its results. Amazingly, this category still outclasses all the other dividend policy categories by a notable margin. That's an impressive result.

We'll close by presenting Figure 7 from the white paper, which presents the average annual returns and volatility by dividend policy for the various grouped components of the S&P 500 index from 1973 through 2023.

")

The ultimate bottom line: Changes in a company's dividend-paying policies matter a lot!

References

Hartford Funds. The Power of Dividends: Past, Present, and Future. 2024 Insight White Paper. [PDF Document]. April 2024.

Labels: dividends, ideas, personal finance, SP 500

The market capitalization of new homes sold in July 2024 reached a record high, breaking the previous nominal record from August 2005 during the height of the housing bubble.

After months of hovering near or above a seven percent threshold, interest rates on a 30-year fixed rate conventional mortgage dropped below it in July 2024. While the amount of the change was small, new home buyers appear to have leapt upon the lower rates, racing to buy new homes during the month.

Consequently, July 2024 was the best month for new home sales since March 2022, when the U.S. Federal Reserve first started hiking interest rates in the United States to combat the inflation unleashed by the Biden-Harris administration's fiscal policies. The initial estimate of annualized new home sales is a seasonally-adjusted 739,000, which compares with a finalized sales count of 707,000 in March 2022.

That increase in sales was accompanied by a month-over-month increase in the average sale price of new homes sold in the U.S. The initial estimate of the average sale price of a new home sold in July 2024 is $514,800, which is up from a revised estimate of $501,700 for June 2024. For reference, the finalized estimate of the average sale price for a new home sold in March 2022 is $511,800.

The combination of the surge in new homes sold with average new home sale prices that remain well elevated has resulted in a spike in the U.S.' new home market cap. For new home builders, that's a welcome change because through June 2024, the industry had been experiencing stagnant growth.

The three following charts track the trends for the U.S. new home market capitalization, the number of new home sales, and their sale prices as measured by their time-shifted, trailing twelve month averages from January 1976 through July 2024.

New home sales trend picks up:

Prices on a slow uptrend:

July 2024's initial estimated trailing twelve month average new home market cap of $31.30 billion surpasses the $31.05 billion recorded in August 2005 in nominal (non-inflation adjusted) terms. Taking inflation into account, the size of the new home market in July 2024 is over 37% smaller in real terms than it was in August 2005.

Since mortgage rates have continued falling in August 2024, how that change will impact this month's sales has yet to be determined, in part because July 2024's elevated number of sales shrank the supply of new homes.

Lower mortgage rates provide that stimulus because they improve the affordability of new homes by reducing the monthly mortgage payments for equivalently priced homes. The downside of the mortgage math is that falling mortgage rates make it possible for home buyers to afford homes sold at higher prices, which will add an inflationary element to the new home market and U.S. economy.

References

U.S. Census Bureau. New Residential Sales Historical Data. Houses Sold. [Excel Spreadsheet]. Accessed 23 August 2024.

U.S. Census Bureau. New Residential Sales Historical Data. Median and Average Sale Price of Houses Sold. [Excel Spreadsheet]. Accessed 23 August 2024.

Image credit: Aerial Neighborhood photo by David McBee on Pexels. Public domain image.

Labels: market cap, real estate

Speaking at the Federal Reserve's annual retreat to Jackson Hole, Wyoming on Friday, 25 August 2024, Fed Chair Jerome Powell finally committed to cutting U.S. interest rates after months of playing "will they or won't they, even though everybody knows we're going to."

The S&P 500 (Index: SPX) responded to the Fed's commitment by rising 1.15%, ending the week at 5,634.61, up 1.45% from where the index closed out the preceding week.

That's less impressive than might have been predicted, but the level of the S&P 500 is consistent with investors focusing their attention on the current quarter of 2024-Q3. Investors have reason to do so because now the question at the center of billions of investment decisions is no longer "will they cut?" or "when will they cut?" but instead is now "how much will they cut?"

The CME Group's FedWatch Tool continues to anticipate the Fed will hold the Federal Funds Rate steady in its current target range of 5.25-5.50% until 18 September (2024-Q3). On that date, the Fed is expected to start a series of 0.25%-0.50% rate cuts that will occur at six-week intervals well into 2025.

In the latest update for the alternative futures chart, we find the trajectory of the S&P 500 running just above the top end of the redzone forecast range.

- Snapshot on 23 Aug 2024")

As regular readers will recall, that redzone forecast range is based on the assumption that investors would be shifting their forward looking attention from the distant future quarter of 2025-Q2 toward the nearer term quarter of 2024-Q4 during the period it covers. Instead, the Fed's long-awaited commitment to cutting rates has prompted investors to draw their attention back to the current quarter, which is why the S&P's trajectory has settled where it has without any more impressive change in its level on the biggest news of the week. If we were to re-draw the redzone forecast range to show that adjustment, the actual trajectory of the S&P 500 would fall well within the projected range.

As it is, without dramatic new information to compel it to perform otherwise, we think the S&P 500's trajectory will increasing converge with the redzone forecast range shown on the chart because investors will have no reason to maintain their focus on the current quarter for much more than the next four weeks and will once again reset their forward time horizon. We think the next change will involve them shifting their attention toward 2024-Q4, which the redzone forecast range already assumes will happen.

Meanwhile, other things happened during the week that was, here are the week's market moving headlines:

- Monday, 19 August 2024

-

- Signs and portents for the U.S. economy:

- US regional bank deals rise as lenders aim to bolster balance sheets

- Oil price dip keeps Brent below $80 on China demand woes

- Fed minions now expected to deliver three rate cuts in rest of 2024, to signal upcoming policies at Jackson Hole event:

- Nasdaq, S&P, Dow end higher as investors wait for Powell Jackson Hole’s speech

- Tuesday, 20 August 2024

-

- Signs and portents for the U.S. economy:

- Fed minions paying more attention to soon-to-be revised jobs data:

- Bigger trouble developing in China:

- BOJ minions now expecting wage inflation, but won't do much about it:

- ECB minions thinking about next Eurozone rate cuts, may have caught a break with German wage inflation:

- ECB may need to cut rates again in Sept, Rehn says

- German negotiated wage growth slows in likely relief for ECB

- Nasdaq, S&P, Dow end lower, break win streaks as investors cast eye toward Fed rate views

- Wednesday, 21 August 2024

-

- Signs and portents for the U.S. economy:

- US job growth in year through March was far lower than estimated

- US Jobs Revised Down By 818,000 In Election Year Shocker, Second Worst Revision In US History

- US Bureau of Labor Statistics under scrutiny again for latest data misstep

- Oil slips on higher US crude stocks, easing Middle East tensions

- Fed minions thinking about when, how much to cut U.S. interest rates:

- Bigger bailouts developing in China:

- BOJ minions seeing Japan's export economy slow, majority of economists think they'll be forced to hike rates in Japan again this year:

- Japan's July export growth lags expectations, volumes fall again

- BOJ to raise rates again by end-year, say 57% of economists - Reuters poll

- S&P, Nasdaq, Dow end higher after Fed minutes point to rate cuts beginning in September

- Thursday, 22 August 2024

-

- Signs and portents for the U.S. economy:

- US business activity edges lower; pricing power ebbs further

- US existing home sales rise more than expected in July

- Fed minions getting excited to start cutting U.S. interest rates, claim there won't be any recession:

- Fed's Schmid signals open mind on September rate cut

- Fed's Harker is ready to start methodical course of rate cuts

- Fed's Collins: will soon be appropriate to cut interest rates

- Fed has 'clear path' to achieving goals without recession, Collins says

- Slowing decline in Japan's factory output:

- BOJ minions influencing global central bank policies as synchronized Japanification spreads:

- ECB minions get summer boost from Olympics, looking forward to next rate cut:

- Euro zone business activity gets boost from Olympics, PMI shows

- ECB policymakers shift focus to September meeting

- Nasdaq slumps, S&P, Dow end down ahead of Powell's potential signal on rate-cut sizing

- Friday, 23 August 2024

-

- Signs and portents for the U.S. economy:

- US job market may be near tipping point, research shows

- Oil climbs over 2% after Fed's Powell indicates US rate cuts

- New homes sales rise 10.6% in July spurred by lower mortgage rates

- Fed minions commit to cutting U.S. interest rates in September 2024:

- Fed's Powell, in policy shift, says 'time has come' to cut rates

- Fed policymakers flag rate cuts as job market cools

- Studies find Fed actions more impactful than words, use mortgage bonds to influence economy's momentum:

- Fed's actions spoke louder than words in inflation fight, research shows

- Fed mortgage bond holdings play 'central' policy rule, paper says

- BOJ minions looking at stagflation, claim's they'll get a benefit from Fed rate cuts:

- Japan's core inflation picks up, but demand-driven growth below 2%

- Fed's dovish shift a mixed blessing for BOJ rate hike plan

- ECB minions getting excited to cut Eurozone interest rates again:

- Exclusive: ECB policymakers' views converging on Sept rate cut, sources say

- ECB making good progress but job not done, Lane says

- S&P, Nasdaq, Dow end higher after Powell says rate cuts are in the pipeline

The Atlanta Fed's GDPNow tool's projection of the real GDP growth rate for the current quarter of 2024-Q3 remained at +2.0% with no updates taking place during the past week. It will next be updated during the upcoming week.

Image credit: Microsoft Copilot Designer. Prompt: "An editorial cartoon of Federal Reserve officials dancing to celebrate interest rate cuts with a banner at the top that says 'IT'S RATE CUTTING TIME!'" We're not sure why three of the dancing Fed officials are Fed Chair Jerome Powell, but we're running with the assumption that the AI was trained on images of the "Dancing Itos" from the era of the O.J. Simpson trial in the 1990s and couldn't help itself....

There are a lot of factors that can influence the quality of your experience of flying on a commercial airline. But what are the big ones that have the most impact on how passengers judge how good their flying experience is?

Back in 2015, the flight booking company Skyscanner surveyed 2,000 international passengers to find out what they felt mattered most. They identified three big things affected how passengers evaluated the quality of their flight:

- Time of Day for Departure. This factor is important because it directly affects the things you can do either before or after your flight.

- Seat Pitch (or Legroom). This factor directly affects how physically comfortable you can expect to be on your flight. As a general rule, the more you have, the more likely you will be comfortable.

- Punctuality at Arrival. Keeping in mind that the whole point of flying is to get where you're going, getting there on time is almost just as big a deal, because it affects how everything you plan to do after you get to your destination will actually happen. Or doesn't happen, as might be the case if your flight is excessively delayed.

But Skyscanner took it to the next level. They worked with a statistician at the University of Sheffield to create a formula that you can use to find out, before you fly, how good your flight is likely to be. And we've taken that math and built the following tool you can use when planning your next flight!

Just enter the indicated information, following the links we've provided to get it if you don't have it handy, click the "Calculate" button and the tool will do the rest. If you're accessing this article on a site that republishes our RSS news feed, please click through to our site to access a working version.

We've set two of the three defaults for options that will likely result in a good flying experience for you, and one that won't. The one that probably won't is the seat pitch, which we set at a value that's consistent with what you'll find in "Economy" class.

As for the Potential Flight Quality Score, here's the decoder ring for interpreting the tool's results:

- 10 or less: Not good

- 10 to 14: Okay

- 14 or more: Good

Playing with the various options, we found it surprising at how much the seat pitch influences the tool's results. Most combinations we tried with typical seat pitch dimensions result in flights that most passengers would not describe as either good or okay. Which if you think about it, is pretty consistent with what most passengers experience when they fly today.

Image credit: Black leather airplane seats photo by Douglas O on Unsplash.

Labels: personal finance, tool

The Federal Reserve has a tough job. It must use monetary policy to achieve two goals for the U.S. economy: stable prices and maximum employment.

Doing its job requires Federal Reserve officials to pay close attention to a lot of data, which ideally, would be of high quality. After all, both jobs and the control of inflation are on the line. Having accurate, high quality data is needed to make achieving the Fed's dual goals possible.

Unfortunately, a lot of the data on which they rely hasn't been passing muster in recent years, particularly employment data reported by U.S. government agencies. The situation has gotten bad enough that Fed officials have been openly complaining about it for months. In their view, the contemporary employment data is becoming less than useful.

Here's an example discussing how bad data in 2021 caused the Fed to badly misread the true state of the U.S. economy.

Federal Reserve officials have said countless times they take a “data-dependent approach” to their policy decisions, including their current conundrum of when to slash interest rates. But what if the data isn’t as dependable as it once was?

That’s what appears to be happening — and it’s making central bankers’ jobs a lot harder.

“We have to make decisions in real time,” Fed Governor Christopher Waller said late last year. “Whatever data is released, that’s the data I have to use. The problem with data is it gets revised.”

That wouldn’t necessarily be so much of an issue if the revisions, which can come months after initial reports are released, were relatively small. However, many revisions over the past few years have been game-changers.

For instance, Waller pointed out that initial monthly headline employment numbers for 2021 led him to believe that the job market was “okay, but it’s not really great.” Even though inflation was at a 40-year high, he and other Fed officials were under the impression that they’d need to proceed very carefully with raising interest rates, fearing it could lead to job losses, Waller said.

In reality, the job market was much stronger than the numbers indicated after state and local governments lifted their pandemic lockdowns, which added to the inflation unleashed in 2021, making it much more difficult to contain. Getting the data wrong, as in this example, literally imposed a higher cost of living on all Americans.

That situation involved the U.S. government's employment data failing to capture the true number of Americans who went back to work after being forcibly idled by the lockdowns. Let's flash forward to today, where the opposite situation has just taken place. The U.S. government has failed once again to accurately account for the number of working Americans, only this time, it has overcounted them. Job growth in the U.S. has been "far weaker than initially reported":

US job growth during much of the past year was significantly weaker than initially estimated, according to new data released Wednesday.

The Bureau of Labor Statistics’ preliminary annual benchmark review of employment data suggests that there were 818,000 fewer jobs in March of this year than were initially reported.

Every year, the BLS conducts a revision to the data from its monthly survey of businesses’ payrolls, then benchmarks the March employment level to those measured by the Quarterly Census of Employment and Wages program.

The preliminary data marks the largest downward revision since 2009 and shows that the labor market wasn’t quite as red hot as initially thought.

Here's how that matters to Federal Reserve officials:

Both Chicago Fed president Austan Goolsbee and San Francisco Fed President Mary C. Daly said the central bank was closely watching unemployment to gauge whether to cut rates and if so, how much to cut by.

And last week, Atlanta Fed president Raphael Bostic told the Financial Times that he was open to the idea of the central bank cutting interest rates at its next meeting in September, and that the Fed has to be “extra vigilant.”

“Because our policies act with a lag in both directions, we can’t really afford to be late. We have to act as soon as possible,” he said.

That's what's at stake. If jobs were really as strong as the data had previously indicated, Fed officials would every reason to continue acting as if job growth in the U.S. economy were not slowing, which is what they have been doing for much of the past year.

One of the outcomes of that are news stories that point to the bad jobs data as if it's an accurate description of reality and treat the people affected by the true lackluster performance of the U.S. job market like they're idiots. Here's an example of that phenomenon, which is coincidentally from the same article quoting the Fed officials paying close attention to unemployment data:

The economy may look strong on paper, but Americans are more worried than ever about losing their jobs as fears of a “vibecession” take hold.

The portmanteau “vibecession,” coined by Gen-Z economist and TikTok star Kyla Scanlon, refers to the disconnect that occurs when public financial sentiment is negative even though the economy isn’t in a recession. Given the growing chasm between the stock market and job anxiety, the phenomenon appears to be in full swing.

In truth, that Gen-Z TikTok influencer hot take had a one-day shelf life. It was quickly debunked by the second largest-ever downward revision to the Bureau of Labor Statistics employment data in the bureau's history. Only 2009 has seen a larger downward revision, during the Great Recession.

It would seem that public sentiment is not as misplaced as that initidata, now recognized to have been far off target, had suggested. The revised data, such as it is, still suggests the U.S. job market improved over the past year, but with far less growth than had previously been claimed. The one thing we know for sure is the economy is not anywhere near as strong as the previous data had claimed.

The bottom line is the BLS has some serious work ahead of it to improve the quality of its employment data collection. Getting it so far off target and letting it stay wrong for so long is making it harder for decision makers to put forward the policies that are truly needed when they are needed. In the case of Federal Reserve officials who rely on that data, getting the data wrong has costs that ripple all the way through the economy.

Image credit: Useless information by Curly via Flickr. Creative Commons. Attribution-NonCommercial 2.0 Generic License (CC BY-NC 2.0).

Labels: ideas

.")

There were some very small changes for the outlook of the quarterly dividends of the S&P 500 (Index: SPX) through the rest of 2024.

On the plus side, the outlook for dividends being paid in the current quarter of 2024-Q3 improved since the snapshot we took on 19 July 2024. The quarter's dividend futures contracts rose by six cents per share, bringing 2024-Q3's projected payout for the S&P 500 to $18.35 per share.

On the negative side of the ledger, the outlook for the final quarter of 2024 dimmed slightly. Going into 16 August 2024, the S&P 500's anticipated dividend payout for 2024-Q4 declined by eight cents to $18.82 per share.

Combined, that's a net negative two cent change in the index' dividends projected to be paid out before the end of 2024, which is to say that not much changed in the overall outlook over the past month.

The following animated chart shows these changes in the expectations for dividends in the month from our 19 July 2024 snapshot to our 16 August 2024 snapshot:

More About Dividend Futures Data

Dividend futures indicate the amount of dividends per share to be paid out over the period covered by each quarter's dividend futures contracts, which start on the day after the preceding quarter's dividend futures contracts expire and end on the third Friday of the month ending the indicated quarter. So for example, as determined by dividend futures contracts, the now "current" quarter of 2024-Q3 began on Saturday, 22 June 2024 and will end on Friday, 20 September 2024.

That makes these figures different from the quarterly dividends per share figures reported by Standard and Poor. S&P reports the amount of dividends per share paid out during regular calendar quarters after the end of each quarter. This term mismatch accounts for the differences in dividends reported by both sources, with the biggest differences between the two typically seen in the first and fourth quarters of each year.

Image Credit: Microsoft Copilot Designer. Prompt: "A crystal ball with the word 'SP 500' written inside it". And 'Dividends' written above it, which we added.

Labels: dividends, forecasting, SP 500

.")

Every three months, we take a snapshot of the expectations for future earnings in the S&P 500 (Index: SPX) at approximately the midpoint of the current quarter, shortly after most U.S. firms have announced their previous quarter's earnings.

The recovery from 2022's earnings recession for the S&P 500 is now complete with the index' earnings per share in June 2024 finally rising above its pre-recession peak recorded back in March 2022. Earnings per share in the S&P 500 had fallen by 12.7% from March 2022 to December 2022 before their slow and uneven recovery over the following eighteen months.

By contrast, the recovery from 2020's Coronavirus Pandemic Recession was much quicker, with the index taking less than two quarters to fully regain the earnings per share it lost after the government mandated lockdowns that shuttered economic activity were lifted.

Looking forward to the ends of 2024 and 2025 respectively, Standard and Poor is now projecting slightly lower earnings per share for the S&P 500 than they had in their 14 May 2024 forecast. S&P's projected earnings per share for December 2024 is $216.65 per share, while December 2025's earnings per share are now anticipated to come in at $250.87 per share.

All these developments are shown on the following chart:

If we include the near-zero rate of earnings per share growth the S&P 500 saw from December 2021 to March 2022, the S&P 500's earnings recession fully overlaps the two quarters of negative real GDP growth the U.S. economy went through in the first half of 2022 as inflation unleashed by the Biden-Harris administration raged out of control. As it was, the earnings of the companies that make up the S&P 500 index had enough positive momentum coming out of 2021 to record a positive gain in the first quarter of 2022 of just four cents per share over the previous quarter's level, which is why it narrowly avoids being included in the earnings recession.

Reference

Silverblatt, Howard. Standard & Poor. S&P 500 Earnings and Estimates. [Excel Spreadsheet]. 13 August 2024. Accessed 17 August 2024.

Image Credit: Microsoft Copilot Designer. Prompt: "A crystal ball with the word 'SP 500' written inside it". And 'Earnings' written above it, which we added.

Labels: earnings, forecasting, SP 500

There's one thing we know for sure about stock price volatility. Big moves, whether up or down, tend to be clustered together.

During the last several weeks, a new cluster of volatility formed in the U.S. stock market. The S&P 500 (Index: SPX) experienced a large downward move after being triggered by a noise event that arose in Japan's stock market. That event was followed by a week of recovery, which in turn, has been followed in the past week by large upward moves in the level of the S&P 500.

By the closing bell on the trading week ending on Friday, 16 August 2024, the index rose to 5,554.25, more than 210 points and 3.93% higher than where it closed in the previous week. The upward moves coincided with the arrival of new information suggesting the perceived risk of recession in the U.S. economy is much lower than other data signaled just a few weeks earlier.

The result was several unusually large upward moves in the level of the S&P 500, which are captured in the latest update to the dividend futures-based model's alternative futures chart.

- Snapshot on 16 Aug 2024")

Assuming investors are still focusing on the distant future quarter of 2025-Q2 as they have in the last several weeks, these upward movements have put the trajectory into the upper part of the redzone forecast range we've added to the alternative futures chart. This forecast range runs through 1 November 2024 and is based on the assumption that investors will shift their forward looking attention toward the nearer term future of 2024-Q1 as we get closer to the end of 2024.

We've added this new forecast range because we've entered a period where we know in advance the dividend futures-based model's projections will be affected by the echoes of the past volatility of stock prices for a prolonged period. This situation arises a result of the model's use of historic stock prices as the base reference points from which it projects their future. When that historic data captures previous volatility in stock prices, it skews the model's projected future for stock prices. We compensate for this echo effect by bridging across the period in which we know the past volatility of stock prices will affect the model's raw projections, which we show on the chart using a red-shaded forecast range.

But enough about dry technical details. Here's our summary of the past week's market-moving headlines, which we present to document the random onset of new information that investors absorbed as they went about setting the level of stock prices during the week that was.

- Monday, 12 August 2024

-

- Signs and portents for the U.S. economy:

- Oil prices jump on prospect of widening Middle East war shrinking supply

- Shrinking cash cushions may pinch US consumer spending, SF Fed report says

- Fed minions don't say "recession" but claim rate cuts will be needed if inflation falls:

- Fed's Bowman: Rate cuts will be needed if inflation keeps falling

- Fed hawks and doves: The latest from US central bankers

- Bigger bond market bailout developing in China:

- Nasdaq, S&P, and Dow finished mixed as investors await inflation data

- Tuesday, 13 August 2024

-

- Signs and portents for the U.S. economy:

- Oil tumbles on easing fears of wider Middle East war

- US producer inflation slows as pricing power diminishes

- US manufacturers hit by soaring property insurance costs

- Fed minions still signaling U.S. interest rate cuts are coming soon:

- Bigger trouble, stimulus developing in China:

- China new loans hit 15-year low in July, more policy steps expected

- What is the Chinese yuan carry trade and how is it different from the yen's?

- BOJ minions to get a stern talking to:

- Nasdaq ends up 2%, S&P, Dow rise as cooling wholesale inflation feeds rate-cut views

- Wednesday, 14 August 2024

-

- Signs and portents for the U.S. economy:

- US consumer prices increase as expected in July

- US annual consumer price increase slows to below 3% as inflation ebbs

- July CPI supports disinflation scenario for Sept ease

- Brent oil holds above $80 as fears over Middle East ease

- Oil prices settle 1% lower after surprise rise in US crude stockpiles

- Slowing global jet fuel consumption adds to oil demand concern

- US junk debt investors cautious of leveraged loans as economy slows

- Possible US seaport strike could back up goods for months, shipping experts say

- Bigger trouble, stimulus developing in China:

- More central banks start cutting their domestic interest rates:

- S&P 500 ends up, win streak at 5; Nasdaq ekes out gain even as Alphabet weighs

- Thursday, 15 August 2024

-

- Signs and portents for the U.S. economy:

- Oil prices rise on hopes of US rate cuts boosting fuel demand

- US corporate bond spreads recover on promising economic data

- Fed minions starting to get rate cut mania:

- Bigger trouble developing in China:

- China's factory output slows, dashing speedy recovery hopes

- China's diesel demand fell in June by most in three years, US EIA says

- China's home-price slump deepens to new 9-year low despite stimulus

- BOJ minions get data they really didn't want to get, expected to roll over under pressure from JapanGov minions:

- Japan's economy rebounds strongly on consumption boost, backs case for more rate hikes

- Political uncertainty may prod BOJ to pause, but not end, rate hike path

- Nasdaq closes up 2%, S&P, Dow advance as growth view brightens; Walmart soars

- Friday, 16 August 2024

-

- Signs and portents for the U.S. economy:

- Oil falls more than $2, set for weekly decline on China worries

- Hurricane Beryl, excess inventory pressure US single-family homebuilding

- Fed minions claim they don't want to tighten monetary policy longer than they need to:

- Bigger trouble, stimulus developing in China:

- China's spending slump weighs as e-commerce giant Alibaba misses estimates

- China's faltering growth revives cash vouchers talk

- Central banks signaling more rate cuts to come:

- Dow, S&P, Nasdaq finish in the green, mark strongest week so far in 2024

The CME Group's FedWatch Tool continues to anticipate the Fed will hold the Federal Funds Rate steady in a target range of 5.25-5.50% until 18 September (2024-Q3). On that date, the Fed is expected to start a series of 0.25% rate cuts that will occur at six-week intervals well into 2025.

The Atlanta Fed's GDPNow tool's projection of the real GDP growth rate for the current quarter of 2024-Q3 dropped to +2.0% from its forecast of +2.9% growth a week earlier.

Image credit: Microsoft Copilot Designer. Prompt: "An editorial cartoon of a Wall Street bull dancing to celebrate the best week for the S&P 500 in 2024".

Welcome to the blogosphere's toolchest! Here, unlike other blogs dedicated to analyzing current events, we create easy-to-use, simple tools to do the math related to them so you can get in on the action too! If you would like to learn more about these tools, or if you would like to contribute ideas to develop for this blog, please e-mail us at:

ironman at politicalcalculations

Thanks in advance!

Closing values for previous trading day.

This site is primarily powered by:

CSS Validation

RSS Site Feed

JavaScript

The tools on this site are built using JavaScript. If you would like to learn more, one of the best free resources on the web is available at W3Schools.com.

Other Cool Resources

Blog Roll