We can sum up the final chapter of The Boglehead's Guide to Investing,

We can sum up the final chapter of The Boglehead's Guide to Investing, by Taylor Larimore, Mel Lindauer and Michael LeBoeuf in one word: motivation.

This is true for any good book on investing that you will ever read. The final chapter is always about taking the key points made in the book and putting them to work.

But what are the key points you should take away from the book? The last chapter is also the authors' last chance to really underscore the points they believe are the most important they made in writing the book. Here's our list of the authors' key points with links to the corresponding posts reviewed by other members of The Boglehead's October Project:

- Choose and live a sound financial lifestyle.

- Start to save early, invest regularly and diversify your investments!

- Don't invest in things you don't understand.

- Pay attention to investing costs and especially taxes!

- Plan! Plan! Plan! Plan! Plan! Plan! Plan!

- Avoid fads and master your emotions.

While All Financial Matters provides a better guide to the topics listed above, we hope you get the gist of what the Bogleheads advocate....

One theme that the Bogleheads consistently communicate is that you're not in it alone. To that end, the other offer the Bogleheads bring to the table in the final chapter of the book is access to the Boglehead community, where you can interact online with the groups members to find answers to the unique questions you might have for your situation.

The only question left now is whether or not you've learned or re-learned enough from The Boglehead's Guide to Investing and are enthusiastic enough about what you've read to go out and bet your life's earnings on it. That's really what the Bogleheads are all about: taking solid and time-tested lessons in minimizing the risks of investing and putting them to work to build a more comfortable life.

Are you ready?

More at Political Calculations

If this is your first visit to Political Calculations, come try out our Investing Tools. But wait, that's not all! We've also built tools dedicated to solving the problems of personal finance, economics and other really interesting topics. You'll find your key to all our tools at the User's Guide to Political Calculations!

It's a glorious Monday when we can celebrate two new Trunk Monkey ads! Our hero saves the day twice - first giving first aid (QuickTime, Windows Media), then defeating aliens (QuickTime, Windows Media)!

Speaking of inspired ads, the "Real Men of Genius" series for Bud Light (must be over 21 years old) has to be among the funniest collection of radio spots ever. The best of the current batch: "Mr. Overzealous Foul Ball Catcher"!

After the St. Louis Cardinals became the 2006 World Champions after upsetting the favored Detroit Tigers in St. Louis, fans stayed at the stadium for hours after the game. Turns out they may not have just been celebrating, as the city has also claimed first place in being the Most Dangerous City in the U.S. - again beating Detroit, which was the second most-dangerous city.

It's time, once again, for Political Calculations review of the best business and money-related posts of the week that was On the Moneyed Midways! Each week, we plow through a dozen or more blog carnivals, seeking out the posts most worth reading. And, each week, we award one post with the title of being The Best Post of the Week, Anywhere!(TM)

It's time, once again, for Political Calculations review of the best business and money-related posts of the week that was On the Moneyed Midways! Each week, we plow through a dozen or more blog carnivals, seeking out the posts most worth reading. And, each week, we award one post with the title of being The Best Post of the Week, Anywhere!(TM)

Reading as many blog carnivals as we do, we find that there are a handful of writers whose posts are routinely excellent. At some point, we're going to go through all our back issues and put together a special edition highlighting the best writers we've found in our reviews of the multitude of blog carnivals. Something to watch for at the end of the year!

| On the Moneyed Midways for October 27, 2006 | |||

|---|---|---|---|

| Carnival | Post | Blog | Comments |

| Carnival of Business | What My Father Taught Me About Business: Endless Fools | My 1st Million at 33 | Frugal reveals how smart shopping doesn't involve listening to salespeople (who lie), but instead on doing your homework. |

| Carnival of Career Intensity | The Secret of Highly Productive People | Unleash Your Potential | My Bubble Life defines what "the flow", the secret of the highly productive, is, then shows how to get into it. |

| Carnival of Fraud | Your Ultimate Guide to Identity Theft Prevention | Your Credit Advisor | The Credit Advisor provides tips on how to avoid having your identity stolen. Absolutely, positively The Best Post of the Week, Anywhere!. Very well done! |

| Carnival of Home Business | Deduct New Business Costs | Gina's Tax Blog | Gina Gwozdz reports that those launching new businesses can deduct the costs of doing so on their taxes, even before they officially open up shop! |

| Carnival of Personal Finance | Paying Off Old Past Due Bills Without Hurting Your Credit | Searchlight Crusade | Dan Melson uncovers how to pay off those old bills in ways that won't dent your credit score. |

| Carnival of Personal Finance | The Real Return on My Rental Property | 2million | 2million is new to the world of property rental, and shares the results (and lessons) of the first 12 months of renting out his first home. |

| Carnival of Project Management | Quickie Time Tracking | Work, in Plain English | Penina S. Finger (don't ask us) takes pencil to napkin to reveal the mysteries of managing time on projects. |

| Carnival of the Capitalists | Better Investment in Education | Gongol.com | Brian Gongol has a better idea on how states and local governments can use the money they spend on economic "development" - putting it toward schools instead! |

| Cavalcade of Risk | Costs vs. Spending | Cato @ Liberty | There is, Michael Cannon points out, a fundamental difference between costs and spending. |

| Festival of Frugality | Who Wants to Play the Paper Bag Game? | Blogging Away Debt | Tricia shows how a paper bag can be the key to your getting a grip on your weekly spending habits. |

| Festival of Investing | Getting the Most from a Savings Account | How Do People Get Rich? | Capital One is mostly known for its credit cards, but David B. finds they're a real bank with great rates on their savings accounts. |

| Festival of Stocks | Why Microsoft Should Disband | Search Engine Stocks | Chris proposes that Microsoft ought to be broken up into five or six pieces. |

| Personal Development Carnival | How to Know Who You Are in 20 Minutes | A Better You Blog | Patricia outlines a method for getting to the core of who you are in as little as twenty minutes. |

| Wealth Building Ideas | Out of the Mouths of Babes - A Mortgage Lesson | Wisdom from Wenchypoo's Mental Wastebasket | Wenchypoo shares an anecdote of a 6 and 8-year old who truly understand opportunity costs! |

Previous Editions

- On the Moneyed Midways – October 27, 2006

- On the Moneyed Midways – October 21, 2006

- On the Moneyed Midways – October 13, 2006

- On the Moneyed Midways – October 6, 2006

- On the Moneyed Midways – September 30, 2006

- On the Moneyed Midways – September 23, 2006

- On the Moneyed Midways – September 15, 2006

- On the Moneyed Midways – September 8, 2006

- On the Moneyed Midways – September 1, 2006

- On the Moneyed Midways – August 25, 2006

- On the Moneyed Midways – August 19, 2006

- On the Moneyed Midways – August 11, 2006

- On the Moneyed Midways – August 4, 2006

- On the Moneyed Midways – July 29, 2006

- On the Moneyed Midways – July 21, 2006

- On the Moneyed Midways – July 14, 2006

- On the Moneyed Midways – July 7, 2006

- On the Moneyed Midways – June 30, 2006

- On the Moneyed Midways – June 23, 2006

- On the Moneyed Midways – June 16, 2006

- On the Moneyed Midways – June 9, 2006

- On the Moneyed Midways – June 2, 2006

- On the Moneyed Midways – May 26, 2006

- On the Moneyed Midways – May 19, 2006

- On the Moneyed Midways – May 12, 2006

- On the Moneyed Midways – May 5, 2006

- On the Moneyed Midways – April 28, 2006

- On the Moneyed Midways – April 21, 2006

- On the Moneyed Midways – April 14, 2006

- On the Moneyed Midways – April 7, 2006

- On the Moneyed Midways – March 31, 2006

- On the Moneyed Midways – March 24, 2006

- On the Moneyed Midways – March 31, 2006

- On the Moneyed Midways – St. Patrick's Day 2006 Edition

- On the Moneyed Midways – March 10, 2006

- On the Moneyed Midways - The inaugural edition from March 3, 2006!

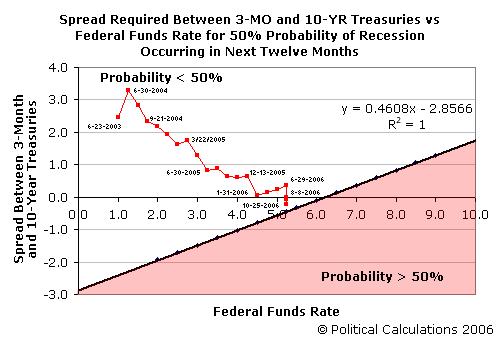

The Federal Reserve's Open Market Committee announced yesterday that they would be leaving the Federal Funds Rate unchanged at 5.25%.

Using Political Calculations' recession probability tool, which determines the odds that the U.S. economy will enter into a recession sometime in the next 12 months, we find that the current probability of recession in the U.S. is 43.4%. This figure is based on the current level of the Federal Funds Rate and the yields at market close of the 3-Month Treasury (4.98%) and the 10-Year Treasury (4.76%) on October 25, 2006.

We've also updated our chart that tracks the odds of recession since the Federal Reserve began it's most recent series of rate hikes:

Since the last FOMC meeting, the odds of recession have largely held stable in the lower 40 percents. While the probability of recession has increased slightly since the Fed last left interest rates unchanged, it is still within a narrow range it has been since the Fed set the 5.25% rate in June 2006. The peak occurred in late August as the probability of recession reached slightly over 45%.

In other words, "Move along. Nothing to see here people", which more or less expresses the market's reaction to the Fed's announcement.

Craig Newmark cited our humble blog yesterday, remarking that:

One tool that I think I'll use the next time I preach to high schools about saving money is "Best and Worst Case Stock Market Investing".

Our tool for mapping the inflation-adjusted extremes of the performance of the total U.S. stock market is definitely one of our favorites, and our Lemony Snicket vs. King Midas tool is based upon it - but it does leave an open question that we often have to answer: How does the performance of the total stock market compare to the S&P 500?

We understand why. The S&P 500 is, after all, *the* benchmark against which all stock market investing performance is measured.

To date, we've only answered half the question in mapping the historical performance extremes of the S&P 500 index, and building a tool to estimate the best, worst and average performance of the S&P 500 for investments of any holding period.

To date, we've only answered half the question in mapping the historical performance extremes of the S&P 500 index, and building a tool to estimate the best, worst and average performance of the S&P 500 for investments of any holding period.

Today, we'll answer the rest of the question by taking our mathematical model of the S&P 500's performance extremes and using it in the behind-the-scenes math of our Lemony Snicket tool! Now, you can find out what your actual returns would be if you make a fixed, once-a-year investment in the S&P 500 (like a lot of people do with their IRAs!), and you consistently get the best, average or worst case historical performance ever achieved by the index!

What's more, you can even play with the effects of inflation on your hypothetical absolute best, average and worst case performance! Our default value of 2.5% is the median average inflation rate (as measured by CPI-U) for all 30-year periods between 1871 and 2000, and we'll note for your reference that the worst 30-year period of inflation recorded in that period is 5.41%. You can see a small sample of this data in this Word document from Global Financial Data.

What value for inflation should you use for your investing horizon? The median average inflation rate will be the best representative of inflation for any holding period, but you should adjust this figure to consider a range of values above and below this quantity. As a general rule of thumb, the longer your investing horizon, the smaller the range around the 2.5% value you should consider.

Update (30 December 2006): Don't say we don't learn anything! We went and found the highest, lowest and average rates of inflation for the U.S. since 1913 and changed the default value in the tool below to match what we actually found. Plus, the tool we created in the link above will provide you with the range of historical values you need to consider!

As an added bonus, we've also expanded the range for the possible investing holding periods all the way out to 100 years! And why not? We've got the data to back it up....

The Total Amount Invested "Unadjusted for Inflation" is the amount that you actually contributed to your investment over the entire investing period. The "Adjusted for Inflation" amount shows how much this money would be worth at the end of the investing period if you used it to stuff your mattress instead (which we note for short periods of time can be a valid investment strategy....)

And to finally answer the question of how the performance of the total stock market compares to the S&P 500, well, all you need to do is to compare the results above with those in the original Lemony Snicket tool!

Labels: best case, investing, tool, worst case

Management is the art of getting things done through other people. To be a good manager, you need to be capable of responding to a wide range of issues with the right mix of people and technical skills in time enough to get things right.

Getting it right means that you've successfully balanced your available resources with the work that must be done, in the time that it must be done, while satisfying the goals of the organization.

Then, there are those times where management fails. Somewhere, somehow, something didn't happen that needed to happen and it's not because of something that could not be foreseen or that would be impossible to accomplish with your available resources. You knew about it, you could have taken steps to deal with it, and you didn't.

How you deal with this situation will not just make yor break you as a boss. How good a person you are will be tested too.

Your initial impulse may be to cover your mistake up and act like nothing's happened and hope that nothing comes of it. That is, obviously, WRONG. It's already too late, so don't even bother going down that road.

Your next impulse will be to do more management. A lot more. You'll redirect your people to directly overcome the immediate crisis. You'll enlist other managers and their people to help right the results of your oversight. You'll have meetings, make plans and contigency plans. You'll throw every resource you have into the effort, not just calling more people onto the task but also working long hours and spending whatever it takes to erase your mistake.

You've panicked. Clear and simple. And you've just done more damage than you likely did in your original oversight.

Here's what you've done by your act of management: You've disrupted your people and quite possible the people of other groups by redirecting them away from their regular tasks to cope with your emergency. Away from their regular tasks that are required to keep the business running smoothly. The tasks that other people and your customers are relying upon them to do.

This means that at some point, they will need to devote additional effort, beyond the usual level needed, just to recover to where they would be if you hadn't intervened. Many of them will be profoundly annoyed by this, but not because of having to do the work.

Instead, their irritation will be directed at you, because they know you could have acted proactively to address the situation that led to your management by panic. They've been there all along, they've seen things develop into the current crisis and now they resent the disruption to their work enviornment and their lives just to cover for your oversight or lack of action.

It's too much to ask and you shouldn't have. Many of your people will begin pursuing a new work environment, when they're really just looking to replace you. Other managers won't be inclined to go out of their way to support your career. Literally, doing nothing would have been better than doing what you've done.

If only you had considered it. If only you had offered to take full responsibility for the mistake by presenting "nothing" as one of options to consider in developing your elaborate recovery plans. If only you had presented that choice as an option for your staff and other members of your organization. That's where their hard effort could be won over to the task and and where truly earning their respect lay.

But, you had to "manage" your way through it. Because doing something is better than doing nothing. Because nothing else would make you the center of all the action and the hero in the story.

Your ego may have driven you to pursue the course you did. Funny that in the end, it really was all about you.

We've been peering into our crystal ball here at Political Calculations - the one that only looks at the past to tell us the future - to tell us where the U.S. Gross Domestic Product will be. When we want to forecast GDP, we turn to our "Climbing Limo" tool to create our crystal ball predictions. And what we've found in the future of the next three quarters is presenting more questions than we have answers.

We've been peering into our crystal ball here at Political Calculations - the one that only looks at the past to tell us the future - to tell us where the U.S. Gross Domestic Product will be. When we want to forecast GDP, we turn to our "Climbing Limo" tool to create our crystal ball predictions. And what we've found in the future of the next three quarters is presenting more questions than we have answers.

What kind of questions, you ask? Well, for starters, how about these:

- How much will the combined impact of Hurricane Katrina and Hurricane Rita have on the upcoming release the latest GDP data this week?

- Is the stock market climbing significantly now in reaction to surging economic growth three to six months from now?

We present the following table, which we generated using historical data and the forecasts viewed through our crystal ball to underscore why we're asking these questions. We've highlighted the data for the economic quarter that will be released later this week:

| Historical and Forecast Quarterly U.S. Real GDP | ||||

|---|---|---|---|---|

| Year-Quarter | GDP (Real, $billions) | Smoothed Growth Rate (2 Quarters) | BEA Growth Rate (1 Quarter) | Comment |

| 2007-Q1 | 11733.0 | 5.72% | 3.76% | Forecast Using 2005 Q4 thru 2006 Q2 GDP data. |

| 2006-Q4 | 11625.2 | 4.21% | 7.71% | Forecast Using 2005 Q3 thru 2006 Q1 GDP data. |

| 2006-Q3 | 11411.3 | 1.68% | 0.82% | Forecast Using 2005 Q2 thru 2005 Q4 GDP data. |

| 2006-Q2 | 11388.1 | 4.06% | 2.56% | Historical data. |

| 2006-Q1 | 11316.4 | 3.65% | 5.58% | Historical data. |

| 2005-Q4 | 11163.8 | 2.97% | 1.76% | Historical data. |

| 2005-Q3 | 11115.1 | N/C | 4.18% | Historical data. |

| 2005-Q2 | 11001.8 | N/C | N/C | Historical data. |

Analyzing the Results

In looking at this backward-looking data, we observed that the lousy real-GDP number we expect this upcoming Thursday was set by the impact of the two major hurricanes that knocked out the U.S.' Gulf Coast's economic production back in the third and fourth quarter of 2005! Why might this be the case, nearly a year after the hurricanes?!

Our best thinking is that a major economic shock, like the effect of a hurricane, shifts economic activity away from when it happens into the future. Where an event is largely forecastable, like a hurricane, this generally means that short term economic activity is shifted - you see a dip for the month of the hurricane that's fully recovered in the following months. Intermediate term economic activity, which is driven primarily by business contracts between six and eighteen months of duration, is largely unaffected, while long term economic activity is nearly entirely unaffected.

What separates the effects of Hurricane Katrina and Hurricane Rita from regular, garden-variety hurricanes is that they caused enough damage, and worse, unpredictibility, to enter the economic calculations of millions of people and thousands of businesses that the effect of these hurricanes is affecting intermediate term economic activity. People and businesses shifted when they started their intermediate term contracts enough, until the full hurricane season of 2005 had passed - and even until when the hurricane season of 2006 would pass, to avoid this risk. We hypothesize that's why our tool may well forecast why this week's GDP data will come in far below the previous quarter's level.

That also leads us to the GDP forecasts for the quarters following this quarter: our tool foretells of some really impressive growth levels! In looking at this data, which will come out three to six months from this week, we can't help but remember the old investor's axiom that the stock market "looks ahead" six months. We wonder if the market isn't anticipating the same growth that our tool seems to indicate is coming.

Hey, if all these predictions pan out, maybe we'll open up a fortune-telling shop!

Welcome to this special Friday Saturday, October 21, 2006 edition of On the Moneyed Midways, the one place on the web where you can find the best posts from the blogosphere's major business and money-related blog carnivals! Every week, we award one post, chosen from our short list of top posts, with the title of being The Best Post of the Week, Anywhere!(TM)

This week, we had more blog carnivals to consider than usual - it would seem that the fracturation (fracturing + saturation) of blog carnivals is continuing, as we're drawing upon more niche carnivals to compile OMM. We'll also note that a negative effect of this trend is that bloggers submitting posts to blog carnivals can expect much less site traffic than in the past. We've done an experiment over the last two weeks with the venerable Carnival of the Capitalists and have found that the volume of traffic originating from the carnival is far below where it was when we stopped regularly contributing to all carnivals just six months ago, despite achieving favorable placement within the carnival.

Instead, we're finding that a stronger and growing source of our traffic is coming from the web's search engines, which have improved greatly in their ability to find information in blogs. Our guess is that will be the future and that blog carnivals will go the way of the first, and recently deceased, Carnival of the Vanities.

We also anticipate that ubercarnivals like On the Moneyed Midways will replace the regular blog carnivals, just to serve the general interest reading purposes of blog surfers everywhere. Speaking of which, scroll down for the best posts of the week that was....

| On the Moneyed Midways for October 21, 2006 | |||

|---|---|---|---|

| Carnival | Post | Blog | Comments |

| Carnival of Business | User Driven Innovation | Innovation Zen | Daniel Scocco looks at how businesses can tap their customers to develop new products. |

| Carnival of Career Intensity | Looking Busy | Botulus | How important is it to you that you be busy all the time at work? Goss shows how working smarter, not harder is really what's important. |

| Carnival of Debt Reduction | Hey Tricia... It's Your Pal, Your Credit Card | Blogging Away Debt | Tricia received an unusual letter from her credit card, wanting to go do something together. Unfortunately, it turns out she's just not that into you, Plastic! |

| Carnival of Fraud | Fraud, Burnout and Getting What We Deserve | Non-Profit Consultant | Can devoting a little time each day to the "selfish" needs of non-profit workers help prevent them from the temptation of dipping into their organization's tills when they get burned out? Ken Goldstein wonders if the growing problem of fraud in non-profits might not be solved that way. |

| Carnival of Investing | Availability of Exotic Beta | Abnormal Returns | Exchange Traded Funds (ETFs) are revolutionizing the investment options available to common investors. Abnormal Returns reveals how the kinds of investments previously only available to the very well-heeled are now trickling down to the masses. |

| Carnival of Passive Income | Borrowers and Savers: Get Great Interest Rates | My Wealth Builder | Super Saver looks at how Prosper.com's wrinkle on the microloan concept (which just netted economist Mohammad Yunus the Nobel Peace Prize) to both investors and borrowers. |

| Carnival of Personal Finance | Home Equity or Business Loan? | Gina's Tax Blog | Gina Gwozdz talks through why taking out a home equity loan, but not treating the loan like home equity debt on your taxes, makes better sense. |

| Carnival of Real Estate | Broker Commissions: The Law of Thirds, Getting a Commission | Matrix | Jonathan Miller finds that the residential real estate brokerage business has not just a public relations problem, but also a major structural problem. |

| Carnival of the Capitalists | 10 Reasons Why Organizations Are Not Able to Retain Employees | Gautam Ghosh on Management | Well worth reading if you're an employee, and mandatory reading if you're a manager. |

| Economics and Social Policy | Has Wal-Mart Single Handedly Affected the U.S. Economy? How? | Debt Free | Steve Faber looks at what's wrong and what's right with the U.S.' retailing behemoth. |

| Festival of Frugality | Don't Be Afraid to Ask for a Discount | Five Cent Nickel | |

| Festival of Stocks | Why Study the "Fundamentals"? | ValueBlogger | The ValueBlogger shows not just why fundamental analysis should play a large role in your selecting stocks for your investment portfolio, but also why you shouldn't rely on "professionals" to do it! The Best Post of the Week, Anywhere! |

| Investing Carnival | Now What Are the Bad Boys of Hedge Funds Up To? | My Simple Trading System | Praveen uncovers how hedge funds are shaking down companies that are running late in filing their financial statements. |

| Personal Growth Carnival | Many Divisions of Money | Live Your Inspiration | Jane Chin finds that money is not just physical currency. It also has mental, emotional and spiritual dimensions! |

| Wealth Building Ideas | Divide and Rule: Make Compound Interest Work for You | WOW | Alexander Becker has a radical idea: divide and subdivide your money into smaller and smaller amounts, and put them to work for multiple tasks instead of just one big one. In doing so, you'll achieve greater returns than if you had left the original money undivided! |

Previous Editions

- On the Moneyed Midways – October 21, 2006

- On the Moneyed Midways – October 13, 2006

- On the Moneyed Midways – October 6, 2006

- On the Moneyed Midways – September 30, 2006

- On the Moneyed Midways – September 23, 2006

- On the Moneyed Midways – September 15, 2006

- On the Moneyed Midways – September 8, 2006

- On the Moneyed Midways – September 1, 2006

- On the Moneyed Midways – August 25, 2006

- On the Moneyed Midways – August 19, 2006

- On the Moneyed Midways – August 11, 2006

- On the Moneyed Midways – August 4, 2006

- On the Moneyed Midways – July 29, 2006

- On the Moneyed Midways – July 21, 2006

- On the Moneyed Midways – July 14, 2006

- On the Moneyed Midways – July 7, 2006

- On the Moneyed Midways – June 30, 2006

- On the Moneyed Midways – June 23, 2006

- On the Moneyed Midways – June 16, 2006

- On the Moneyed Midways – June 9, 2006

- On the Moneyed Midways – June 2, 2006

- On the Moneyed Midways – May 26, 2006

- On the Moneyed Midways – May 19, 2006

- On the Moneyed Midways – May 12, 2006

- On the Moneyed Midways – May 5, 2006

- On the Moneyed Midways – April 28, 2006

- On the Moneyed Midways – April 21, 2006

- On the Moneyed Midways – April 14, 2006

- On the Moneyed Midways – April 7, 2006

- On the Moneyed Midways – March 31, 2006

- On the Moneyed Midways – March 24, 2006

- On the Moneyed Midways – March 31, 2006

- On the Moneyed Midways – St. Patrick's Day 2006 Edition

- On the Moneyed Midways – March 10, 2006

- On the Moneyed Midways - The inaugural edition from March 3, 2006!

Econlog's Bryan Caplan has written about the economics of the movie theater and recently has proposed an idea that, by all accounts, should be seriously considered by theater owners: theaters should offer their customers tickets at different prices at different times on different days.

Econlog's Bryan Caplan has written about the economics of the movie theater and recently has proposed an idea that, by all accounts, should be seriously considered by theater owners: theaters should offer their customers tickets at different prices at different times on different days.

Right now, theaters already do two parts of what the movie-going economist has proposed: they already offer tickets at different prices at different times (for example, the tickets for matinee showings during the daytime are priced considerably lower than evening showings.) Caplan's proposed innovation then is to differentiate price by days of the week, say by charging the highest prices for the peak movie viewing period of weekend evenings (Friday, Saturday and Sunday), lower prices for weekend matinees and the lowest prices on non-weekend days (Monday through Thursday.)

By using price as a mechanism for distributing the audience for movies away from the peak movie viewing time at the theaters, weekend evenings, to other times during the day and the week where empty seats in the theater are in greater supply, Caplan argues that movie-goers like himself would gain greater happiness (as measured by less grumbling and less time spent in line to buy tickets).

Not mentioned by Caplan though are the potential benefits for theater owners. They would gain by being able to maintain a more consistent level of staffing and ideally, greater revenues as the higher-priced weekend evening showings would continue to be the most popular, but with the additional benefit of being able to make more money than they do now on weekdays by drawing a higher volume of budget-conscious movie fans.

In theory, this system would work great as people would respond to the pricing incentives to shift when they view movies away from the highest priced time on weekend nights to lower-priced times.

The problem with this proposed pricing system is that it solves a problem that doesn't really exist to any great extent. Can you name the last time you couldn't see a movie at the theater on a weekend evening because it was sold out? Sure, you might have had to wait in line longer than you might have liked and not have gotten into the 7:00 showing of Jackass Number Two, but what about the 8:45 showing at the same theater? Or, in the case of the modern movie multi-megaplex, where you might get to choose from 7:30, 8:00 or 8:30 showings too? How put out could today's movie consumer possibly be?

The truth is that if Hollywood and the movie theater owners really want to increase the size of their audiences, they need to deliver greater value to the movie consumer for their money that what they're doing today.

The truth is that if Hollywood and the movie theater owners really want to increase the size of their audiences, they need to deliver greater value to the movie consumer for their money that what they're doing today.

Leaving aside whether Hollywood wants to produce, or is even able to produce, movies for the theater that more people today want to see, let's consider two slightly different pricing options that movie theater owners might want to consider; options designed to provide substantially greater to potential movie consumers.

First, in addition to charging movie audience members by the movie, why not offer ticket buyers the choice of a day pass to the theater instead? Here, the movie-goer would be free to roam from show-to-show, either watching a movie they like over and over or bailing out of a movie they don't like for one that they might find more entertaining. With the only restriction being whether or not seats are available in a given theater, the option of being able to go to any and every movie within the multiplex clearly delivers more value than today's "a la carte" ticket system ever could.

Better still, from the theater owners' standpoint, a day pass delivers benefits in that the movie goers don't leave the theater for other pursuits! The longer they're in the theater, the more likely we suspect that they'll be visiting the all-important, high profit margin concession stand.

Better still, from the theater owners' standpoint, a day pass delivers benefits in that the movie goers don't leave the theater for other pursuits! The longer they're in the theater, the more likely we suspect that they'll be visiting the all-important, high profit margin concession stand.

The next part of our movie ticket pricing proposal goes straight to the core of the movie-going experience: watching flickering lights projected on a wall in a dark room with a group of people. Here, we suggest that instead of offering discounts for age, the theater owners would do much better by offering discounted tickets to groups, beginning with the second person. For example, the first ticket could be for $8.00, the second for $6.50, the third for $5.00 and on down to some minimum price.

For groups of people, like families or other kinds of groups, this pricing option delivers real value as each member of the group would have much lower out-of-pocket costs than they could if they went to the show individually, thereby encouraging them to see more movies together. The theater owners would benefit from this kind of pricing arrangement by getting what they really want: a large volume of consumers who will very likely be visiting the concession stand.

And when you consider that this pricing option much better reflects the theater owner's actual business, where the marginal revenue gained from showing a movie to each individual additional customer far outweighs the marginal cost of doing so, it's what they should be doing anyway. So, the question to the theater owners is: why not?

Worth Reading Elsewhere

Tyler Cowen of Marginal Revolution has also wondered why movie theaters don't have more pricing options.

Labels: business

Once again, the Bureau of Labor Statistics has reported the Consumer Price Index for Urban Consumers (CPI-U) for September 2006, which has come in at a level of 202.9 (2.1% higher than one year ago).

For us here at Political Calculations, the release of the inflation number means that we can put our tool for predicting the I-bond's future rate of return to work! Now that we know the inflation values to plug in (the September 2006 value above and the March 2006 value of 199.8, the only question remaining is what will the U.S. Treasury set as the core rate of the I-bond.

For the fixed rate component of the I-bond, we'll guess a low-end and a high-end value. Since the core rate of return for the May 2006 I-bond is 1.4%, we'll enter 1.2% for the low end and 1.6% for the high end value. (The beauty of our tool is that if you don't like these values, you're welcome to change them!)

And that's all you need to predict where the I-bond will be set this November!

Using our default data, we would anticipate the I-bond being set at 4.52%, with the low-end of our prediction range set at 4.32% and the high end at 4.73%, give or take a few hundredths of a percent. We'll see where the Treasury Department sets the rate in November!

Where'd we come up with the name for this portion of our user's guide? Well, think about it. Where do *you* put everything that doesn't have a nice, neat defined space?

That's not to say that you'll find junk here! Just like in any junk drawer, there can be some real gems hidden among all the stuff that's crammed in here. It might be a Compact Fluorescent light bulb. Or a can of diet soda. Maybe it the key to converting that idea of yours into wealth you never imagined?!

No matter what, you're already here, so you might as well rummage around....

| Miscellaneous Stuff |

|---|

| Subcategory | Title | Description |

|---|---|---|

| Diet | How Many Cans of Diet Soda Can You Drink Safely? | You know you want to find out the answer, and only Political Calculations has built the tool to do the math! |

| Safety | Truth and the Time to React | How much time do you have to stop your car after soldiers at a checkpoint signal you to stop your car? Our tool answers this question in debunking an anti-American journalist's dubious claims. |

| Journalism | Running Numbers for Reporters | Journalists are among the least knowledgeable people on the planet, especially when it comes to reporting numbers. Our tool is designed to help journalists get a better grip on reality. |

| Ideas | How Much Is That Idea Really Worth? | Do you have a great idea? How good is your execution? Our tool puts the two together to show you how good your idea really is! |

| Wealth | Are You wealthy? | A quick, back of the envelope calculation to help you find out if you're closer to the Rockefeller's or their Rottweilers! |

| Home Economics | Are Compact Fluorescents a Bright Idea? | CF lamps cost more, but can save energy costs. Our tool does the math to help you decide if they make sense for you! |

| Blogging | MSM vs Blogger Influence | How do you compare the influence of a journalist against that of a blogger? How about by the number of their actual readers? Our tool puts it all together…. |

Return to the User's Guide to Political Calculations

Is there anything ickier than dealing with the government and its bureaucrats? When, for instance, was the last time you had a pleasant experience in a government office, that had anything to do with why you were really there?

We couldn't answer that last question either! That's why, as part of our public service policy, mandated by Section 714.323.210 Paragraphs b, d and k, of the Uniform Blog Commerce Code, we've provided the following tools to help you better understand the effects of current and proposed government policies.

Don't get us started about the tax code....

| Public Policy |

|---|

| Subcategory | Title | Description |

|---|---|---|

| Spending | Projecting the Growth of Pork | How bad is pork barrel spending in Washington D.C.? Our tool shows pork's exponential growth and projects it into the future! |

| Social Security | Your Investment Return from Social Security | What if the taxes you paid into Social Security were an investment. Our tool estimates your rate of return. |

| Social Security | Social Security or Personal Retirement Accounts? | Our first tool that explored whether you'd end up ahead or behind if Social Security was replaced with Personal Retirement Accounts. |

| Social Security | The President's Plan for Social Security and You | Our tool was the first to accurately model the President's proposed plan for reforming Social Security. |

| Social Security | Slashing Social Security Benefits | The Democrats opposed to Social Security reform in 2005 did have an alternative: doing nothing. Our tool shows how much benefits paid in the future would be slashed under that risky scheme. |

| Taxes | Taxing Matters | Public policy is funded by taxes - our index has all our tax-related tools! |

| Demographics | Estimating the U.S. Population | How many people are there in the U.S.? Our tool estimates just how many Americans there are! |

| National Debt | National Debt | The U.S. government borrows money. A lot of money. Our analysis spans more than 100 years of the national debt. |

| Economics | DIY Economics! | A lot of public policy falls under the realm of economics. Our tools make it possible for you to do your own analysis! |

Return to the User's Guide to Political Calculations....

Air America Radio filed for bankruptcy today, according to breaking news reports (HT: InstaPundit). The go-to source for the inside story continues to be Brian Mulroney's Radio Equalizer (click the last link for new posts.)

Air America Radio filed for bankruptcy today, according to breaking news reports (HT: InstaPundit). The go-to source for the inside story continues to be Brian Mulroney's Radio Equalizer (click the last link for new posts.)

In the meantime, this move doesn't come as much of a surprise - we've been anticipating it for quite some time here at Political Calculations. Here's a brief history of our analysis of AAR's business situation:

- The Future of Air America

We kicked off our series of posts analyzing Air America Radio viability as a business with this post. We really didn't think it would go much further than this!

- Air America, Again

We found that AAR doesn't just have competition from the right - it has it on the left as well....

- The Financing of Air America Radio

A throw-away post that let us fill space with some information on where AAR got its financing that we had come across in our previous analysis.

- Time to Harvest or Divest

As AAR appeared to be running into significant turbulence, we updated our original strategic business analysis, finding that what AAR's management needed to do was to find "white knight" financing or to start making moves to significantly cut its costs.

- A Top Ten Countdown

We couldn't resist applying a list a bankruptcy lawyer came up with for a failing company to AAR's known problems - lucky thing AAR has benefitted from the generosity of multi-millionaires with deep pockets.

- Profiles in Semi-Obscurity

Another space-filler post where we just unloaded background information about various members of AAR's Board of Directors that we had come across in previous analysis.

- Air America's Ratings in the Top 100 Radio Markets

Our look at AAR's ratings through Arbitron's Winter 2006 period.

- A Bigger Footprint

An intrepid e-mailer let us know that AAR's flagship affiliate WLIB had a bigger footprint than just the New York City market - plus, we find that roughly half of AAR's audience is in just five cities.

- Profiling a Handful of AAR's Local Affiliates

Once again, we unload information we collected in other analysis. This time, we estimate just how many local AAR affiliates there are by determining where they're not.

- Air America's Spring 2006 Ratings

Here, we found that ratings weren't growing, at all, for the troubled radio network.

- The Clock Ticks Toward Bankruptcy

A premature report that Air America Radio's parent company would be declaring bankruptcy prompted this post, which still held up after the liberal blog that reported it retracted their story.

Welcome to this special Friday, October 13, 2006 edition of On the Moneyed Midways, the web's weekly round-up of the top posts from the blogosphere's major business and money-related blog carnivals! Each week, we award one post with the title of being The Best Post of the Week, Anywhere!(TM), so if you read nothing else this week, you should at least read our top pick!

Actually, now that we think about it, The Best Post of the Week, Anywhere!(TM) is really just what we think is the best of the best, so you should read them all! Just scroll down for the best posts of the week that was....

| On the Moneyed Midways for October 13, 2006 | |||

|---|---|---|---|

| Carnival | Post | Blog | Comments |

| Carnival of Career Intensity | How to Get More Done by Doing Less | Jack Yoest | Jack Yoest says a "Day of Rest" does more to get things done that continuously working. Is he right? |

| Carnival of Debt Reduction | Credit Card Balance Transfers: The Art of Moving Debt | Money Under 30 | David provides advice and a how-to for consolidating credit card debt while taking advantage of low introductory rates. |

| Carnival of Home Business | 4 Things to Consider About Your Home-Based Business Structure | Success from the Nest | Should you set up your home-based business as an LLC? An S corp? Or maybe as a sole proprietorship? The NestGuy outlines the basics of what you need to know. |

| Carnival of Personal Finance | Foolarch's Laws of Real Estate [de]Valuation | folleyball | Is your neighborhood cluttered with liquor stores, payday loan outfits and auto audio establishments? Foolarch shows how each of these businesses contribute to low property values. |

| Carnival of Real Estate | "The Proof Is In the Puddin'" Range Pricing Part 1,275! | active rain | Bryant Tutas sheds light on how emotions can influence purchasing decisions for big ticket items, and how a sharp real estate agent could cash in! |

| Carnival of the Capitalists | Why Smart Companies Do Dumb Things | Signal Without Noise | Guy Kawasaki points out all the factors that go into bad business decisions, then offers advice on how to avoid the traps. |

| Cavalcade of Risk | Managing Business Risk | The Home of Sourcing Innovation | Would your business survive a major disruption? Michael Lamoureaux demonstrates how Business Continuity Planning can reduce risk in the face of natural or man-made disaster in The Best Post of the Week, Anywhere! |

| Festival of Stocks | Deficient Market Hypothesis | Margin of Safety | Mr. Market advances his revolutionary theory of the Deficient Market Hypothesis - suggesting how a contrarian approach to the underlying theories behind the Efficient Market Hypothesis might be used to successfully grow one's investments. |

| Investing Carnival | Options 101 | Million Dollar Count Down | Do you know what calls or puts are - or how they work? The Million Dollar Count Down provides a great introduction to these trade vehicles. |

| Personal Development Carnival | How to Increase Your Value by Tracking Your Time | Unleash Your Potential | My Bubble Life reveals how a humble activity log can help you eliminate wasteful activity in favor of more valuable applications of your time. |

| Personal Growth Carnival | Swallow That Frog! | MattHutter.com | We admit we selected this post purely on the title alone! Then again, Matt Hutter has a really good point…. |

| Wealth Building Ideas | Hit 'Em Where They Ain't | Ask Uncle Bill | Uncle Bill provides invaluable career advice on how to get ahead by standing out in a crowd. |

Previous Editions

- On the Moneyed Midways – October 13, 2006

- On the Moneyed Midways – October 6, 2006

- On the Moneyed Midways – September 30, 2006

- On the Moneyed Midways – September 23, 2006

- On the Moneyed Midways – September 15, 2006

- On the Moneyed Midways – September 8, 2006

- On the Moneyed Midways – September 1, 2006

- On the Moneyed Midways – August 25, 2006

- On the Moneyed Midways – August 19, 2006

- On the Moneyed Midways – August 11, 2006

- On the Moneyed Midways – August 4, 2006

- On the Moneyed Midways – July 29, 2006

- On the Moneyed Midways – July 21, 2006

- On the Moneyed Midways – July 14, 2006

- On the Moneyed Midways – July 7, 2006

- On the Moneyed Midways – June 30, 2006

- On the Moneyed Midways – June 23, 2006

- On the Moneyed Midways – June 16, 2006

- On the Moneyed Midways – June 9, 2006

- On the Moneyed Midways – June 2, 2006

- On the Moneyed Midways – May 26, 2006

- On the Moneyed Midways – May 19, 2006

- On the Moneyed Midways – May 12, 2006

- On the Moneyed Midways – May 5, 2006

- On the Moneyed Midways – April 28, 2006

- On the Moneyed Midways – April 21, 2006

- On the Moneyed Midways – April 14, 2006

- On the Moneyed Midways – April 7, 2006

- On the Moneyed Midways – March 31, 2006

- On the Moneyed Midways – March 24, 2006

- On the Moneyed Midways – March 31, 2006

- On the Moneyed Midways – St. Patrick's Day 2006 Edition

- On the Moneyed Midways – March 10, 2006

- On the Moneyed Midways - The inaugural edition from March 3, 2006!

Just for fun, we decided to take a dark, steamy look at the murky underside of the U.S. national debt. Well, okay, it wasn't fun, but we learned something, so we're passing on our cumulative knowledge on to you! Not much in the way of tools here, but we did the math all the same....

Why, you ask? Well, the name of this blog is "Political Calculations", after all....

| National Debt |

|---|

| Subcategory | Title | Description |

|---|---|---|

| History | Picturing the National Debt | We look at the history of the national debt, from 1900 onward! |

| History | Looking at the U.S. National Debt on a Personal Level | Here, we've taken the national debt and broken it down into individual portions! |

| History | Picturing the U.S. National Debt on a Real Personal Level | Well, what about inflation you ask? We show each individual American's share of the U.S. national debt since 1900 after inflation is taken into account! |

| History | Picturing the U.S. National Debt to Income Ratio | Isn't there a better way to measure the U.S.' debt burden? Well, yes - we can measure it against the U.S.' national income! |

| Economics | Why Isn't the U.S.' National Debt per Capita Higher? | In answering this question, we uncovered an even better way to measure the national debt burden for individual Americans. |

| Public Policy | Automatically Indexing the U.S. Debt Ceiling | We take the index we created in a previous post and show how it might be used to set the U.S.' national debt limit, while keeping the national debt managable. |

Return to the User's Guide to Political Calculations

Labels: national debt

How much will you have left in your paycheck after Uncle Sam gets a hold of it? Should you invest in tax-free municipal bonds or in taxable corporate bonds? How much is the government siphoning off from your fuel tank?

We've taken on these questions and more with the tools we've built to answer them! Just scroll down for the most current edition of all our tax-related tools!

| Taxing Matters |

|---|

| Subcategory | Title | Description |

|---|---|---|

| Paycheck | Your 2006 Paycheck | What's your paycheck going to look like after the government gets its dirty, stinking ape paws all over it? Our tool has the answer, plus it can show you what your new take home pay will be after a raise! |

| Investing | Marginal Tax Rates and Investment Choices | Should you invest in a tax-free or a taxable investment vehicle? Our tool can help you find the answer! |

| Gas | How Much Do You Pay in Gas Taxes? | Did you know that governments in the U.S. collect more on each gallon of gas sold than the oil companies collect in profits? Our tool estimates how much you pay each year in gas taxes! |

| Investing | Income Taxes and Investing in 2006 | We update our original look at the importance of marginal tax rates in making investment decisions for 2006! |

| Tax Breaks | Exploiting the Child Interest Income Credit | If you have kids, you can reduce your tax bill while building up the resources they'll need later in life - our tool runs the numbers for you. |

| What If?... | What If the Death Tax Were an Income Tax? | Death and Taxes are the two constants of life. Perversely, there are also death taxes, as if the government couldn't drain enough from you while you were alive. Our tool shows how much the death tax actually is by converting it into an equivalent income tax charged during your life. |

| What If?... | Consumption vs Income Taxes | Should we do away with the income tax in favor of a national consumption tax? Picking up on Greg Mankiw's math, we built a tool that shows why the consumption tax is economically preferable. |

Return to the User's Guide to Political Calculations

Labels: taxes

Welcome to the blogosphere's toolchest! Here, unlike other blogs dedicated to analyzing current events, we create easy-to-use, simple tools to do the math related to them so you can get in on the action too! If you would like to learn more about these tools, or if you would like to contribute ideas to develop for this blog, please e-mail us at:

ironman at politicalcalculations

Thanks in advance!

Closing values for previous trading day.

This site is primarily powered by:

CSS Validation

RSS Site Feed

JavaScript

The tools on this site are built using JavaScript. If you would like to learn more, one of the best free resources on the web is available at W3Schools.com.

Other Cool Resources

Blog Roll