Halloween means many things to many people. For kids, its the opportunity to dress up and score big in the candy department. For others, its the opportunity to go out and raise a little hell by partying until sunrise.

But unlike other candy consumption-oriented holidays or party-oriented holidays, Halloween combines the two with an environment of fear.

It is, perhaps, the only holiday where the participants are virtually required to approach a stranger's house for the purpose of seeking treats or fun. And that's where the fear starts, because what if that house belongs to that recent transplant from Transylvania whose hospitality is such they invite you in.

And once on the inside, they invite you to "make yourself comfortable and have a seat". You were already a little uncomfortable, but now, your spook-o-meter is about to spike because of their taste in furniture, because, well, the chair to which you've been directed to sit looks something like the following examples.

If a chair is seemingly formed by the impact of a human body having been dropped or thrown from a great height, how comfortable would you be sitting in it? Ezra Tazari's "Free Fall" chair forces you to confront that prospect.

Better yet, how will would you be to sit in Thomas Feichtner's M3 chair? Here's the concept:

Liberated from the demands normally made on a mass-produced item, this design experiments with functionality, structural engineering and material. Both its back and its armrests are mere tangents of the construction, the functions of which are only discovered via actual use. With a seating surface floating within the construction and legs extending far to the sides, the M3 is most assuredly not a chair that saves space—it is much rather one which creates a space [of exactly one cubic meter; hence the name of the piece]

Yes, being asked to sit in a Thomas Feichtner M3 chair is the same as being asked to fit yourself inside a box. Scared yet?

What's more inviting than being asked to sit in a chair that's also a storage unit for closet hanger? Which we note says a lot about what the chair's owner thinks about their guest's seating requirements. We suppose that being asked to hang around in a closet might be, but for those fearless souls seeking a new sitting experience, the Coat Check chair might fit the bill.

What if your host is really a cyborg from the future who has been sent back in time to terminate you? Perhaps then you should think twice about sitting in Philipp Aduatz' "melt" chair, which looks to be made from liquid metal. Just watch out for when the chairs arms form into, well, arms....

What if the chair in which you've been asked to sit resembles a creature more than a chair - making it more of a furniture organism, if you will? Eyal Hirsh's "Pet Stool" adds a plush appendage to the more traditional three-legged stool....

Say, did you ever wonder what happened to your old bike? The one that disappeared from your yard one day when you were a kid? Bruno Urh's "Chair for Janez Suhadolc" re-configures it for stationary seating purposes, but still keeps your old bike's "chafing" seat at the center of the sitting experience.

And speaking of bike seats:

Jeremy Petrus collaborated with Italian bike saddle manufacturer Selle Royal to create the "Mishmash" chair presented above.

Hey, remember that chair made from coat hangers? We bet you'd really rather sit on that one than this concept, envisioned by Italian design firm Stylemylife, which takes the same concept down a different path:

Let's call that one a throne of bones. And don't you just love the decor! You'll be very comfortable chatting with your neighbor there....

Meanwhile, you might quite literally be sucked into a separate dimension if you dare sit in Artem Zigert's "Mechanical Perspective" chair:

Finally, via Barry Ritholtz, a ginormous infographic that describes how sitting is killing you!

Maybe you should think twice before taking that offered seat....

Update 19 February 2013: The original source for the infographic above is Medical Billing and Coding, who entered it into the public domain along with the exact code we've incorporated in this post back on 9 May 2011 - our apologies for missing this citation in our original post!

Why Chairs and Halloween?

What can we say? We have some odd holiday traditions here at Political Calculations. For us, nothing says Halloween or a trip to the corporate suites of Goldman Sachs quite like a super scary chair!

Labels: none really

Yesterday's 3.4% gain in the S&P 500 marked the biggest gain in a month of gains. Since 3 October 2011, when the S&P closed just below 1100 at 1099.23, the S&P 500 has risen 16.9%, or 185.36 points, through the end of 27 October 2011 to close at 1284.59.

As you can see in the chart above, stock prices have pretty consistently trended upward during the month. And although the European debt deal is being credited for the one day gain, that doesn't explain the rise in stock prices over the past month, given the uncertainty surrounding the progress in working toward the deal announced on 27 October 2011.

And if we look at the change in the rates of growth of both stock prices and the S&P 500's underlying dividends per share, we see that average stock prices during October 2011 would appear to be below the level that the change in dividends projected for the third quarter of 2012 would put them (remember, investors always look forward in time!):

But that's the average of stock prices for the month-to-date for October 2011. What if we just considered where stock prices closed on 27 October 2011?

Here, we see that stock prices have indeed caught up, and have even slightly passed where the change in the growth rate for dividends per share for the third quarter of 2012 would put them!

And that's after stock prices for September 2011 were almost exactly where the projected future for the second quarter of 2012 would put them.

What has happened during the month of October 2011 is that investors setting today's stock prices have shifted their focus forward in time from the second quarter of 2012 to the third quarter of 2012. The market has risen in response to that shift in forward-looking focus.

We would then describe the Euro deal as little more than a noise event. Since stock prices have overshot where dividends would place them, we would anticipate that the market will flatten out or fall back a bit in the immediate future as the effect of this news-driven event fades with time.

On the whole however, we can expect November 2011's stock prices to be higher on average than they were in October 2011, and if not for the overshooting effect of the European debt deal noise event, we would expect slowly rising stock prices for the month.

Labels: chaos, SP 500, stock market

According to a CBO report, the top 1% of income earners saw a 275% increase in their inflation-adjusted, after-tax income between 1979 and 2007.

By our quick math, that 275% increase works out to be an annualized rate of change of 4.83% over the CBO's oddly cherry-picked 28 year period from 1979 through 2007 (click the links for the years to understand why).

By contrast, our S&P 500 at Your Fingertips tool indicates that if the Top 1% had just invested their after-tax income in an S&P 500 index fund in January 1979 and then let it ride to December 2007 as the stock market peaked, fully reinvesting dividends all that time, they would have seen an inflation-adjusted, tax-free rate of return of 8.70%.

And that's without even bothering to work! If taxed at the maximum 1979 capital gains tax rate of 28%, their after-tax income would represent an annualized rate of return of 6.26% annually. Or rather, a 448% increase in their inflation-adjusted, after-tax income!*

So clearly, the Top 1% were total suckers for even bothering to put their money to work at all doing those other things they apparently did during those 28 years that pushed their effective rate of returns down. Like work!

[* Not really, and for the record, the analysis presented in this post is wrong, on purpose, although we suspect that certain people who will be really irritated by this post won't be able to explain why. If it helps, sometimes, we post things just to upset certain people, who like to think they know it all, but who are really short in the mental horsepower department, among others!]

Labels: none really

Why is income inequality rising for U.S. families and households, but not for individual Americans?

Having now shown that there has been absolutely no significant change in the level of inequality among U.S. individual income earners from 1994 through 2010, we thought we'd take a step back and look at the data for U.S. families and for households to examine those trends over time.

The chart below shows what we find for each grouping of Americans according to their Gini Coefficient, where a value of 0 indicates perfect equality (everyone has the same income) and a value of 1 indicates perfect inequality (one person has all the income, while everyone else has none):

In the chart above, we've adjusted the vertical scale to zoom in on the data, which magnifies the amount of any change from one data point to the next.

Starting with the topmost line on the chart, shown in red, which applies to all individual income earners in the United States, we see that this group contains the greatest degree of inequality by income, according to its Gini ratio. Here, there is no meaningful change in the amount of measured income inequality for the personal income distribution for the years from 1994 through 2010 (or if you really want to stretch, there has been a very slight decline in individual income inequality over that time - in our view, it is too slight to be meaningful as it may be the result of natural variation from year to year.)

The next line down, shown in green, applies to all households in the United States. Here we see that compared to U.S. individuals, U.S. households experience less income inequality. However, we see that there has been a slowly rising trend toward greater inequality from 1994 through 2010.

Meanwhile, the next line down, shown in blue, applies to all U.S. families. Here, we see the greatest amount of equality for incomes earned in the United States, and we also see that like the trend for U.S. households, there has been a slowly rising trend toward greater income inequality in the period from 1994 through 2010.

If that sounds familiar, that's because the income inequality data for both families and households has been what has typically been presented in a very biased media as evidence that the "rich are getting richer" over time, especially as these claims are being used by academics and activists to justify an ever-increasing amount of intervention by the government to combat this so-called "problem".

But here's the thing. We have already confirmed that there has been absolutely no meaningful change in the inequality of individual income earners in the years from 1994 through 2010. If income inequality in the U.S. was really driven by economic factors, this is where we would see it, because paychecks (or dividend checks, or checks for capital gains, etc.) are made out to individuals, not to families and not to households.

It would seem then that the real complaint of such people isn't about rising income inequality, but rather, how people choose to group themselves together into their families and households.

With a near rock-steady level of income inequality among individual income earners over time, it is only possible for income inequality to rise among families and households if the most successful income earners group themselves into families and households and if the least successful income earners likewise group themselves together into families and households as well.

Think about it. The reason that the income inequality levels recorded for families and households are lower than those for individuals are because most families and households may have one high income earner, who is balanced out by individuals within the families or households who have low or no incomes.

But, if people with very high income earning potential join together to form families and households, and increasingly do so over time, perhaps because such people might have things in common that make forming themselves into families and households an attractive proposition, then income inequality among families and households will increase.

The same holds true for the opposite end of the income earning spectrum. If people with really low income earning potential join together to form families and households, or perhaps if they choose to split apart, and increasingly do so over time, then the resulting low income family and household will also make income inequality among families and households rise, even though there has been no real change in the amount of actual income inequality among individuals.

Now for the bigger picture. Ivan Kitov has done an extended analysis of the U.S. Census' income data back to 1947. He found the following related to the personal income distribution (PID) for the U.S. since 1960 (emphasis ours):

In fact, the Gini curve associated with the fine PIDs is a constant near 0.51 between 1960 and 2005 despite a significant increase in the GPI/GDP ratio and the portion of people with income during this period (see Figure 1). This is a crucial observation because of the famous discussion on the increasing inequality in the USA as presented by the Gini coefficient for households (US CB, 2000). Obviously, the increasing G for households reflects some changes in their composition, i.e. social processes, but not economic processes as defined by distribution of personal incomes.

In short, it's those social processes, which have driven demographic changes within U.S. households, that are almost exclusively behind the observed increase in family and household income inequality observed in the U.S. since the 1960s.

Surprisingly, many economists are still hypothesizing on what might be the cause of rising income inequality among families and households. From the discussion however, it's pretty clear that just about all of them may not be aware of the Gini coefficient data that applies to the personal, or individual, income distribution data that makes it possible to eliminate the proposed alternatives as serious contenders for explaining what we observe.

We hate to be the ones to tell you guys, but the econophysicists have solved this puzzle....

Labels: income distribution, income inequality

Perhaps the most common measure of income inequality in a nation is the Gini Coefficient (aka the "Gini Ratio"), which ranks the amount of inequality there is in a country on a scale from 0, which represents perfect equality, where everyone would have an equal share of the nation's income, to a value of 1, which represents perfect inequality, where one person would have all the income, but everyone else has none.

So now, thanks to so much media attention being focused on the Occupy Wall Street "movement" (aka "politically-oriented publicity stunt"), where many activists (aka "not-too-bright people") appear to be upset at "the Top 1%" (aka "really high income earners"), who they claim have "gotten too rich" (aka "earned a high income by doing things that satisfy other people's needs"), we thought we'd use the "Gini coefficient" (aka "a well-established mathematically-based method for measuring inequality") to find out how out of whack things have become in the United States over the years.

Or more specifically, the years from 1994 through 2010, for which the U.S. Census has published detailed data related to the incomes earned by Americans based on their annual surveys of the U.S. population. Our chart showing the trend in income inequality for all individuals as measured by the Gini ratio for these years is below:

We were shocked to see the overall trend from 1994 through 2010 take the path it has, because it's so completely contrary to what we keep hearing in the news.

We only ask that someone ask the media for their reaction to this disturbing data!

Data Sources

U.S. Census. Current Population Survey. Annual Demographic Survey, March Supplement. Table PINC-01. Selected Characteristics of Persons 15 Years and Over, By Total Money Income in 1994, Work Experience in 1994 and Sex. September 1995.

U.S. Census. Current Population Survey. Annual Demographic Survey, March Supplement. Table PINC-01. Selected Characteristics of Persons 15 Years and Over, By Total Money Income in 1995, Work Experience in 1995 and Sex. September 1996.

U.S. Census. Current Population Survey. Annual Demographic Survey, March Supplement. Table PINC-01. Selected Characteristics of Persons 15 Years and Over, By Total Money Income in 1996, Work Experience in 1996 and Sex. September 1997.

U.S. Census. Current Population Survey. Annual Demographic Survey, March Supplement. Table PINC-01. Selected Characteristics of Persons 15 Years and Over, By Total Money Income in 1997, Work Experience in 1997 and Sex. September 1998.

U.S. Census. Current Population Survey. Annual Demographic Survey, March Supplement. Table PINC-01. Selected Characteristics of Persons 15 Years and Over, By Total Money Income in 1998, Work Experience in 1998 and Sex. September 1999.

U.S. Census. Current Population Survey. Annual Demographic Survey, March Supplement. Table PINC-01. Selected Characteristics of People 15 Years and Over By Total Money Income in 1999, Work Experience in 1999, Race, Hispanic Origin, and Sex. September 2000.

U.S. Census. Current Population Survey. Annual Demographic Survey, March Supplement. Table PINC-01. Selected Characteristics of People 15 Years and Over By Total Money Income in 2000, Work Experience in 2000, Race, Hispanic Origin, and Sex. September 2001.

U.S. Census. Current Population Survey. Annual Demographic Survey, March Supplement. Table PINC-01. Selected Characteristics of People 15 Years and Over By Total Money Income in 2001, Work Experience in 2001, Race, Hispanic Origin, and Sex. September 2002.

U.S. Census. Current Population Survey. Annual Demographic Survey, March Supplement. Table PINC-01. Selected Characteristics of People 15 Years and Over By Total Money Income in 2002, Work Experience in 2002, Race, Hispanic Origin, and Sex. September 2003.

U.S. Census. Current Population Survey. Annual Demographic Survey, March Supplement. Table PINC-01. Selected Characteristics of People 15 Years and Over By Total Money Income in 2003, Work Experience in 2003, Race, Hispanic Origin, and Sex. September 2004.

U.S. Census. Current Population Survey. Annual Demographic Survey, March Supplement. Table PINC-01. Selected Characteristics of People 15 Years and Over By Total Money Income in 2004, Work Experience in 2004, Race, Hispanic Origin, and Sex. September 2005.

U.S. Census. Current Population Survey. Annual Demographic Survey, March Supplement. Table PINC-01. Selected Characteristics of People 15 Years and Over By Total Money Income in 2005, Work Experience in 2005, Race, Hispanic Origin, and Sex. September 2006.

U.S. Census. Current Population Survey. Annual Social and Economic (ASEC) Supplement. Table PINC-01. Selected Characteristics of People 15 Years and Over By Total Money Income in 2006, Work Experience in 2006, Race, Hispanic Origin, and Sex. September 2007.

U.S. Census. Current Population Survey. Annual Social and Economic (ASEC) Supplement. Table PINC-01. Selected Characteristics of People 15 Years and Over By Total Money Income in 2007, Work Experience in 2007, Race, Hispanic Origin, and Sex. September 2008.

U.S. Census. Current Population Survey. Annual Social and Economic (ASEC) Supplement. Table PINC-01. Selected Characteristics of People 15 Years and Over By Total Money Income in 2008, Work Experience in 2008, Race, Hispanic Origin, and Sex. September 2009.

U.S. Census. Current Population Survey. Annual Social and Economic (ASEC) Supplement. Table PINC-01. Selected Characteristics of People 15 Years and Over By Total Money Income in 2009, Work Experience in 2009, Race, Hispanic Origin, and Sex. September 2010.

U.S. Census. Current Population Survey. Annual Social and Economic (ASEC) Supplement. Table PINC-01. Selected Characteristics of People 15 Years and Over By Total Money Income in 2010, Work Experience in 2010, Race, Hispanic Origin, and Sex. September 2011.

Labels: income distribution, income inequality, satire

Previously, we've shown that the stock market's expected dividends per share are the fundamental driver of today's stock prices. In fact, we even worked out the basic math:

In the equation above "P" refers to the average stock prices for a given month, while "D" refers to the stock market's trailing year dividends per share. "s" refers to how many months ahead we might be looking to see where the stock market's trailing year dividends per share are expected to be at that point in time. "Current" means now (or your period of interest) and "current - 12 months" indicates a value that was recorded 12 months earlier (or 1 month earlier, or 13 months earlier, as whatever the case may be.)

But "m", our amplification factor, is something we've empirically observed. Typically, or at least through much of the current century, we've found its value ranges between 6.0 to 12.0, and we most often select the mid-range value of 9.0 for use in forecasting where stock prices are headed.

But what affects the actual value of this amplification factor? We've previously observed that it can vary substantially, as this single component in our math absorbs what we describe as "noise" in the market, but what if it has its own fundamental component?

We ask that question today because we think we're on to something. The chart below, updated from the version we posted one month ago, shows the game that's afoot (the only changes are that we finalized the data point for September 2011 and added a new data point covering this point in time through October 2011):

Right now, trailing year dividends per share for the S&P 500 are retracing the exact same levels they first recorded in the years from June 2003 through December 2007. But, stock prices aren't at the same level as they were during that period. They are instead about 14-16% below that earlier trajectory.

The last time that happened, was the months of May through September 2010. And what made those months unique is that they fell in the gap between the Federal Reserve's QE 1.0 and QE 2.0 programs, where the Federal Reserve used a strategy of "quantitative easing" to actively fight the prospects for deflationary conditions taking hold in the U.S. economy during the months that these programs ran.

During the five months from May through September 2010, the Federal Reserve had no quantitative easing program in place to combat deflationary conditions from taking hold in the U.S. economy. In the absence of those programs, expectations for deflationary conditions returned to the U.S. economy.

By contrast, the period from June 2003 through December 2007 was characterized by relatively steady inflationary conditions. Coincidentally, about the same level that we briefly recorded in January through May of 2011.

In our math, the only way we can have approximately the same changes in the growth rate of dividends per share and the approximately the same dividends per share without having the same average stock prices is for the value of the amplification factor, m, to be different. And what appears to be different during the periods of interest we've described above is the expectations of investors with respect to the future rate of inflation.

Ultimately, if we're right, we'll be able to more precisely quantify the value of "m" for use in our stock market math, rather than just going by empirical observations. We'll be better able to forecast where stock prices will go next, which is saying something because we're already pretty good at that.

But then, as we said last month too, we're pretty sure that most investors today would really rather not be part of the science experiment we need to run to get better at that. After all, it took some pretty scary bouts of deflationary pressures for us to notice there might be some sort of connection....

You know, we're really not sure why so many people seem to be surprised that new, seasonally-adjusted, weekly jobless claim filings persist in clocking in at levels above 400,000, or that the adjusted values for the previous weeks tend to be revised upward.

In fact, based upon the trend that has been established since 9 April 2011, that's exactly what we can expect somewhat more than half the time throughout the rest of 2011, provided the current trend continues to remain in effect:

We can arrive at that forecast by following the trajectory of the mean trend line, which is shown as the heavy black line on the chart. Based on the existing trend, we can expect the number of new jobless claims filed in future weeks to be above this line 50% of the time, or below it 50% of the time.

And since that slowly downward trending line is currently projected to stay above the 400,000 level through the end of 2011, we can therefore expect that there is over a 50% probability that the number of new, seasonally adjusted initial unemployment claims will be above the 400,000 mark through the end of the year.

In fact, what we can expect as we go forward in time is that we'll see an increasing number of times in the weeks ahead where the number of new jobless benefit claim filings will fall below the 400,000 mark, as the number of layoffs from U.S. employers each week continues to decline gradually.

At present, that would put the number of layoffs each week in the U.S. on track to reach the average level of 317,000-318,000 that it recorded throughout most of 2006 and 2007 in another 2.6 years. A slight improvement from the 2.7 year figure we projected just two weeks ago, as nothing has happened in that time to significantly affect the overall trend.

Meanwhile, for those of you joining us in progress, here's a look at the primary trends that have characterized the seasonally-adjusted initial unemployment insurance claim filings in each week since 7 January 2006, along with the specific events that we've been able to determine initiated them:

The table below describes the events that altered the trajectory of U.S. layoff since 7 January 2006:

| Timing and Events of Major Shifts in Layoffs of U.S. Employees | |||

|---|---|---|---|

| Period | Starting Date | Ending Date | Likely Event(s) Triggering New Trend (Occurs 2 to 3 Weeks Prior to New Trend Taking Effect) |

| A | 7 January 2006 | 22 April 2006 | This period of time marks a short term event in which layoff activity briefly dipped as the U.S. housing bubble reached its peak. Builders kept their employees busy as they raced to "beat the clock" to capitalize on high housing demand and prices. |

| B | 29 April 2006 | 17 November 2007 | The calm before the storm. U.S. layoff activity is remarkably stable as solid economic growth is recorded during this period, even though the housing and credit bubbles have begun their deflation phase. |

| C | 24 November 2007 | 26 July 2008 | Federal Reserve acts to slash interest rates for the first time in 4 1/2 years as it begins to respond to the growing housing and credit crisis, which coincides with a spike in the TED spread. Negative change in future outlook for economy leads U.S. businesses to begin increasing the rate of layoffs on a small scale, as the beginning of a recession looms in the month ahead. |

| D | 2 August 2008 | 21 March 2009 | Oil prices spike toward inflation-adjusted all-time highs (over $140 per barrel in 2008 U.S. dollars.) Negative change in future outlook for economy leads businesses to sharply accelerate the rate of employee layoffs. |

| E | 28 March 2009 | 7 November 2009 | Stock market bottoms as future outlook for U.S. economy improves, as rate at which the U.S. economic situation is worsening stops increasing and begins to decelerate instead. U.S. businesses react to the positive change in their outlook by significantly slowing the pace of their layoffs, as the Chinese government announced how it would spend its massive economic stimulus effort, which stood to directly benefit U.S.-based exporters of capital goods and raw materials. By contrast, the U.S. stimulus effort that passed into law over a week earlier had no impact upon U.S. business employee retention decisions, as the measure was perceived to be excessively wasteful in generating new and sustainable economic activity. |

| F | 14 November 2009 | 11 September 2010 | Introduction of HR 3962 (Affordable Health Care for America Act) derails improving picture for employees of U.S. businesses, as the measure (and corresponding legislation introduced in the U.S. Senate) is likely to increase the costs to businesses of retaining employees in the future. Employers react to the negative change in their business outlook by slowing the rate of improvement in layoff activity. |

| G | 18 September 2010 | 2 April 2011 | Possible multiple causes. Political polling indicates Republican party could reasonably win both the U.S. House and Senate, preventing the Democratic party from being able to continue cramming unpopular and economically destructive legislation into law, bringing relief to distressed U.S. businesses. Fed Chairman Ben Bernanke announces Federal Reserve will act if economy worsens, potentially restoring some employer confidence. The White House announces there will be no big new stimulus plan, eliminating the possibility that more wasteful economic activity directed by the federal government would continue to crowd out the economic activity of U.S. businesses. |

| H | 9 April 2011 | Present | Rising oil and gasoline prices exceed the critical $3.50-$3.60 per gallon range (in 2011 U.S. dollars), forcing numerous small businesses to act to reduce staff to offset rising costs in order to prevent losses. After this initial shock, as oil and gasoline prices have fallen back to lower levels, so has the number of new jobless claims, but at a less steep pace than before the shock, confirming the reduced optimism of employers for a more strongly improving business climate. |

Provided the established trend remains in effect, the number of seasonally-adjusted initial unemployment insurance claims filed each week in the U.S. is perhaps the easiest economic statistic of all to forecast.

Labels: jobs

In one picture:

1,946,000 fewer teens and young adults between the ages of 15 and 24 were counted as having earned income of any kind between 2006 and 2010, falling from 27,360,000 in 2006 to 25,414,000 in 2010.

During that time, the population of teens and young adults rose by 710,000, from 41,702,000 to 42,412,000.

The income range of $7,500 to $9,999 saw the biggest increase in the number of teens and young adults for any of the income ranges shown on our chart, growing by 299,000 in those four years.

Meanwhile, the number of teens and young adults with total money incomes of $15,000 or less fell by 759,000, despite that dramatic increase in the number of teens and young adults with annual incomes between $7,500 and $9,999.

The federal minimum wage in 2006 was $5.15 per hour. An individual earning the federal minimum wage in 2006 and working full time for the entire year (or 2,080 hours) would have earned $10,712.

In 2010, the federal minimum wage had risen to $7.25 per hour. An individual earning the federal minimum wage in 2010 and working full time for a full year would have earned $15,080.

The net decline of 759,000 people between the ages of 15 and 24 for total money incomes of $15,000 or less represents 39% of the entire decline in the number of teens and young adults with incomes between 2006 and 2010.

But that statistic hides the fact that a total of 1,058,000 incomes for teens and young adults disappeared below the $15,000 level between 2006 and 2010. That figure represents 54% of the total decline in the number of individuals Age 15-24 with incomes from 2006 to 2010.

Labels: demographics, income distribution

We're continuing our visual presentation of the data inside our "How Much Does It Cost to Employ You? (2011-12 Edition)" tool today with a look at the average tax rates paid by employers to support the unemployment insurance benefits mandated by the states in which they operate!

But, because we're always looking at new data visualization capabilities that we haven't previously explored, today, we're simultaneously showing all the data we have by state for each year from 2005 through 2011 in the chart below:

As we did with the workers' compensation tax rate data for 2010, we've posted an interactive version of the chart above and the source data at IBM's Many Eyes data visualization site.

Data Source

U.S. Department of Labor. Office of Workforce Security. Division of Fiscal and Actuarial Services. Significant Measures of State Unemployment Insurance Tax Systems. [2005, 2006, 2007, 2008, 2009, 2010, 2011]. Accessed 15 October 2011.

Labels: data visualization, taxes, unemployment

Which states have the highest average workers' compensation tax rates? And which have the lowest?

The answer is presented visually below:

We've posted an interactive version of the chart above, and we've also made the data publicly available through IBM's ManyEyes data visualization site.

We used this data in our "How Much Does It Cost to Employ You? (2011-12 Edition)" tool, as it's the most recent we have available. We'll be exploring the other data behind the tool later this week!

Data Source

Manley, Mike and Dotter, Jay. 2010 Oregon Workers' Compensation Premium Rate Ranking Summary. Oregon Department of Consumer and Business Services. October 2010.

Labels: data visualization, work

Whether you appreciate it or not, your employer pays quite a bit of money, above and beyond the amount you see on your paycheck to keep you on their payroll. Our tool below estimates how much that is, taking into account things like where you live, what benefits you have, how you get paid and of course, how much you actually see on your paycheck!

Just enter the indicated data into the table below, click the "Calculate" button, and we'll run the numbers....

And that's just for the private sector! Compared to the private sector, people who work for the government will frequently earn equivalent or higher salaries, but will be provided with benefits that far exceed the value of those available in the private sector.

Of course, the economics between work done in the private sector and the public sector are different. The value of the work that employees in the private sector perform must exceed the value of their compensation in order to justify their continued presence on their employer's payroll, generating a combination of revenue or cost savings for their employer. Otherwise, an employer cannot justify keeping the employee on their payroll.

The government however can either raise taxes, arbitrarily increasing its revenue, or can borrow money to pay for its excessively generous compensation packages that no-one in the private sector can hope to receive.

Unless they really earn it, that is!

Labels: business, income, tool

Want to see what happens when someone designs and constructs an intricate structure, where all the individual components are constrained to stay in place, and suddenly, the tension holding the entire system together is broken at just one place?

Well, if you read through that first paragraph, of course you do! Here you go (HT: Core77):

What you've just seen is called a "Stick Bomb". Core77's hipstomp describes it:

A Stick Bomb is simply a grouping of sticks—in this case, tongue depressors or ice cream sticks—woven together in a pattern that creates tension, as seen in the photo above, so that one stick holds another in place. Once that tension is released, you can achieve some surprising things.

Indeed. We wonder if the lessons of the Stick Bomb might be applied to other avenues of human endeavor.

Labels: none really

Isn't it about time that we just stopped thinking of NCAA-member universities as institutions of higher learning and started thinking of them as a massively successful national professional sports league that operates colleges on the side for the tax advantages?

Instead of having federal tax deductions that are based on how much interest you had to pay, which provides incentives to people to rack up a lot of debt, what if we had tax credits that reward people based on how much loan principal they've paid down or that rewards them for maintaining no debt?

Does Dancing with the Stars' Chaz Bono = American Idol's Sanjaya?

Citibank's "Consumer Hourglass Theory" explained by demographics:

Hmm. The very large Baby Boom generation is currently and collectively in its peak earning years, while the very large Generation Y is currently and collectively in its lowest earning years. Meanwhile, the much smaller by comparison Generation X is in its middle-earning years. And for some reason, Citibank's analytical hacks need to concoct the "Consumer Hourglass Theory" to explain why businesses are marketing toward either high-end consumers or low-end consumers, while political hacks are decrying the "destruction of the middle class." For crying out loud hacks: follow the people!

Labels: ideas, none really

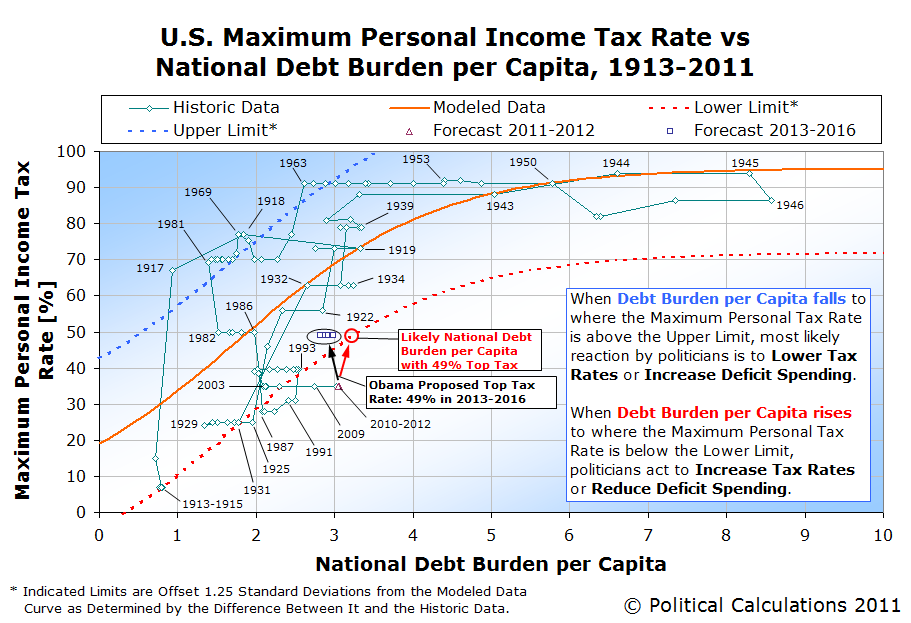

Once upon a time, we created a tool that makes it possible to predict how high U.S. politicians will set the maximum personal income tax rate in the U.S., depending upon three things:

Once upon a time, we created a tool that makes it possible to predict how high U.S. politicians will set the maximum personal income tax rate in the U.S., depending upon three things:

- The size of the U.S.' national debt.

- The nation's GDP, and;

- Its population.

This exercise is especially timely now that President Obama and his Democratic Party are pushing to hike that top rate to 49%, which includes the so-called "Buffett tax", it's time to see how well our tool works.

Using our tool with the default data, we find that today's national debt burden per capita scores in at 3.168, which translates to an "old school" maximum income tax rate of 71.5%. Modern politicians are a different breed however, preferring to stay closer to the margins where changes in the nation's maximum personal income tax rate are likely to be triggered for the political advantages such a strategy offers. Our tool finds that they would set the top tax rate at 48.0%.

President Obama and the congressional Democrats are currently proposing to raise the top tax rate to 49.0% 50.0%.

We should note that the real difference between the "old school" and "modern" politicians is that the "old school" politicians didn't actually know where the margins for triggering changes in the top income tax rate are - it's something that's had to be worked out by political trial and error. It has really only been since the late 1960s, and really, since the 1980s, that U.S. politicians appear to have registered any sort of recognition that these margins exist.

Comparing Today with the Past

The first time we featured this tool back in April 2009, the U.S. national debt was only 11.15 trillion dollars, U.S. GDP was 14.2 trillion dollars and the U.S. population was estimated to be 306,170,293. The national debt burden per capita was 2.565, which corresponds to an "old school" top tax rate of 62.1%. Modern politicians would the top tax rate would be somewhere close to 40% with that old data. And President Obama was, at the time, seeking to let the Bush-era tax cuts expire, which would push the top marginal income tax rate up to 39.6%.

The reason today's predicted maximum income tax rate has risen to 48.0% since that time is completely due to President Obama's spending, which has significantly driven up the national debt.

Of course, we foresaw that President Obama would push for higher income tax rates back in December 2009 as well, finding that the sharp rise in the national debt through that point in time would likely result in the maximum personal income tax rate in the U.S. being set somewhere between 44 and 45%.

And that's exactly where they're currently set to rise in 2013, thanks to the new taxes that congressional Democrats and President Obama imposed through the Patient Protection and Affordable Care Act (aka "Obamacare").

Adding in President's Obama and the congressional Democrats' "Buffett Tax" of 5.4% is how we get to the new proposed top income tax rate of 49% 50%.

Which either means that they're overshooting where they should set the top income tax rate, or are planning to crank up spending and the national debt even more to make that rate seem to make sense.

Updating the Chart

As you might imagine, tracking the interaction between the United States' national debt, GDP, population and U.S. politicians for the sake of predicting how high they might try to set the maximum personal income tax rate gets pretty complicated. Fortunately, we have a chart that visualizes all this data, which incorporates President Obama's optimistic national debt and GDP forecasts through 2016:

What can we say? President Obama is nothing else if not depressingly predictable. We've had his number for a pretty long time now....

Update 13 October 2011: We re-did the math and found the top personal income tax rate would rise to 50.0%.

Labels: forecasting, taxes, tool

Welcome to the blogosphere's toolchest! Here, unlike other blogs dedicated to analyzing current events, we create easy-to-use, simple tools to do the math related to them so you can get in on the action too! If you would like to learn more about these tools, or if you would like to contribute ideas to develop for this blog, please e-mail us at:

ironman at politicalcalculations

Thanks in advance!

Closing values for previous trading day.

This site is primarily powered by:

CSS Validation

RSS Site Feed

JavaScript

The tools on this site are built using JavaScript. If you would like to learn more, one of the best free resources on the web is available at W3Schools.com.

Other Cool Resources

Blog Roll