Ben Schmidt has done some interesting work in visualizing data, with one of his more recent projects involving creating a Sankey diagram of the connections between various college majors and the professions where the people who majored in those field have reported they found work.

Mostly, there's a strong connection between one's major and one's career, but we couldn't help but notice that those who studied Journalism in college tended to end up just about anywhere else:

The Top 10 careers where journalism majors find work, ranked from most popular to least, include:

- Marketing and Sales Managers

- Elementary and Middle School Teachers

- Miscellaneous Managers, Including Funeral Service

- Lawyers, Judges, Magistrates and Other Judicial

- Retail Salespersons

- Secretaries and Administrative Assistants

- Wholesale and Manufacturing Sales Representatives

- First Line Supervisors of Retail Sales Workers

- Postsecondary Teachers

- Market Research Analysts and Marketing Specialists

We find it pretty interesting that legal careers rank fourth, especially since those careers require considerably more schooling than the other listed professions, most of which don't require much in the way of schooling, much less schooling in journalism. We wonder what we should make from that?

Perhaps what that tells us is that the people who study journalism are really looking for an easy degree. After all, if you're going to have to bust your back end to earn a law degree after you get some other degree first, why not spend the first four years of your post-secondary education studying something that sounds so much more pretentious than a humble business degree, but that allows you to party more while still keeping the door open to a meaningful career in so many marketing and sales professions in case the law school thing doesn't work out?

Because apparently, it's not like you really have to learn anything like how to actually report news as a journalism major in college these days.

Labels: data visualization, education, jobs

According to preliminary data released by the U.S. Census Bureau, for the second time in the past three months, the trailing twelve month average of new home sale prices declined.

In April 2014, the initially reported figure for the median new home sales price was $275,800, down from the revised figure of $281,700 in the previous month. More significantly, the trailing twelve month average of median new home sale prices, which allows us to minimize the effects of seasonality in the housing data, fell from $268,583 in March 2014 to $268,292 in April 2014.

The last time the trailing twelve month average of median new home sale prices declined was in June 2012, right before the second U.S. housing bubble began to inflate.

So what might that mean for the U.S. economy?

Historically, for the 605 months through April 2014 for which we have trailing twelve month data (or rather, from December 1963 through April 2014), there are 103 months in which the trailing year data for median new home sale prices fell from the preceding month. 42 of those months coincided with periods of outright economic contraction in the U.S.

The average economic growth rate for the 103 months of declining median new home sale prices is 1.0%. The average economic growth rate of the remaining 402 months is 3.5%.

According to the National Association of Home Builders, new housing construction (residential investment) typically makes up about 5% of GDP. Over the last four quarters, it has accounted for an average of 3.1% of the nation's GDP.

We think that housing prices are a coincident-to-slightly-lagging indicator of the relative health of the U.S. economy - it's something that tends to be in sync with the overall state of economic conditions in the U.S. As such, housing prices are confirming something we already know - the U.S. has been experiencing recessionary conditions in early 2014.

Labels: real estate

According to the Associated Press, the typical Chief Executive Officer of a company makes 257 times the average worker's salary.

Is that really a problem?

Here's why we ask that question - how much somebody earns in doing a job depends tremendously on who else can do their job. For example, people who earn the minimum wage tend to have minimal job responsibilities. Consider the case of Tyree Johnson, a 20-year McDonalds employee:

After 20 years cooking burgers and manning the fryer for the national chain, Tyree Johnson still makes just the minimum wage, Bloomberg reports. That's $8.25 an hour in 44-year-old Johnson's hometown of Chicago, where he works at two different McDonald's restaurants.

First, let's look at what it would take to replace Tyree Johnson as a fry cook at McDonalds. Here's a recollection of a St. Louis McDonalds' crew member's experience in being hired and trained:

I applied in-person and the process took a day - interviewed at McDonald's in March 2013.

Interview Details – The interview process took less than 15 minutes. It wasn't really thorough or relevant. Once hired, you go through a two day training period. It was a group interview and not hard at all.

Negotiation Details – You got to choose the hours you worked and they attempted to make a flexible schedule.

Of course, one of the big reasons that so little training is needed is because McDonalds invests heavily in automating many aspects of restaurant work, with the position of cashier likely to be the next job at McDonalds that will make more sense to have done by technology rather than by people. As a business, McDonalds does not rely upon employing workers at minimal wages for its profits, as it long ago recognized that standardizing and automating work was its key to growth. Consequently, McDonalds employees earn wages consistent with those who might replace them in their very limited roles.

By contrast, a CEO is responsible for overseeing the operations at all levels of a company's operations and all locations at which the company does business. The CEO is responsible for all aspects of the company's business strategy and is responsible for reporting on the state of the business to the company's owners, which in many cases, includes themselves. Generally speaking, a CEO is not easily replaceable, taking months to put into place, at a minimum.

In 2012, McDonald's CEO Jim Skinner earned $8.75 million. He retired and was replaced by Don Thompson in June 2012, who had joined McDonalds 22 years earlier, leading projects to design and develop robotic equipment for food transport and control circuits for automating cooking operations at McDonalds' 34,000+ restaurants worldwide. Thompson had been being groomed to become McDonald's CEO since being promoted to be the company's Chief Operating Officer in June 2010. In 2013, Thompson earned $9.5 million as CEO.

We're making a point of emphasizing the sheer scope of McDonalds' operations because that's the key to understanding what drives the pay of CEOs.

Xavier Gabaix and Augustin Landier found back in 2008 (using data up through 2003) that CEO pay follows a special version of a power law, known as Zipf's Law, where what a major company's CEO earns is directly proportional to the size of the firm that they are responsible for running. The chart below shows the correlation between firm size and CEO compensation for the top 500 public firms in 2010:

But more importantly, Gabaix and Landier have updated their earlier results to include data through 2011, allowing them to determine whether the relationship between firm size and CEO compensation would hold through the extreme gyrations the economy experienced in going from boom, to bust and then into recovery. Here's the abstract of their 2013 paper updating their findings:

In the 'size of stakes' view quantitatively formalised in Gabaix and Landier (2008), CEO compensation reflects the size of firms affected by talent in a competitive market. The years 2004-2011 were not part of the initial study and offer a laboratory to examine the theory with new positive and negative shocks. Executive compensation (measured ex ante) did closely track the evolution of average firm value, supporting the 'size of stakes' view out of sample. During 2007 - 2009, firm value decreased by 17%, and CEO pay by 28%. During 2009-2011, firm value increased by 19% and CEO pay by 22%.

We see then that CEO pay is indeed driven by firm size.

In fact, the only time we see CEO compensation race far above what we would expect based upon firm size directly corresponds to the years of the Dot-Com Bubble, where a reduction in the capital gains tax rate without a corresponding reduction in dividend tax rates created massive distortionary imbalances in the U.S. economy. Imbalances, we might add, affected people earning minimum wages by just as much as those who pocketed that era's massive capital gains.

And for those people whose pay is determined by the wages that would be paid to their potential replacement, perhaps a good question to ask is what can you do to generate enough additional revenue to justify a higher paycheck for yourself without passing the costs on to your customers. Because the odds are that the CEO of the company where you work already has some idea of what that answer might be.

And you know that they've just gotta be loving it!

References

Xavier Gabaix & Augustin Landier & Julien Sauvagnat, 2014. "CEO Pay and Firm Size: An Update After the Crisis," Economic Journal, Royal Economic Society, vol. 124(574), pages F40-F59, 02. http://www.nber.org/papers/w19078. [Ungated Version].

Political Calculations. Debunking Income Inequality Theory. http://politicalcalculations.blogspot.com/2014/01/debunking-income-inequality-theory.html. 23 January 2014.

Political Calculations. What Caused the Dot Com Bubble to Begin and What Caused It to End? http://politicalcalculations.blogspot.com/2010/12/what-caused-dot-com-bubble-to-begin-and.html. 15 December 2010.

Labels: business, income inequality, jobs

From time to time, we encounter some really strange comments from people who are generally well respected in the world of stock market analysis.

Meet Dennis Gartman, since 1987, the author of the Gartman Letter, and frequent commentator on CNBC. Here's what he said about the current state of the stock market just last week, on Wednesday, 21 May 2014:

The stock market is in the midst of a correction, closely followed investor Dennis Gartman told CNBC on Wednesday.

"I think the process began several weeks ago … [with] the Nasdaq," the publisher of The Gartman Letter said in a "Squawk Box" interview. "We're in a correction right now."

A correction is defined as a 10 percent decline in major averages from their highs. As of Tuesday's close, the Dow Jones Industrial Average was down 2 percent, the S&P 500 was down 1.5 percent, while the Nasdaq was off 6 percent from their 52-week highs.

It doesn't sound like much of a correction, does it? And if you paid attention to where stock prices went on to finish the week, as the S&P 500 closed at a new record high, it's pretty difficult to square Gartman's declaration with apparent reality.

But, what if there was a correction - a major one - that nobody noticed because it was invisible?

Here's how that might work. Last week, we recognized that stock prices had begun deviating from where our dividend-based model had indicated they would be in the previous week, as the stock market was experiencing what we described as a "noise event". We went on to say that we expected that stock prices would "once again converge with the future as defined by the dividends expected for 2014-Q3, which would be positive for stock prices in the short term", unless it were followed by an additional noise event.

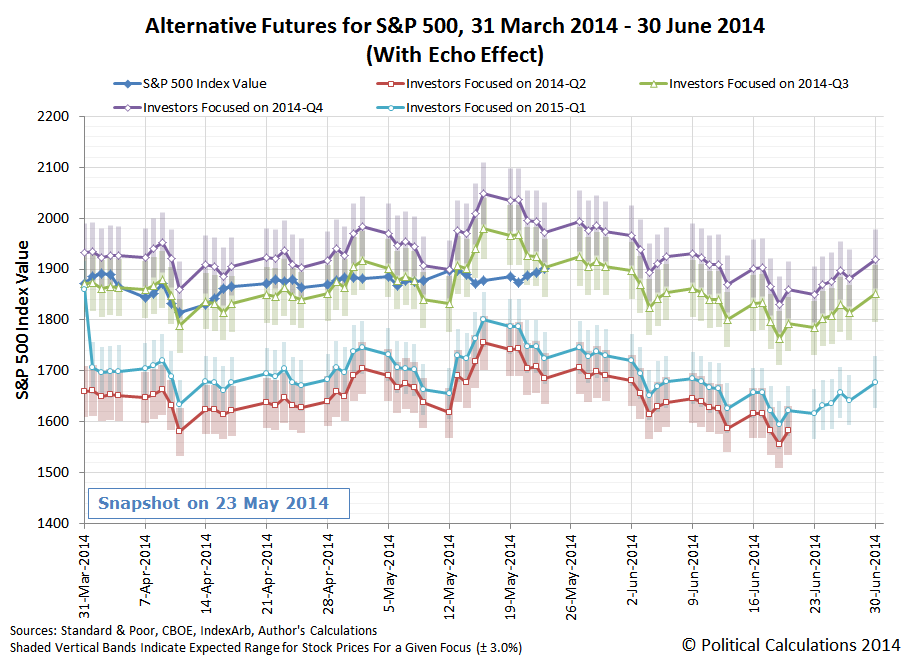

Alas, that's exactly what happened on 20 May 2014! Fortunately, that was a very short-lived noise event, as stock prices went on to "converge with the future as defined by the dividends expected for 2014-Q3" on Friday, 23 May 2014.

Words can only do so much to describe that activity, so here's our alternative futures chart, updated with the actual recorded stock prices through Friday, 23 May 2014, to help visualize what happened:

So if you look at the period between 14 May 2014 and 23 May 2014, you see a pretty big deviation between what stock prices actually were and what our model projected. In fact, there's about a 108 point difference between the midpoint of the likely range of stock prices associated with a focus on 2014-Q3 and what the S&P 500 actually did. That gap represents the equivalent of a 5.4% correction.

And if for some reason investors had shifted their forward-looking focus to 2014-Q4 during that time, that gap opens up to be 177 points wide - an 8.6% virtual correction!

That means that what we have here is an invisible correction - where stock prices were set to rise substantially, but didn't, because a significant correction wiped out all of the rise, leaving behind the impression that stock prices were mostly drifting sideways instead.

Yeah, we don't buy that one either, but it's fun to think about! As for Dennis Gartman, let's revisit his call back in February 2014 that the stock market was set to experience a 15% correction, and see how that worked out:

A prediction that stocks would see a 15 percent correction was off, Dennis Gartman said Monday.

"Vociferously, I'd say I was wrong," he said. "We got to a trend line that really did hold. I didn't think it would hold. It did, in fact, hold."

Hmmm. "A trend line that really did hold". We think we may know what's giving Gartman those false signals....

The general consensus among most people who seriously study markets is that technical analysis is mostly garbage.

After all, how can a investing method that completely disregards a company's fundamental business prospects in favor of tracking its stock price over time possibly ever get anything right except by chance?

In fact, the most wide-ranging study conducted to date of technical analysis as a trading strategy found that it wasn't consistently profitable in any of the stock exchanges of 49 countries. Furthermore, of the 5,806 technical analysis trading rules they tested, none provided any "value beyond what may be expected by chance".

So why would investors waste any time on it at all?

One insight to that question was provided by Morris Armstrong, who used technical analysis while working as a currency trader:

I used technical analysis quite alot when I was a currency trader and I think that it adds a lot of value in the establishment of entry and exit points when contemplating a position. It will also allow you to get a very good idea on when a trend is getting tired or is picking up steam again.

I am not sure if people think that it is a tool for investment strategy but it certainly is a good tool for trading.

Besides, in trading there is the old axiom "I'd rather be lucky than good"

Well, there is always that to stake your livelihood upon, isn't there?

The reason we're bringing this up today is because our recent discussion of the actual mechanism that might lead stock prices to "revert to the mean" as stock prices follow a trend provides an ideal opportunity to see if technical analysis might be anything other than worthless.

Specifically, the idea of whether the moving averages used by technical traders can give us any legitimate insights. We'll do that by overlaying the 20-day, 50-day and 200-day moving averages over our power law statistical equilibrium chart to see how well any of these components might coincide with elements of our analysis that have statistical meaning. The chart below shows the results of that exercise:

We selected this period because it coincides with a relative period of order in the U.S. stock market extending through the present day, where the variance of stock prices might be reasonably approximated with a normal distribution. As such, if technical analysis is going to provide any sort of meaningful insight, it should work in this environment.

But before going further however, we should note that stock prices do not closely adhere to a normal distribution - the best that can be said of them is that they do follow a central tendency, but that the variance of their distribution about this central tendency is not normal. This assumption however lets us apply the tools that have been developed for statistical analysis, which provides useful insights in our regular analysis.

Let's focus on the 200-day moving average to see what its interaction with stock prices and the various statistical indications shown on our chart can tell us about the value of using this technical indicator to choose entry and exit points for investments. Specifically we'll focus on whether seeing stock prices drop below the 200 day moving average is sending a buy or sell signal, defining where an investor should enter or exit the market.

Here, the most evident thing that stands out to us in the chart above is the relative position of the 200-day moving average with respect to the lower equilibrium limit of our chart when trailing year dividends were between $31 and $34 per share, which occurred between mid-December 2012 and mid-August 2013.

Since the 200-day moving average is often considered to be a "support level" for stock prices, its overlapping of this lower limit of the statistics-based range in which we would expect stocks to fall actually has real meaning. If stock prices drop below this range, that would be an indication that order is breaking down in the stock market, which would be a very clear indication to sell if history is any guide.

Unfortunately, that nine-month period was the only time in the last two and three-quarter years where the insight provided by technical analysis might have been useful. Otherwise, we see that the 200-day moving average has spent much of its time at a level about one and half standard deviations below the mean trend trajectory for stock prices. At this relative position, if stock prices were to drop below this level, it would really be an indication to buy, where an investor would benefit whenever stock prices might revert back to the mean.

These opposing scenarios reveal why technical analysis fails. Unless you know where the 200-day moving average is with respect to the range into which stock prices will most likely fall, whether following an upward or a downward trend, there's no guarantee that an investor relying upon technical analysis will make the correct investment decision given the same technical signal.

It really is like flipping a coin, since success is random. And really, random at best - most investors who use technical analysis "frequently make poor portfolio decisions".

In conclusion, we consider technical analysis to be, at best and under very limited circumstances, a very, very weak form of statistical analysis. At worst, more effective and less time consuming ways of making sound investment decisions would involve flipping coins or reading tea leaves.

References

Marshall, Ben R. and Cahan, Rochester H. and Cahan, Jared, Technical Analysis Around the World (August 1, 2010). Available at SSRN or dx.doi.org/10.2139/ssrn.1181367. Ungated version available [PDF Document].

Now that we've discussed what "reverting to the mean" means for stock prices, let's peer into the future to see when that will likely happen for the S&P 500.

To do that, we're building upon our original observations of the relationship between changes in the growth rate of stock prices and changes in the growth rate of dividends per share.

Here, we discovered that by applying a simple amplification factor and by shifting the data for dividends backward in time, we could pretty closely match the change in the growth rate of stock prices at given points in time with the change in the growth rate of dividends per share at later date.

What that indicates is that investors are looking forward to specific points of time in the future as they set stock prices in the current day. And if you know what investors expect for the future for dividends, you can then forecast with a decent amount of accuracy how stock prices will change over time.

The challenge in doing that is determining which point of time in the future they have focused their attention upon in setting stock prices. Thanks to dividend futures data, we know what dividends are expected to be at specific points of time in the future, but can only identify which point in time that might be by observation.

Let's do that now. Starting with our power law statistical equilibrium chart, which shows the daily closing value of the S&P 500 against its underlying trailing year dividends per share (with the daily data interpolated between quarters):

Let's focus just on 2014 and superimpose what stock prices are projected to be for a given investor forward-looking focus on the dividends expected to be earned in each of the next four future quarters, from 2014-Q2 through 2015-Q1:

In this chart, you can see how stock prices have closely paralleled the projected stock prices for the various points of time in the future that investors have focused upon since the beginning of the year. More importantly, you can also see how stock prices have shifted to follow the trajectory for the future focused upon by investors whenever they have shifted their attention from one point in the future to another.

Looking forward through the end of 2014-Q2, we see that regardless of which future investors choose to focus upon, stock prices should fall below the mean trajectory of their established long term trend in the very near future.

That's the when for mean reversion, at least according to the math that describes how stock prices work. We should also note that there are times when stock prices deviate from these defined trajectories, which we typically describe as noise events when they occur. Subsequent event studies of the data during these times suggests that these are periods in which investors are splitting their forward-looking focus between two or more points of time in the future as they set current day stock prices.

What does it mean to say that stock prices will "revert to their mean"?

After all, aren't stock prices supposed to be random? And if they are really random, how on earth could they be following any sort of stable trend for any length of time, whose mean trajectory they might periodically revert back to as time goes by?

And yet, if we look at a long enough period of time, say 22+ years, we find that stock prices would appear to follow definite trends for up to years at a time. Even as they seem to bounce about randomly about these trends as they follow them.

Now here's where it gets interesting. From this chart, it's really tempting to start drawing lines where you see trends to try to define them. And in fact, there's a whole field within investing and finance that's dedicated to the practice called technical analysis, where its practicioners seek to identify trends as they progress over time to make investment decisions.

Technical analysis, as it's generally practiced, has a critical flaw. When one charts stock price trends over time, the effect is to treat stock prices as if they are a function of time.

Nothing could be further from the truth, and to understand why, just consider how many times in the chart above that you see the S&P 500 with a value of 600 and how many times you see it with a value of 1200. If time were the driving factor for stock prices, we would see stock prices steadily progress ever upward as time marches ever forward.

That we do not see that tells us that some other factor is the primary driver of stock prices. Our next chart shows what we've identified that factor to be and its relationship with stock prices during the major relative periods of order in the stock market since December 1991:

This chart is an updated version of the one that originally marked one of our original discoveries - the extent to which stock prices and dividends are correlated - particularly during the trends that define relative periods of order in the stock market. Periods of order, we might add, that are punctuated by periods of chaos.

The thing to take away from this chart however is the relationship shown between stock prices and their underlying trailing year dividends per share. That definition allows us to do something that technical analysts can only dream of - to map out the trends about which stock prices might actually revert!

Even better, we can apply the tools of statistical analysis to do that job, as one of the other things we've discovered is that during relative periods of order in the stock market, the variation of stock prices about the trends we've mapped would appear to follow a normal distribution. Or more accurately, during these periods, we cannot reject the statistical hypothesis that stock prices behave "normally". (As you can see in the chart above though, those rules don't apply during relative periods of chaos in the stock market!)

So what does that have to do with the potential for mean reversion? Well, if we apply our tools, we can see where stock prices currently are with respect to their established mean trajectory during relative periods of order. At present, and really, since 4 August 2011, we find that the U.S. stock market has been in what we would describe as a relative period of order:

By definition, when following a trend, stock prices will be above their established trend about 50% of the time and below it 50% of the time. In looking at the chart above, we see that stock prices have been above their established trend for quite a while now, which is a pretty significant factor behind why a number of market observers are increasingly anxious over why we haven't seen a significant correction for so long.

Even if they can't quite put their finger on why.

It would certainly help to know the future to sort out how a reversion to the mean would play out, wouldn't it? Fortunately for you, that's where we work, so how about we give you a general idea of how and when the phenomenon of mean reversion will play out, assuming no noise events interfere with the schedule for the future? Say, in our next installment, where we'll apply the tools we've invented to cope with the market during periods of chaos!

We think that Pinch Sulzberger is an idiot.

There. We said it. Now, let's discuss why we think that....

It all starts with a story that was floated to and repeated by the New Yorker's Ken Auletta regarding the reasons why Sulzberger sacked Jill Abramson, the woman who has worked for several years as the Executive Editor of the New York Times as that company worked to shrink its way toward profitability under her leadership. The emphasis in the following section is ours:

Several weeks ago, I’m told, Abramson discovered that her pay and her pension benefits as both executive editor and, before that, as managing editor were considerably less than the pay and pension benefits of Bill Keller, the male editor whom she replaced in both jobs. “She confronted the top brass,” one close associate said, and this may have fed into the management’s narrative that she was “pushy,” a characterization that, for many, has an inescapably gendered aspect. Sulzberger is known to believe that the Times, as a financially beleaguered newspaper, needed to retreat on some of its generous pay and pension benefits; Abramson, who spent much of her career at the Wall Street Journal, had been at the Times for far fewer years than Keller, which accounted for some of the pension disparity. Eileen Murphy, a spokeswoman for the Times, said that Jill Abramson’s total compensation as executive editor “was directly comparable to Bill Keller’s”—though it was not actually the same. I was also told by another friend of Abramson’s that the pay gap with Keller was only closed after she complained. But, to women at an institution that was once sued by its female employees for discriminatory practices, the question brings up ugly memories. [Update: On Thursday, Sulzberger gave his staff a memo on what he said was “misinformation” on the pay question. “It is simply not true that Jill’s compensation was significantly less than her predecessors,” he wrote. “Her pay is comparable to that of earlier executive editors.”] Whether Abramson was right or wrong, both sides were left unhappy. A third associate told me, “She found out that a former deputy managing editor”—a man—“made more money than she did” while she was managing editor. [Update: The man in question, John Geddes, was in fact the managing editor of news operations.] “She had a lawyer make polite inquiries about the pay and pension disparities, which set them off.”

The reason we believe that Sulzberger is an idiot is because his solution to the problem of unequal pay at the New York Times was to significantly boost the pay of his top-ranking female employee. If he were more serious about running a successful and more profitable business, he should have replaced all the overpaid men on the New York Times' staff with women willing to do the same jobs at lower levels of compensation.

To demonstrate why, we'll adapt the math on wage gaps that was recently developed by economist Steve Landsburg to the particular situation that applies at the New York Times and media organizations in general. To do that, we'll use data provided by Pew Research and the New York Times' 2013 annual report.

The results of the math in our tool below will tell us how much more profitable the New York Times could have been, if only Pinch Sulzberger were not so determined to maintain just under two men for every one woman on the New York Times' payroll at their average 20% higher pay.

That additional 10.4% profit may not seem like much, but the financially-troubled New York Times Company would not have had to shrink so much in recent years if Sulzberger had implemented such a lower wage-paying strategy. Sexism is costing Sulzberger's New York Times' money.

And that's why we think that Pinch Sulzberger is an idiot. As it happens, others have other reasons for thinking the same thing.

Image Credit: Christopher Coons.

Labels: business, math, satire, tool

If stock prices dipped just one percent after reaching their all-time high last week, why are investors so freaked out?

The answer has to do with the sudden onset of a new noise event in the stock market, which began making its present known around 2:40 PM EDT on Wednesday, 14 May 2014. Our accelerations chart reveals the sudden downward shift of stock prices with respect to the change in the growth rate of dividends per share for each future quarter from now through 2015-Q1:

Applying what we've been learning about the nature of noise events - namely, that they really represent events where investors suddenly and temporarily shift some or all of their forward-looking focus in setting today's stock prices toward a different point of time in the future from where they had been, finding the specific mechanism that would appear to have driven the sudden shift took very little effort for us last week, thanks to an aside offered by UBS' equity and derivative strategist Julian Emanuel in a discussion with CNBC:

"As an aside, there's been some concentrated large-size sellers of June out-of-the-money (S&P 500) options—1910 and 1920 calls, and on the downside 1840 and 1850 puts," Emanuel said. "As the market goes toward either of those strike prices, the possibility for acceleration increases through the strike prices."

As we can see by each of the dividend futures in our chart above, the expectations for the future didn't meaningfully change last week. But what Emanuel's observation confirms for us is that the point of time that investors were focused upon changed. In this case, that forward-looking focus changed from 2014-Q3, where it has been for weeks, to suddenly pull back somewhat toward 2014-Q2 ("June"), corresponding to the unusually concentrated put activity.

This is very similar to what we observed for the events of 26 March 2014 in our now infamous "experiment".

The good news is that it would appear that the noise from this event has already begun to dissipate. But still, the presence of the noise has spooked a number of investors, for whom the effect of the noise has placed stock prices considerably below the level that they might have otherwise reasonably expected.

Assuming that the last noise event continues to dissipate and isn't followed by any additional new noise events, our best thinking is that stock prices will once again converge with the future as defined by the dividends expected for 2014-Q3, which would be positive for stock prices in the short term.

But in the longer term, if that convergence is sustained, it would ultimately lead stock prices lower, where it seems a reversion to the long-term mean may be in the works. More on that later this week....

Update: 20 May 2014: New York Fed President William Dudley, who had previously been considered an interest rate dove in favoring hiking rates later rather than sooner, indicated today that such hikes might now occur sooner rather than later. Other influential Fed Presidents have indicated that such an action may come as early as by the end of 2015-Q1.

If you look at our accelerations chart above, what effect do you think that shifting the focus of investors toward 2015-Q1 would have on stock prices today? P.S. - Also try to guess at what time that Dudley began speaking (hint: a minor decline from the day's mid-day peak suddenly steepens!...)

So did stock prices behave any differently on Tuesday, 20 May 2014 from what we should expect under these circumstances?

The bottom line: it's a new noise event - one following the one we described in the post above. You can thank the Fed's minions for it.

Via Core77, meet the Miracle Machine - a device that you can use to make high quality wine at home in just a few days with low-cost basic ingredients, which uses a smart phone app to let you monitor how it's fermentation process is coming along:

Do you have what it takes to make your own wine? Most likely not. But with this fancy gadget and a lower-than-average amount of skepticism, you might. Drink like Jesus did with the Miracle Machine: just add water, grape concentrate, yeast and a vaguely described "finishing powder" to impart that truly barrel-aged flavor without true barrel-aging.

The modestly named Miracle Machine is a household appliance with the capability of fermenting and age-flavoring fine wine within three days, for as little as $2 per bottle in materials.

Here is developers Kevin Boyer and Philip James' "Kickstarter" pitch:

Sound too good to be true? That's likely because it was.

In reality, the water-to-wine Miracle Machine turned out to be quite a publicity stunt:

It's amazing what you can do with some attractively turned wood, plastic and LEDs these days!It sounded like a dream come true. The Miracle Machine was a gadget that would turn water -- along with grape concentrate and yeast -- into wine in your very home in as little as three days. A lot of people got excited, imagining becoming home winemakers without all the bother of growing grapes, aging in barrels, or knowing anything about how to make wine.

There was just one catch, and it was a big one. The Miracle Machine is a made-up product. The Miracle Machine founders promised a Kickstarter launch, but that debut never materialized. It was just a hook to get people to sign up for more information. Today, those people got an e-mail leading them to a video about Wine to Water, a nonprofit organization dedicated to supplying clean drinking water to people in need around the globe.

The end game for the stunt is to raise awareness of Wine to Water and drive donations and volunteers to the cause. The people behind it say that more than 600 media outlets around the world picked up coverage of the fake product within the last 10 days.

Labels: technology

The WSJ's Real Time Economics blog recently caught our attention with the following headline: Why the Nation's Hot Housing Market Is Cooling Slightly.

After wiping down our monitor after our initial spit-take, we found it to be a fairly decent article, summarizing much of what we've observed and reported upon in the nation's housing industry months ago. But then, we had to wipe down our monitor again as we read the following section:

“One of the reasons that demand appears to be slowing is that the pace of previous home-price increases has negatively affected affordability,” Mr. Lawler said. “And some of the previous year-over-year gains were from depressed levels when there was a lot of distressed inventory on the market.”

Economists have differing opinions on the extent to which price increases have made homes less affordable for buyers. Interest rates are higher, with the rate for a 30-year fixed-rate mortgage now at 4.21%, up from 3.42% a year earlier, according to Freddie Mac. Mortgage-insurance fees also have increased.

However, the Realtors association argued Monday that homes remain affordable, noting that a buyer purchasing a home at the first-quarter median price with a 5% down payment would need an income of $44,200 to land a mortgage. With a 20% down payment, the necessary income is $37,200, the group said.

To understand why we needed to wipe down our monitor again, let's turn to Barry Ritholtz' classic unloading upon the lack of utility offered by the National Association of Realtor's Housing Affordability Index:

In the past, we have discussed how worthless the NAR’s Housing Affordability Index is. This weekend saw an odd column in Barron’s that was suckered in by the silliness of that index.

This suggests to me it is time to take another pass showing exactly why this index has so little value to anyone tracking housing values and affordability. let’s begin by going back to our 2008 analysis:

“The index as presently constructed is utterly worthless. It provides little or no insight into how affordable US Housing actually is. Further, what is omitted from the index is especially relevant to the problems occurring in the housing market today. The Index fails to account for — or even recognize — any of the out of the ordinary circumstances that are currently bedeviling the Housing market.”

That’s not the worst of it — during the huge run up from 2001-2007, there was but one month — ONLY ONE MONTH! — where the NAR said homes were not affordable!

Only One Month When NAR Said Homes Were Not Affordable

Going by the chart, the only time the National Association of Realtor's Housing Affordability Index ever suggested that housing prices were not "affordable" by their standards was in late 2005.

Let's review how the median sale prices of homes evolved with respect to median household incomes since 2000:

Using the values provided by the NAR for an individual purchasing a $191,600 home with a 30-year mortgage at 4.21% with either a 5% down payment at an annual pay of $44,200 or with 20% down with an annual income of $37,200, it would appear that the main qualification the National Association of Realtors places upon determining whether a home is within the reach of affordability for a potential buyer is whether the homebuyer is willing to contribute as much as 24% of their annual income toward just their mortgage's principal and interest payments for thirty years.

By contrast, we've already demonstrated that the typical share that U.S. homeowners actually dedicate of their annual income toward home ownership is 10%, which is what most Americans would say defines the real line of affordability for the cost of owning a home.

The difference between these two figures is why the NAR's housing affordability index is such a poor indicator of housing affordability. But then, these are the same people who insist that there has only ever been one month in all of U.S. history in which there was a better time to buy a house.

Labels: real estate

Approximately every three months, we take a snapshot of the expectations that investors have for the S&P 500's trailing year earnings per share. The chart below represents the Spring 2014 update for our series, showing what has changed for investors in the three months since February 2014:

We find that earnings for the S&P 500 in the first quarter of 2014 are falling significantly below what investors had expected in the middle of the first quarter, but curiously, they would seem to be in line with what investors had expected three months earlier, in November 2013.

So what got the hopes of investors up so much in mid-February 2014?

The answer might be a misplaced belief in economic momentum - investor expectations for earnings in 2014-Q1 were buoyed upward by companies reporting stronger than expected earnings for the fourth quarter of 2014, as indicated by contemporary reporting:

The major US indices registered their strongest week so far this year and injected investors with optimism. The combined effect of better-than-expected earnings reports and a growing confidence in the economy gave a boost to US indices. The S&P500 rose by 2.35% reaching 1,839, the Dow added 2.28% to its value to close at 16,150 points on Friday, while the technological Nasdaq100 increased by 2.86% to end the week at 3,663 points.

Curiously, investors didn't appear to believe that harsh winter weather would be a significant factor for the quarter:

The stock market started lower Friday following news that U.S. factory output fell sharply in January. Manufacturers made fewer cars and trucks, appliances, furniture and carpeting, as the recent cold spell ended five straight months of increased production.

The Federal Reserve said factory production plunged 0.8 percent in January, following gains of 0.3 percent in both December and November.

Investors are hopeful that much of the weakness seen in recent economic reports is due in large part to the unusually cold winter weather this year, said Kristina Hooper, US investment strategist at Allianz Global Investors.

"Investors are choosing to look at very mixed data through a positive lens," Hooper said.

In retrospect, investors were correct to discount the negative impact of harsh winter weather, but misread the signals that were being sent by U.S. automakers at the end of November 2013, long before the cold of winter had any impact, indicating that they had misjudged consumer demand going into the end of the year and would need to cut their production as the sales weren't there to support it. The same was true for homebuilders, where the new home sales that might drive purchases of appliances, furniture and carpeting also were decelerating long before Winter 2014 arrived.

In other words, the poor economic performance of 2014-Q1 had little, if anything, to do with unusually cold winter weather in much of the U.S., which is the real reason why investors have had to deflate their expectations for that quarter's earnings.

And as you can also see in the chart above, they've deflated their future earnings expectations all the way through the end of 2015.

Data Source

Silverblatt, Howard. S&P Indices Market Attribute Series. S&P 500 Monthly Performance Data. S&P 500 Earnings and Estimate Report. [Excel Spreadsheet]. Last Updated 8 May 2014. Accessed 13 May 2014.

Labels: earnings, forecasting, SP 500

What percentage of an average U.S. business' revenue goes to pay wages and salaries? Or employer-provided health insurance benefits? How much goes to pay debt? How much gross business income is retained on average to be invested in new capital?

You can spend a lot of time searching the web to try to answer basic questions like these and still fall short of filling in much of the whole picture, or you can take advantage of our already having done that for you! Our chart below presents our results graphically:

Here's how we came up with that visual breakdown. Starting with 100% of all revenue, or income, taken in by a business, we first find that through the end of 2013, the share of that amount that goes to compensate labor is 61%, with the remaining 39% being accounted for by capital.

Breaking down the labor side of the accounting, we find that 69% of that portion of total business revenue goes to actually pay wages and salaries, and 31% goes to provide employee benefits.

Continuing to drill down, we found that 30.4% of all benefits is represented by paid leave and supplemental pay, which covers things like vacations, holidays, overtime, bonuses and shift differentials. Employer provided health insurance accounts for 27.5% of all employee benefits, with employer provided life insurance adding an extra 1.5%. Pension and retirement benefits represent 15.6% of all money spent on employee benefits. Finally, mandated benefits for compensating labor, which includes the portions of Social Security and Medicare paid by employers as well as unemployment insurance and workers compensation, makes up the remaining 25% of money spent on employee benefits in the U.S.

Looking at the capital side of the ledger, we find that money here is split into three main categories: payments to debtholders (40% of capital), payments to business owners or shareholders (31.6% of capital) and money that stays with the business to support new capital investments (28.4% of capital).

That's how each of these major categories break down as either a percentage of labor or of capital. Our table below goes one step further and reveals the percentage share of each of these major categories consume of the total income generated in the U.S. going into 2014:

| Percentage Share of Component of Labor or Capital of Total Business Income, 2014 | ||

|---|---|---|

| Category | Component of Labor or Capital | Share of Total Revenue (or Income) |

| Labor | Wages & Salaries | 42.1% |

| Paid Leave & Supplemental Pay | 5.7% | |

| Employer Provided Health Insurance | 5.2% | |

| Pension & Retirement Benefits | 2.9% | |

| Mandated Benefits | 4.7% | |

| Employer Provided Life Insurance | 0.3% | |

| Capital | Payments to Debtholders | 15.6% |

| Payments to Shareholders | 12.3% | |

| Retained Earnings | 11.1% | |

If you want to drill down even deeper on your own, our data sources are presented below....

References

U.S. Bureau of Economic Analysis. National Income and Product Accounts Tables. Table 1.12. National Income by Type of Income. [Online Database]. Accessed 10 May 2014.

U.S. Bureau of Labor Statistics. Employer Costs for Employee Compensation - December 2013. [PDF Document]. 12 March 2014.

Bolton, Patrick, Mehran, Hamid and Shapiro, Joel. Executive Compensation and Risk Taking. Federal Reserve Bank of New York Staff Reports. Staff Report No. 456. [PDF Document]. June 2010. Revised November 2011.

Ameta, Michael. Factset Dividend Quarterly. [PDF Document]. 24 March 2014.

Labels: business, data visualization, math

How much do events in the past drive stock prices today?

Last week, we took advantage of a natural experiment with the stock market to find out (not to be confused with the somewhat larger "experiment" we described previously, where we have subsequently been cleared of any mal-intent thanks to an investigation by the Financial Investment Regulatory Authority. Really - it was the satisfying conclusion to the most successful April Fools' prank we've executed to date!)

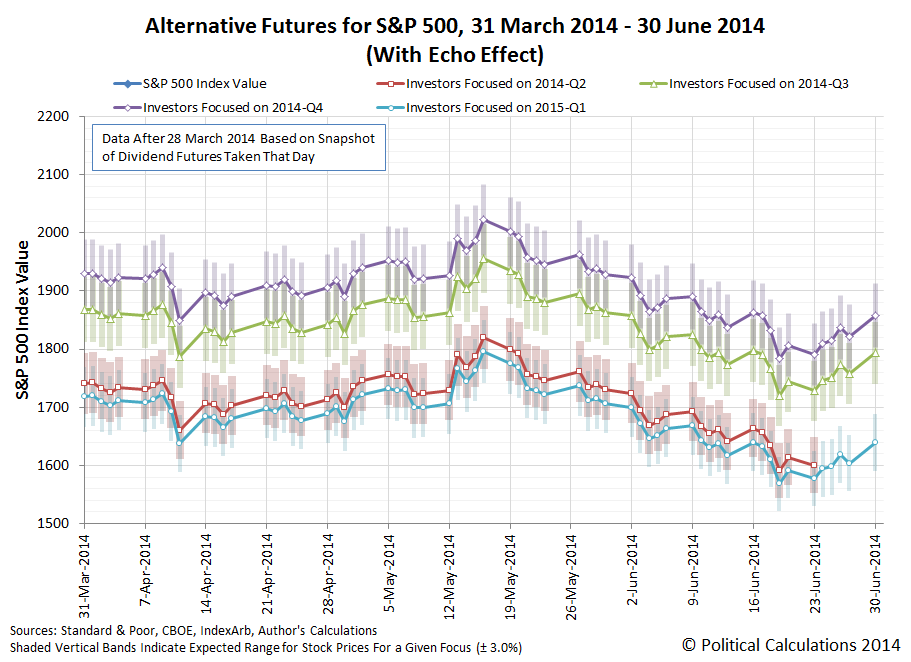

Here though, the events that set up the experiment occurred both one year and one month earlier, just as it did a month earlier in what we described as an aftershock event for the S&P 500. As you recall, our model of how stock prices behave anticipated the aftershock event of 10-11 April 2014 weeks before its arrival - the chart below shows what our model was projecting as of 28 March 2014:

Let's flash forward to last week, when we very uncharacteristically offered very little comment about the week as we focused instead upon setting up a proper state of nervous anxiety as we showed what our model was projecting as of 2 May 2014:

Comparing the projected future between these two charts, we see that prior to the arrival of the 10-11 April 2014 aftershock event, our model really only saw somewhat of a modest downturn covering the period from 9 May through 12 May 2014. But after the aftershock, our model, which incorporates the stock prices of one month ago and one year ago as key base reference points for making its projections of the future, shifted to indicate a sharper decline in stock prices, as the ripples of the previous aftershock event rippled forward in time.

Let's now look at the latest version of our alternative futures chart, showing what it projects as of 9 May 2014:

Clearly it's not playing out that way. Instead of an aftershock, our model is really projecting an echo. Noise from the past.

But wait - didn't we go to quite a lot of trouble to develop a method for filtering out that kind of thing from our model?

We did, but we only filtered the echoes from a year earlier in time - not the echoes from a month ago. We didn't make any adjustment for the echo effect in the short term, choosing instead to accept a larger degree of error in our projections than we might otherwise, which you see in our charts as the shaded vertical bars shown with respect to the midpoint of the likely range our model anticipates for stock prices for each of the alternative futures investors might focus upon as they set today's stock prices.

But should we account for the short-term echo effect? In our analysis of the 10-11 April 2014 aftershock event, we recognized a number of factors where events in the past could indeed create the potential for the outcomes we observe in the present to occur. If we filtered out the short term echo effect, our model might miss those episodes.

The answer then to the question we asked at the beginning of this post is that the degree to which events in the past might drive today's aftershocks or dissipate as yesterday's echoes would really appear to depend greatly upon what investors expect for the future as the maturity and option expiration dates associated with their previous investment choices come to pass and provide the means for executing new decisions.

And perhaps the best we can do in forecasting the future as these echoes develop into aftershocks or not is to simply acknowledge when a state of nervous anxiety on the part of investors is appropriate.

Once upon a time, the Internet was a really cool place to search out and learn useful information about the real world. Keep that in mind as David Tufte reveals a shocking discovery of what's lurking just a few pages of search results away from you are right now....

As best as we can tell, the Internet has degenerated into a massive electronic wasteland that is increasingly being overrun by cats. And Kardashians. And countless other empty distractions with precious little room to communicate useful information about real life unfolding in the real world in real time.You've probably heard about the mass kidnapping in Nigeria? (If not, Islamist terrorists raided a girls school, kidnapped a few hundred teenagers, and are threatening to sell them for … you know …).

This week there’s news that the Islamists may be hiding out in the Sambisa Forest.

This forest is a topic that is basically … not on Google. (I know, you thought everything was on the google these days). The linked article above is one of the few items with any content.

After some sleuthing I was able to find, what I think is this forest, on Google Maps. I circled it in red. The dark green with a little blue above it is what is left of Lake Chad — the big lake you always see on maps in the middle of the Sahara.

Anyway, the linked article says that the forest has huge crustaceans on the forest floor. That caught my eye: crustaceans in the Sahel?

So I went to Google and found … pretty much nothing about crustaceans in the Sambisa Forest. After a few minutes I concluded that English was not the primary language of the person who wrote the article. This makes me think that maybe they meant arthropod (millipedes) rather than crustaceans (crabs).

What does all this have to do with Kim Kardashian, the center of all media? It's that if you enter "sambisa forest crustacean" into Google, you get only 5 pages as the default response. Most of them are uninformative, but when you get to the 4th page, you find a link to this:

Kim Kardashian Shows Off Her Big b*tt in Sexy…

Hits like this start increasing. So Google has very little on the Sambisa Forest, but eventually you get to photos of Kim Kardashian's butt because she happened to go to an LA restaurant called Crustacean.

Go figure.

Labels: none really, technology

Welcome to the blogosphere's toolchest! Here, unlike other blogs dedicated to analyzing current events, we create easy-to-use, simple tools to do the math related to them so you can get in on the action too! If you would like to learn more about these tools, or if you would like to contribute ideas to develop for this blog, please e-mail us at:

ironman at politicalcalculations

Thanks in advance!

Closing values for previous trading day.

This site is primarily powered by:

CSS Validation

RSS Site Feed

JavaScript

The tools on this site are built using JavaScript. If you would like to learn more, one of the best free resources on the web is available at W3Schools.com.

Other Cool Resources

Blog Roll