From time to time, we'll conclude our more remarkable posts with the phrase "Welcome back to the cutting edge!" We're going to do that again today.

The reason we'll do that today is because of a new paper that was published just 20 days ago that describes cognitive decision making as the collapse of a quantum superstate. Phys.org's Christopher Packham provides the background for the application of "Quantum Random Walks" to decision making.

Decision making in an enormous range of tasks involves the accumulation of evidence in support of different hypotheses. One of the enduring models of evidence accumulation is the Markov random walk (MRW) theory, which assigns a probability to each hypothesis. In an MRW model of decision making, when deciding between two hypotheses, the cumulative evidence for and against each hypothesis reaches different levels at different times, moving particle-like from state to state and only occupying a single definite evidence level at any given point.

But the Markov random walk theory, based in classical probability theory, runs into problems when confronted with the emerging research consensus that preferences and beliefs are constructed, rather than revealed by judgments and decisions. An international group of psychological researchers now suggests a new model called the quantum random walk (QRW) theory that specifically posits that preferences and beliefs are constructed rather than revealed by judgments and decisions, and they have published the results of an experiment that support this theory in the Proceedings of the National Academy of Sciences.

By contrast with MRW, the new theory assumes that evidence develops over time in a superposition state analogous to the wave-like state of a photon, and judgements and decisions are made when this indefinite superposition state "collapses" into a definite state of evidence.

That new theory has a direct practical application, because it describes much of the behavior we've directly observed in how investors collectively set stock prices.

To see what we mean, let's update and animate alternative futures chart, which projects the likely trajectories that stock prices will follow based upon how far forward in time investors are collectively looking when they make their current day investment decisions, where we'll pick up the action beginning one month ago.

Each of the alternative future trajectories in the chart above represent a specific hypothesis, which is given by the acceleration, or change in the year over year growth rate, of the trailing year dividends per share expected to be paid out by the S&P 500 by the end of the indicated quarter.

At the beginning of the animation, we see that investors were tightly focused on 2015-Q3 on 29 July 2015, which makes sense because investors had strong reason to believe that the U.S. Federal Reserve was on track to begin hiking short term interest rates by the end of the quarter in September 2015, thanks to the Federal Open Market Committee's meeting and announcement issued that day. Thus, the trajectory indicated for 2015-Q3 represents the hypothesis that the Federal Reserve would hold to that policy.

Over the next week, the closing value of the S&P 500 closely tracked that trajectory, until moving higher on Monday, 10 August 2015, boosted by the speculative prospect that China, which announced disappointing economic data that day, would soon act to provide new stimulus measures for that nation's economy.

Stock prices remained elevated throughout the rest of that week as China made good on that speculation, as it announced the surprise devaluation of its currency on 11 August 2015 and by other measures that carried through 17 August 2015. Throughout this period, stock prices remained elevated just above the upper edge of the typical range of day-to-day volatility of stock prices that we would expect would apply for investors remaining focused on 2015-Q3.

That positive speculation began to deflate on 18 August 2015 as China's stock market began to decline, as China's government began to back off from enforcing its previous extraordinary measures to arrest its decline earlier in the summer.

That action also coincided with the two-year anniversary of the so-called "taper tantrum" in the U.S. stock and bond markets, which would appear to be relevant since we used historical stock prices from this period as the baseline from which to project the likely trajectories shown in our chart above. Which we began doing on 28 July 2015 because the period was much less volatile that the one-year ago period that we would normally use to forecast the future likely trajectories of stock prices in our standard model of how stock prices work.

What happened next is now the stuff of forecasting legend. Based on the echo of that two-year old event, our model anticipated that stock prices would begin falling, even if investors remained focused on 2015-Q3 in setting stock prices. And through the week ending 21 August 2015, the level of stock prices was fully consistent with investors remaining focused on 2015-Q3.

But then, on Monday, 24 August 2015, stock prices closed far lower than would be consistent with investors remaining focused on 2015-Q3 alone. Instead, stock prices plunged to a level that was much more heavily weighted toward 2016-Q1, which would be consistent with the hypothesis that the Federal Reserve would back off its plans to hike short term interest rates in the U.S. until that time at the earliest based on the continuing deterioration in China's stock markets.

On Tuesday, 26 August 2015, a sizeable rally in the U.S. stock market throughout much of that day "went up in smoke", as stock prices closed that day at a level that was fully consistent with investors having shifted their forward looking focus to 2016-Q1, in effect, collectively betting that a September 2015 rate hike in the U.S. would now be off the table. Coincidentally that day, Federal Reserve Bank of New York president William Dudley said that a September 2015 rate hike was "less compelling".

The downward swinging pendulum of investor expectations for when the Fed would seek to hike interest rates reversed on the next day with the release of positive economic news, giving more strength to the hypothesis that the Fed would hike rates in 2015-Q3. Overall however, stock prices moved to be about halfway between the levels that would be fully consistent with either 2015-Q3 and 2016-Q1, suggesting that investors gave equal weighting to the difference between these two future quarters in setting stock prices.

The positive momentum continued on 27 August 2015, with the significant upward revision of U.S. GDP recorded in the second quarter of 2015. That news strengthened the view among U.S. investors that the Fed would hold to its September rate hike plans, with the S&P 500 closing in on a level that would be more heavily weighted in favor of that hypothesis.

On Friday, 28 August 2015, there was very little movement in stock prices, but that would be expected for investors having focused once more on the likelihood that the Fed would indeed hike interest rates in September 2015, a view given great emphasis during the day by Stanley Fischer, the Number Two official at the U.S. Federal Reserve.

There are four things we really need to point out about the movement of stock prices during the period from the close of trading on 21 August 2015 through 28 August 2015. First, the concept of a quantum random walk goes a very long way toward explaining why stock prices just simply don't jump straight from one quantum level to another. The uncertainty that investors have regarding the likelihood of future events can restrain the potential extent of such movements.

Second, the quantum levels themselves are not random. They're based on the real and quantifiable expectations for the change in the growth rate of dividends per share that will be paid out at specific points of time in the future, which are projected on top of where stock prices are and have been. That's important because it is the relative distance between the quantum levels that exist when investors are choosing between the hypotheses that apply at different points of time in the future that determines whether stock prices follow a true random walk-style Brownian Motion, or go into a full Lévy Flight such as we observed in the last week.

Third, as stock prices change, so does the likely trajectory of stock prices in the future. Given the math involved, we now see the echo of the China-driven stock market crash in September in our animated chart above.

However, that doesn't mean that stock prices will follow that trajectory. In general, the echoes of past volatility do not tend to affect the trajectory of current day stock prices, although in rare cases, they can. What provides the potential for determining whether they might is the amount of money that might have been tied up in investments with fixed maturity dates, such as options contracts or bonds, which would come due when such echoes appear in our model.

But whether they do have any real world impact depends on what the investment climate looks like when they do come due. It is always the prospects for the future that determine the actual trajectory of stock prices.

Fourth, the existence of the quantum random walk phenomenon helps explain why stock returns have fat tail distributions. To the extent those distributions primarily resemble bell curves is an indication of the extent to which investors collectively tend to focus on one potential future, or investment-driving hypothesis, at a time as they make investing decisions.

Welcome back to the cutting edge!

Previously on Political Calculations

- Emerging Order in the Stock Market - 12 June 2008

- Acceleration, Amplification and Shifting Time - 10 December 2008

- The Math Behind How Stock Prices Work - 23 April 2009

- Playing the S&P 500's Wild Cards - 6 May 2013

- S&P 500: Odds Suggest Schrödinger's Cat Is Three Quarters Dead - 3 September 2013

- Completing a Quantum Shift in Future Expectations - 30 January 2014

- A Better Frame of Reference, Mean Reversion and the S&P 500 - 18 March 2014

- Taking the Fork in the S&P 500's Future - 1 August 2014

- Quantifying Stock Price Volatility - 13 July 2015

- Decoherent Expectations and the S&P 500 - 22 June 2015

- What We Do, Explained by Others - 6 July 2015

- Order Breaks Down in S&P 500, As Expected - 21 August 2015

Labels: chaos, data visualization, SP 500

Three weeks ago, we featured the work of the young Australian behind the Primitive Technology blog, who built a stone adze from scratch in the wild, which he then proceeded to use to build a primitive, yet effective and durable shelter from his surrounding materials.

As human invention goes, the adze is a contemporary of the axe, another tool that first saw the light of day in the stone age.

Today, we're going to feature the modern reinvention of the axe, in which the millenia-old design is being revisited by Finnish inventor Heikki Kärnä to make it a more effective tool, funding for the development of which is now being sought via Kickstarter. Meet the Leveraxe:

We love the quote from Business Insider regarding the invention:

This weird, super-efficient axe solves an engineering problem most people don't even know exists.

Which explains why we're helping to spread the word. For anyone who has ever had or will have a need to split wood logs, this design looks to have an edge up over its traditional axe competition.

Labels: technology

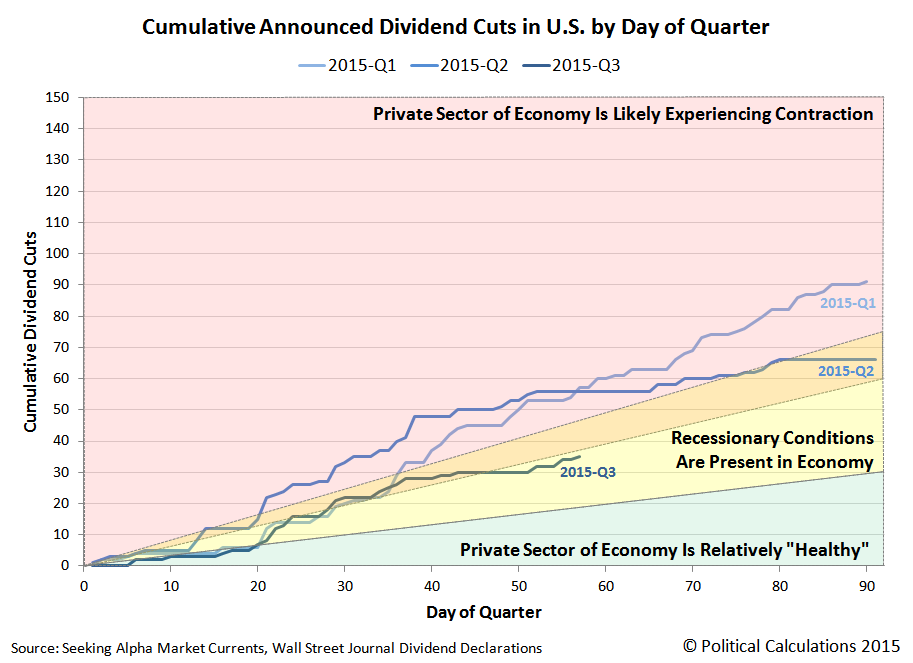

Believe it or not, August is shaping up to be the second best month for dividends in 2015.

But don't take our word for it - the proof is in our near-real time measure of the level of distress in the U.S. economy, the cumulative number of U.S. firms announcing that they are cutting their cash dividend payments to their shareholder owners by day of the quarter.

The best month of 2015 was June 2015, which only saw 10 firms cut their dividends according to Seeking Alpha's Market Currents and the Wall Street Journal's daily listing of dividend declarations. At 13 (and counting since the month hasn't run out of trading days yet), it is unlikely that the total for August 2015 will surpass the next-highest total of 21, which was recorded in January 2015.

Still, any figure over 10 is consistent with recessionary conditions being present in the U.S. economy, although the reduction in the number of firms announcing dividend cuts below levels that are consistent with contraction occurring in the U.S. economy is a positive development.

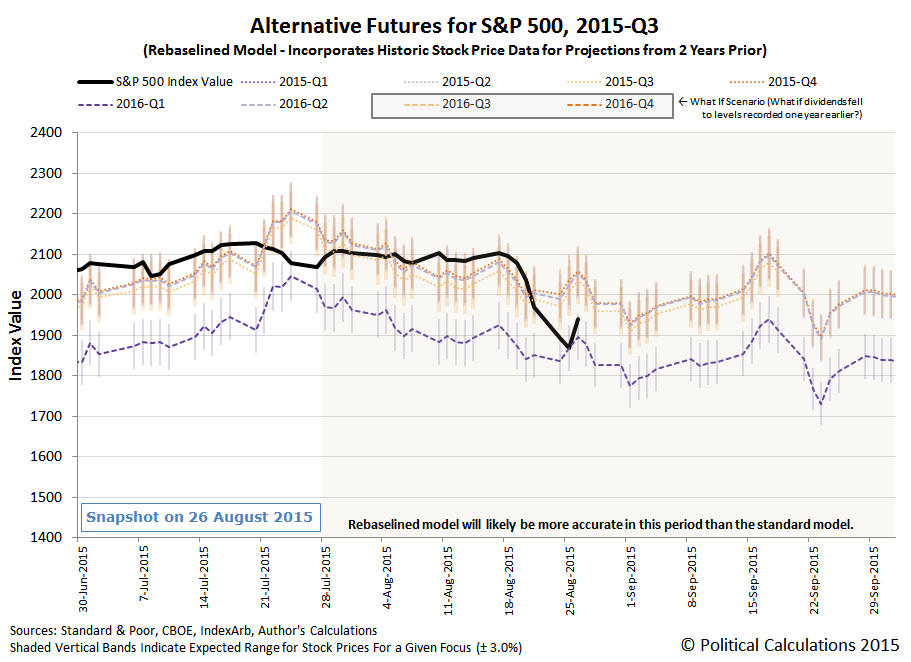

And since 26 August 2015 qualifies as what we would consider to be an interesting day for the stock market, here's the latest update to our alternative futures chart, where it you can predict how far ahead in time investors are focusing their attention, you can anticipate within a relatively narrow margin of where stock prices will go next.

Even with closing up by 72.90 points, the third best trading day ever for the S&P 500 in terms of the point difference from the previous day's closing value, investors would appear to remain focused on 2016-Q1 in setting today's stock prices. Keeping in mind that we're referring to the dividend futures contract that will come into effect after the third Friday of December 2015, which means it covers dividends that will be paid out at the end of the current calendar year through the third Friday in March 2016, that very recent shift in focus is not a good one for investors looking for positive returns.

In our updated chart above, we've begun projecting the impact from the shock wave left behind by the extraordinary market activity of the past week into the future, much of which is a consequence of the event's effect upon the nation's bond markets. Speaking of which, that's a major factor in how we were able to accurately forecast the onset of the event, a good portion of which was embedded into the future of the stock market because of what happened exactly two years ago.

Meanwhile, behind the scenes, we've peered ahead in time through the end of the year, but we're going to hold off on commenting on what we've seen until this initial shock has dissippated to a greater extent and we have a better idea of what the impact crater it is leaving behind will look like.

Data Sources

Seeking Alpha Market Currents. Filtered for Dividends. [Online Database]. Accessed 26 August 2015.

Wall Street Journal. Dividend Declarations. [Online Database]. Accessed 26 August 2015.

Labels: chaos, dividends, SP 500

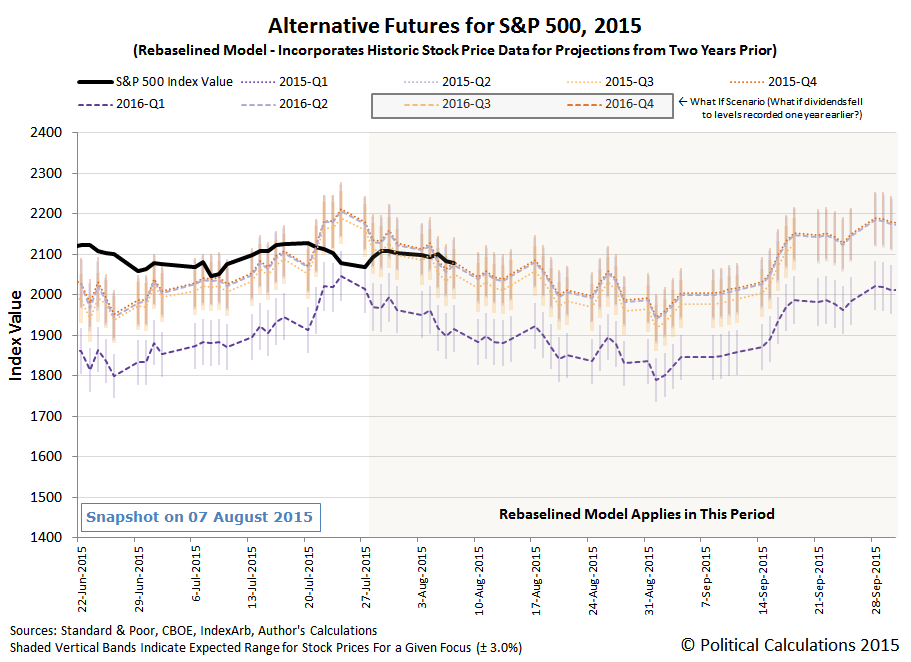

Based on the outcome of the remarkable volatility of trading in the U.S. stock market on 25 August 2015, our rebaselined model of how stock prices work would say that investors are now fully focused on the first quarter of 2016 as they go about setting stock prices.

Just remember, it could be worse. If certain large market-cap weighted firms were to start announcing dividend cuts, then the expected future, and stock prices, will turn south. But don't worry - that likely won't happen until the next earnings season gets underway in October....

Every three months, we take a snapshot of the expectations for future earnings in the S&P 500 at approximately the midpoint of the current quarter. Today, we'll confirm that the earnings recession that began in the fourth quarter of 2014 has continued to deepen.

In the chart above, we confirm that the trailing twelve month earnings per share for the S&P 500 throughout 2015 has continued to fall from the levels that Standard and Poor had projected they would be back in May 2015. And for that matter, what S&P forecast they would be back in February 2015 and in November 2014.

Looking at year over year changes for the recently completed second quarter of 2015, the biggest decline in quarterly earnings per share from 2014-Q2 has been in the energy sector (-113.1%), followed by the materials (-22.5%) and information technology (-16.4%) sectors. There have also been smaller declines in telecommunication services (-9%), industrials (-3.7%), consumer staples (-3%) and health care (-1.7%).

Three economic sectors showed positive year over year changes in their quarterly earning per share figures: utilities (+15.2%), financials (+10.5%) and consumer discretionary (+10%).

Data Source

Silverblatt, Howard. S&P Indices Market Attribute Series. S&P 500 Monthly Performance Data. S&P 500 Earnings and Estimate Report. [Excel Spreadsheet]. Last Updated 20 August 2015. Accessed 20 August 2015.

Labels: earnings, forecasting, SP 500

A little over two years ago, the suggestion that Larry Summers was likely to be appointed to be put in charge of the Federal Reserve was enough to make the stock market swoon.

Fortunately, that never happened, but yesterday, Larry Summers may very well have had his revenge, thanks to the coincidental timing of his op-ed in the Washington Post, in which he encouraged Fed officials to back off their established plan to hike short-term U.S. interest rates in September 2015 (emphasis ours):

Federal Reserve officials have held out the prospect that at long last they may raise interest rates at their September meeting, with the hike taking effect by year’s end barring major unforeseen developments. A reasonable assessment of current conditions suggests that raising rates in the near future would be a serious error that would threaten all three of the Fed’s major objectives: price stability, full employment and financial stability.

Although Summers has chronically read the market situation incorrectly over the last several years, his viewpoint is still important because it reflects the way that a significant number of influential people think. Such as the people who have been nominated to the U.S. Federal Reserve over the last 20 years, who might as well all march to the same drumbeat.

Because of that factor, and because of the increasing pressure that the Fed is now coming under to avoid taking its long-planned action, stock prices fell far more on Monday, 24 August 2015 than they might otherwise have if investors believed that the Fed would hold to its plans to announce it will hike rates almost three and a half weeks from now.

The reason that investors are making that call now is because they anticipate that the situation for the U.S. economy will be worse going forward than the data the Fed has claimed it is dependent upon for making its plans has indicated to date.

Believe it or not, that's good news for the Fed should stock prices continue to decline this week. Since the current worst-case potential bottom for the market is defined by the expectations for the change in the year over year growth rate of dividends per share that will be paid out in the first quarter of 2016, which would be the quarter that investors are now most likely now factoring into their outlook, the Fed won't have to engage in any extraordinary measures like quantitative easing to prop up the U.S. economy unless and until the economic situation clearly deteriorates significantly beyond that level.

That matters because the one thing that the Fed officials would really rather not do is to load up its balance sheet by initiating a another new round of quantitative easing. Especially if the nation's economy is really performing as well as the data they follow indicates.

So what should the Fed do? We would suggest that the Fed do nothing, but in a creative way. The Fed should announce that it will indeed hike short term interest rates as planned in September 2015, and at the same time, that it will also initiate a new round of quantitative easing, initially at a low value with the amount being data dependent with respect to actual economic conditions within the U.S. economy, with the stated goal of achieving a nominal GDP growth rate target it believes it can attain by the second quarter of 2016.

These two actions would arrest the decline of U.S. stock prices by focusing investors on the more positive expectations associated with these two quarters, while at the same time doing nothing, as the new QE initiative would offset the perceived tightening of monetary policy from the interest rate hike.

Then, if the Fed really wanted to get some stimulative power going that would allow them to both raise interest rates and to successfully terminate their quantitative easing program once and for all, they should announce that they will terminate their new QE program by the end of 2016-Q2 unless the nation's tax rates and regulatory burdens on economic activities are reduced by that time, with the goal of generating real economic growth with minimal economic distortions.

With the large positive impact that tax cuts have on economic growth through the multiplier effect, and by committing to continue its new QE program until the benefits take hold, the Fed would create its desired environment where it would be able to both raise interest rates and terminate its QE program.

What's the point of being the U.S. economy's 800 pound gorilla if you don't periodically act the role? And as the U.S. government's most powerful creditor, it has the leverage it needs to achieve those goals by forcing positive changes in the federal government's fiscal policies.

In the Wings

We bumped our publishing schedule this week to accommodate the rather remarkable market activity today, including a look at how the U.S. stock market is signaling that its earnings recession has significantly deepened over the last three months, which we'll now feature on Wednesday, 25 August 2015. On Thursday, we'll update our primary indicator of the relative health of the U.S. economy, the number of companies announcing dividend cuts, where we'll show that the economy through this point in August 2015 is doing the best it has all year long.

It's not your imagination. The stock market really is sending very mixed signals at present.

And then on Friday, we'll change gears, unless something interesting happens with the stock market between now and then. As a general rule of thumb, we don't find the daily action of the stock market interesting unless it changes by more than 2% of its previous day's closing value.

Until then, by request, here's an update of our "broken order" chart showing, well, that order has broken down in the U.S. stock market:

That's definitely no outlier!

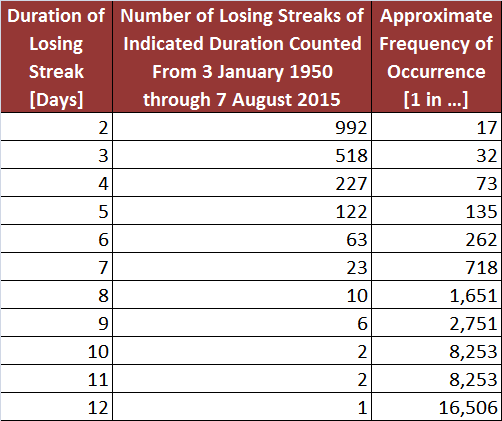

Plus, as a bonus, here are our calculated odds of a losing streak in the S&P 500 for each potential duration for which we have the data:

The longest losing streak on record for the S&P 500 is 12 days. In the last 65 and a half years, there has only been one losing streak that ran that long....

USA Today's Matt Krantz considered an interesting premise at 4:59 PM EDT on 21 August 2015, just after the Dow Jones Industrial average lost 531 points and the S&P 500 lost 65: "How low the stock market can go".

After seeing 6% of their money evaporate this week to drop 8% from the recent highs- investors are wondering how much uglier things can get. The answer is: much.

The Standard & Poor's 500 fell another 3.2% Friday - dragging the index down below 2000 at 1970.89. Seeing such a rapid decline is a reminder this bull market has gone untested for too long and the pain could get worse - much worse to bring valuations back in line with reality.

"There will be more wringing out of this market. There's been too much optimism," says Chris Johnson of JK Investment Group.

Trying to guess how low a market under pressure can go is far from precise. Markets can overshoot on the downside just as they can soar too much on the upside.

Considering that we're the probably the only analysts who appear to have successfully foreseen the specific market action of the trading week ending 21 August 2015, well in advance, we have some insights that might be relevant to consider on how much lower stock prices might go.

Let's first consider the immediate situation, in which the U.S. stock market has racked up a 4-day long losing streak. Based on 16,506 days worrth of historical data from 3 January 1950 through 7 August 2015, the odds were approximately 1 in 73 going into the previous week that such a long losing streak would be recorded.

Meanwhile, the odds that the market will see a 5-day long losing streak are roughly 1 in 135. Based on these figures, the probability that the U.S. stock market will extend its current 4-day losing streak to 5 days is about 46%. So the odds slightly favor the immediate losing streak coming to an end.

But that assumes some degree of general randomness in stock prices, which as we've long since established, is a relatively limited factor in driving stock prices, with its main channel affecting their day-to-day volatility through the interactions of millions of investors conducting billions of transactions.

Since they're not really random, but are instead driven by the expectations that investors have for the changes they expect in the growth rate of the dividends per share they can reasonably expect to earn at specific points of time in the future, let's take a look at what likely lies ahead.

At present, investors would appear to remain focused on the expectations associated with the current quarter, 2015-Q3, which will end in September 2015. This focus has largely been directed by the forward guidance that the Federal Reserve has steadily been providing with respect to its plans to begin hiking short term interest rates over the last several months.

With that being the case, so long as U.S. investors remain focused on the current quarter, we can reasonably expect that stock prices will generally parallel the trajectory indicated in the chart above, within a relatively narrow margin of error as consistent with the typical day-to-day volatility of stock prices.

Given the relatively narrow difference between the alternative future forecasts that apply for when investors might be focused on either 2015-Q3, 2015-Q4 or 2016-Q2, we would anticipate that stock prices are likely within about 3% of where they will bottom in the near term. However, should investors shift their forward-looking focus to 2016-Q1, as might happen if investors adopted the view that the global economic situation is such that the U.S. Federal Reserve will back off its plan to begin hiking short term U.S. interest rates in September 2015, stock prices would likely fall an additional 6-9%.

There are however two wild cards to consider. First, should the expectations for future dividends deteriorate, such as might happen if major U.S. oil producers act to cut their cash dividends in response to declining revenues resulting from falling global crude oil prices, stock prices will fall below the levels indicated in the charts above as the basic fundamental factor that drives stock prices will have been negatively impacted.

Second, a significant noise event could cause stock prices to deviate from the likely trajectories shown in our alternative futures forecast chart above. As these kinds of events are largely driven by speculation in the market in reaction to the random onset of real world news events, which is the other channel by which stock prices are affected by random factors. Although transitory in nature, such noise events can significantly affect the level of stock prices until they dissipate.

If you were looking for absolute certainty about where the market is going, you came to the wrong place. If however you were simply looking to get a better handle on what is happening within the U.S. stock market for the sake of making better informed investment decisions as global markets go through a period of panic, you're welcome.

Labels: chaos, forecasting, SP 500

On 20 August 2015, the period of order that had existed in the U.S. stock market since 4 August 2011 broke down. Statistically speaking that is!

Of course, that outcome should come as no surprise to our readers. Speaking of which, the animated image below compares our forecast chart that we previously featured back on 3 August 2015 and again on 10 August 2015 with what the most recent version of the chart looks like today.

Stock prices are, after all, just a simple quantum kinematics problem, where all you have to know to anticipate where they're going is approximately how far forward in time that investors are looking, their future expectations for dividends at that future point of time, where stock prices were previously, and the typical volatility for daily stock prices!...

Doing all that is, as we like to say, complex, but not difficult. Especially with nearly optimal conditions for this kind of forecasting.

Labels: chaos, forecasting, SP 500

Economist Paul Romer recently made waves in his profession after he recognized the increasing use of misleading math by others in his profession, most often in the attempt to pursue a political or ideological agenda, has gotten to the point where it is obstructing progress in the field.

In doing so, he introduced the concept of "mathiness", which the Wall Street Journal summarized as follows:

In his paper, “Mathiness in the Theory of Economic Growth,” he described how “mathiness uses a mixture of words and symbols, but instead of making tight links, it leaves ample room for slippage.” If this sloppiness or even intellectual dishonesty continues, he warns, mathematical models will lose their explanatory and descriptive power. Instead, he writes, “Presenting a model is like doing a card trick. Everybody knows there will be some sleight of hand.”

How can we cut through the sleight of hand? Marianne Freiberger recently explored why proofs matter so much to mathematicians, but the arguments directly apply to economic analysis, and point to how increased challenges to politically-motivated flawed reasoning to get to the real truth:

In everyday life, when we're not just being completely irrational, we generally use two forms of reasoning. One of them, called inductive reasoning, involves drawing a general conclusion from what we see around us. For example, if all the sheep you have ever seen were white, you might conclude that all sheep are white. This form of reasoning is very useful — scientists form their theories based on the observations they make in a similar way — but it's not water tight. Since you can't be sure that you have seen every single sheep in the Universe, you can never be sure that there isn't a black one hiding somewhere, so you can't be sure your conclusion is really true. If you use inductive reasoning, you have to be open to revising your conclusion when new evidence comes to light, and that's what scientists generally do.

The other form of reasoning, called deductive reasoning, goes the other way around. You start from a general statement you know for sure is true and draw conclusions about a specific case. For example, if you know for a fact that all sheep like to eat grass, and you also know that the creature standing in front of you is a sheep, then you know with certainty that it likes grass. This form of reasoning is water tight. It can only go wrong if your premise is false, that is if you're wrong about all sheep liking grass, or if your observation is wrong, that is, the creature you're looking at is not actually a sheep. But if those two things are correct, then your conclusion follows necessarily from your premise: it is true everywhere and for eternity....

Mathematics is perhaps the only field in which absolute certainty is possible, which is why mathematicians hold proofs so dearly. Also, if we don't insist on proofs, mistakes can creep in that aren't easily spotted otherwise.

How might that be done in economics? We would suggest that the three imperatives, or rather, "economics in 10 words", that Peter Gordon uses to introduce economics to new students might provide an effective starting point for challenging those economists whose misuse of math and use of misleading data discredit both themselves and their profession:

Many econ professors know that some students only pay attention for the first few minutes of any course. So, some immediately tell them that it all boils down to three imperatives (ten little words). 1) at what cost? 2) compared to what? and 3) how do you know?

We think that it will be the "compared to what" and "how do you know" parts of those three imperatives that will most often trip up the deliberately deceptive economist. And to that end, we can apply our checklist for how to detect junk science for going about challenging the flawed work of such politically or ideologically-driven hacks.

The bad news is that we suspect that the people most likely to be engaged in that kind of misconduct will also tend to be highly unpleasant people, who may in fact be "completely irrational", to borrow Marianne Freiberger's phrasing.

On the other hand, it might be instructive to see how far such people are willing to go to deny reality to preserve their agenda.

Image Credit: Scoopnest.

Earlier this year, we broke the news that the Apollo Education Group (NASDAQ: APOL), the parent company of the University of Phoenix, had suffered a major setback with respect to its strategic plan to become a major provider of educational software.

The setback is related to the Adaptive Math Practice instruction software that was developed by the Apollo Group's Carnegie Learning division, which is based upon its Cognitive Tutor software.

The University of Phoenix had implemented the software to support its math classes beginning in October 2013, and quickly ran into costly technical problems in using it. On 27 February 2015, Constance St. Germain, the executive dean of the University of Phoenix's College of Humanities and Sciences, sent out an e-mail (download PDF document), in which she announced that the University of Phoenix had begun the process of terminating the use of Carnegie Learning's Adaptive Math Practice system in the University of Phoenix' math courses after those technical problems proved to be too costly and insurmountable.

The e-mail described the benefits of no longer using the Carnegie Learning-developed software in describing the transition plans away from it, which had begun in January 2015:

In January, we began transitioning from Adaptive Math Practice (AMP) to My Math Lab (MML) with two courses: MTH/208 (in January) and MTH/209 (in February). This decision was made primarily due to all of your valuable feedback from Content Area Meetings, SEOCS, FEOCS, and personal emails.

Thus far, the results have been very positive, including drastically reduced technical support tickets.

In replacing Carnegie Learning's Adaptive Math Practice software with Pearson Education's My Math Lab product, the University of Phoenix is sending the market a very clear message about the value it places on the products developed by its sister division within the Apollo Group.

That setback for the Apollo Group's strategic plans with respect to becoming a developer and provider of advanced education software products were indirectly referenced during the company's 2015-Q3 Results Earnings Conference Call, during which Apollo Group CEO Greg Capelli made the following statement:

We plan to move away from certain proprietary and legacy IT systems to more efficiently meet student and organizational needs over time. This means transitioning an increased portion of our technology portfolio to commercial software providers, allowing us to focus more of our time and investment on educating and student outcomes. While Apollo was among the first to design an online classroom and supporting system, in today's world it's simply not as efficient to continue to support complicated, custom-designed systems particularly with the newer quality systems we have more recently found with of the self providers that now exist within the marketplace. This is expected to reduce costs over the long term, increase operational efficiency and effectiveness while still very much supporting a strong student experience.

What Apollo Group CEO Greg Capelli describes here is directly in line with the actions announced by University of Phoenix executive dean Constance St. Germain earlier in the year - the Apollo Group sees no advantage in sustaining its own proprietary education software at its academic institutions.

That means that the Apollo Group's Carnegie Learning division and its products are now effectively "damaged goods". And that's a problem for the company because the apparent change in strategic direction for the company means that they're not just trying to sell Carnegie Learning's products, but are likely also trying to sell Carnegie Learning as well.

This is not to say that all of Carnegie Learning's products are completely worthless. The U.S. Department of Education's Institute of Education Sciences reports that it has had mixed results with Carnegie Learning's Cognitive Tutor system with respect to mathematics achievement for high school students, while that software has also been recently approved for use in Texas and Florida high schools.

Beyond that, Carnegie Learning recently marketed its products at a June 2015 conference in Spain, which suggests that it sees opportunities in foreign education markets.

But in terms of making sales, Carnegie Learning's sister divisions within the Apollo Group have made that task much more difficult as the failure of Carnegie Learning's Adaptive Math Practice system to be successfully implemented at the University of Phoenix represents a major strike against the division and its products.

The Apollo Group had acquired Carnegie Learning for $75 million in September 2011. The acquisition was an integral part of the Apollo Group's billion dollar bet on its development of an adaptive learning platform, part of its internally developed "Learning Genome Project", in which it would seek to personalize the learning experience of the students enrolled in its classes, which it was counting upon to preserve and build its student enrollment.

That is increasingly looking like a billion dollar bet gone bad.

Labels: business, education, quality

Now that we've quantified all of the streaks of two-or-more consecutive days in which the S&P 500 was either up or down for every trading day since 3 January 1950, it's time to do something with the results of our deep data dive.

So we've taken the math we generated and built the following tool, in which you only need to enter the duration of a particular streak. We'll calculate the odds of a streak that long occurring, the odds of it being either a winning streak (multiple consecutive up days) or a losing streak (multiple consecutive down days), and also the odds of the streak lasting just one more day!

It all begins below. If you're accessing this tool on a site that republishes our RSS news feed, just click through to our site to access a working version....

So, if a streak in the S&P 500 is underway and you're a speculator, the question is: do you feel lucky?

Well, do you?

Labels: investing, probability, SP 500, stock market, tool

After a rough July, in which the number of U.S. firms announcing dividend cuts directly paced what we saw during the first quarter of 2015, it would appear that the U.S. economy in August is shaping up to be much less severe. Our near real time indicator of the relative level of economic distress in the U.S. economy is now suggesting only that recessionary conditions are present in the U.S. economy in August 2015, rather than the kind of contraction that we observed in the near-zero growth of first quarter.

But instead of being a cause for celebration, we have to address a significant and growing cause for concern. The main thing that drove the heightened level of distress in the U.S. economy back in 2015-Q1 was the fall of crude oil prices below $50 per barrel, which primarily hammered small-to-mid-sized U.S. oil producers, many of whom responded by slashing their cash dividend payments to their shareholder owners, while they also slashed their plans for expansion, which in turn, negatively affected things like durable goods providers.

Those negative conditions abated during the second quarter of 2015 as crude oil prices stabilized, but over the past month, crude oil prices have once again resumed their significant decline, with the price of West Texas Intermediate crude oil falling by almost 20% since mid-July 2015.

As we saw back in January 2015, the number of dividend cut announcements for U.S. oil and gas extraction firms lagged behind the declines in price that had begun soon after 4 July 2014. We think that if the decline is not reversed, whether by an improvement in the oil industry's overall fundamentals or the devaluation of the U.S. dollar, it is likely that the level of distress in this sector of the U.S. economy will once again increase, forcing an increased number of firms to cut their dividends.

The big question for investors is how long can oil prices continue falling or remain depressed below their previous levels before the level of distress in the industry expands to its largest producers. Already, the decline in oil prices is negatively impacting the earnings of firms such as Exxon Mobil (NYSE: XOM) and Chevron (NYSE: CVX), who are already on track to reduce their new exploration and production operations.

With the decline in oil prices to date, Exxon Mobil has already fallen from being the largest component by market capitalization in the S&P 500 to now be the index' third largest firm, while Chevron has dropped out of the S&P 500's Top 20 component firms altogether. Even so reduced, should these firms act to cut their dividends, the effect will be felt across the entire index.

So we're left with the question of whether what we're seeing now is a growing level of calm in the U.S. economy and stock market, or is what we're seeing now just the calm before the storm hits?

Data Sources

Seeking Alpha Market Currents. Filtered for Dividends. [Online Database]. Accessed 15 August 2015.

Wall Street Journal. Dividend Declarations. [Online Database]. Accessed 15 August 2015.

Labels: dividends, SP 500, stock market

Bill Hammack, the engineerguy, explains why 5% faster really wasn't good enough for the Dvorak keyboard to unthrone the QWERTY keyboard in the battle to be the dominant letter key layout for typing by hand....

And speaking of the role of new technology in driving new ways to do things, like texting on a mobile phone, there still hasn't been a major advance to really push the old QWERTY keyboard layout into the dustbin of history, where promising innovations such as Swype, Swiftkey, ai.type, Fleksy and our aesthetic favorite, Minuum actually build upon.

Time will tell which was the winner.

Labels: technology

Since we counted up all of the S&P 500's losing streaks by their duration earlier this week, we thought we'd follow up and repeat the exercise for all the S&P 500's winning streaks before the week ended. The chart below shows our results:

We find that while the number of two-day-long winning streaks is lower than the number of two-day-long losing streaks, once we get to streaks of three days or longer, the number of winning streaks outnumber the numbers of losing streaks for each duration.

Not only that, we find that the longest winning streak of 14 consecutive trading days for the S&P 500, which ran from 26 March 1971 through 15 April 1971, is longer than the longest losing streak, which ended after 12 consecutive down days for the index.

Digging into the history of the market of that time, we didn't find any evidence of a change in the Federal Reserve's monetary policy influencing the expectations that drive stock prices at that time, although we will note that just seven days earlier on 19 March 1971, Fed Chair Arthur F. Burns met with President Richard Nixon in the White House, where the President first broached the topic of having the Federal Reserve act to manipulate the U.S. economy to the President's favor in the upcoming 1972 election year. However, although Burns was predisposed to be loyal to President Nixon, it wouldn't be until Fall 1971 that the Fed would really go all out to "goose" the economy by pushing down interest rates below their natural rate a year ahead of the national elections in 1972.

Instead, we think the best explanation for the longest ever recorded winning streak for the S&P 500 had a lot more to do with interest rates hitting a low point during the mid-March to mid-April 1971 time frame, after which they quickly rebounded back up to the levels at which they had started the year.

As for the Fed's stimulative actions, they achieved the desired effect as President Nixon sailed to re-election. But with one really nasty side effect, as it initated the massive inflation that characterized the rest of the 1970s. And though it did help provide a short term positive boost to U.S. stock prices, it couldn't be sustained and where stock prices were concerned, the 1970s was, on the whole, a period of stagnation.

Labels: data visualization, SP 500, stock market

Going by the level of carbon dioxide measured in the Earth's atmosphere in July 2015, it appears that Earth's economy continued its recessionary cooling in July 2015, with the trailing year moving average of the year over year change in the CO2 levels ticking up to be just barely above its June level. Not uncoincidentally, Earth's largest producer of atmospheric carbon dioxide, China, saw its national economy continue to sputter during the month.

The world's economy has been cooling right along with the deceleration in the pace at which carbon dioxide levels in the Earth's atmosphere have been increasing, which began after China's political leadership held their third "plenum", or leadership meeting, in which they committed to a plan to put the nation's economy on a "sustainable growth path" after years of strong economic growth. Since that meeting, China's leaders have been steadily redirecting resources away from supporting the expansion of the nation's low-cost export driven industries to instead favor the expansion of service-oriented enterprises, with the goal of transforming China's economy to be primarily driven by domestic consumer demand.

So at least what we're observing isn't happening by accident.

Analyst Notes

Picking up on our previous hypothesis, we're pleased to announce that we were wrong!

What we're referring to specifically is our effort to fill in more of the world's economic history to correlate where decelerations in global atmospheric CO2 levels had occurred, where we had hypothesized that the Cuban Missle Crisis of October 1962 may have led to sanctions or other negative economic events that occurred in many of the world's communist, socialist and progressive regimes, which are notorious for covering up their failings.

Using historical data from on territorial carbon production from the Global Carbon Project, we found evidence that the territory of Russia saw significant increases in the millions of tons of carbon it burned during the period of interest from 1962 through 1965, which ruled out that possibility.

We also observed that China's own carbon emissons were stagnant from 1963 through 1964, after having plummetted in the preceding two years. Since this is annual data, it occurred to us that China really bottomed in 1962 and was very slow to recover from its failed Great Leap Forward initiative and the famine it produced.

It then occurred to us to consider another possibility. Even though China's GDP is believed to have grown in 1963 and 1964, we wondered if perhaps another economic and CO2-producing heavy hitter, the United States, also recorded positive economic growth during the period in question, but perhaps in a less-than-stellar economic environment.

So we tapped Jon Gregory Taylor's work on Investment Timing and the Business Cycle to find out if any of the observed decelerations in global CO2 levels were correlated with downturns in the U.S. business cycle.

Oh yes, they mostly were! Those results are represented in our chart above, as the light red shaded vertical bands.

The results aren't perfect, but that perhaps might be attributed to the relative severity of the U.S. business cycle downturns. For example, while a severe downturn might be expected to have a negative impact on global CO2 measurements, a very mild downturn might only have a very mild, or muted effect - say only slowing the rate at which CO2 levels increased, rather that correlating to an outright decrease in them, as we often observe during official periods of recession.

Taylor's data on U.S. business cycle downturns only covers the period through December 1995. In our next update, we'll see if we can't flesh out more of the period from 1996 onward.

Labels: data visualization, environment, recession

We learned long ago that trade data published by the Chinese government is almost completely unreliable for anything other than indicating its economy's basic direction.

So we don't rely upon it, as we discovered that the trade data published by the U.S. government about the goods that the U.S. imports from and exports to China is considerably more reliable. Given the volume of trade between the two nations, that data makes for a more accurate indicator of the relative health of China's economy than using China's own trade statistics.

For example, let's consider what China reported about both its exports and imports for the month of June 2015:

On Monday, the General Administration of Customs said Chinese exports grew 2.8 percent last month from a year ago, beating forecasts for a 0.2 percent decline.

Imports fell for an eighth consecutive month, on a yearly basis, but the 6.1 percent drop was the smallest this year, and much better than the 15.0 decline expected by economists.

For June, China had a trade surplus of $46.5 billion, down from May's $59.5 billion. For the first half of 2015, the surplus was $263 billion, more than 2.5 times the figure in the same period last year.

Some analysts warned that the pick-up in China's trade in June may not last.

"Even though inventories at domestic companies stayed at a relatively low level in May and June, the economic fundamental is weak," said Nie Wen, an analyst at Hwabao Trust. "I doubt imports would continue to improve in the next few months."

The following chart shows what we measured as the year over year growth rate of the value of goods and services traded between the U.S. and China, after accounting for the exchange rate between the U.S. dollar and China's yuan.

What we see is that the year over year change in the value of what China exported to the U.S. grew by 4.4%, while the value of it imported from the U.S. rose to a growth rate of 0% from a year earlier. Digging into the detailed trade data for June 2015, we find that most of the unexpected increase in China's imports is attributed to the delivery of more commercial aircraft exported from the U.S. to Chinese airlines than in previous months.

Still, at 0% year over year growth in the value of goods it imports from the U.S, it's clear that China's export-dominated economy is continuing to sputter - especially if its own trade data were correct, because that would mean that the amount of trade between it and other regions of the world had to otherwise plummet during the month for those figures to be valid. Our pie chart below shows how China's export markets is dividend among the world's major economic regions:

Speaking of sputtering, since China reports its trade data one month ahead of when the U.S. does, let's get a glimpse of what direction the U.S. data will likely turn when the U.S. Census Bureau provides its report for July 2015:

China’s economy started the second half of the year on a weak note, posting disappointing trade and factory-price data in July amid pressure from slack demand at home and abroad.

Exports in July slid 8.3% from a year earlier, reversing a gain of 2.8% in June, customs data released Saturday showed. Imports fell for the ninth month in a row, dropping 8.1%, after a decline of 6.1% in June. And on Sunday, the government announced factory prices in July extended more than three years of declines, with the producer-price index taking its biggest year-over-year tumble in nearly six years.

While there were bright spots in the trade picture, as imports of some key commodities made gains in volume terms, the figures were generally worse than expected and pointed to problems ahead on the already struggling export side.

“We could see relatively strong downward pressure on exports in the third quarter,” Customs said in a statement accompanying the trade data.

With numbers like those coming after what had to be abysmal trade numbers in June 2015 in its other export markets, we can better understand why China adopted such an extreme intervention in the nation's stock markets in July 2015, as not doing so would almost certainly have led to a cascading failure in the nation's economy, which is an inherent danger of all centrally-planned and coordinated endeavors.

Update 9:00 AM EDT: In a "surprise" move, China has unexpectedly devalued its currency.

References

Board of Governors of the Federal Reserve System. China / U.S. Foreign Exchange Rate. G.5 Foreign Exchange Rates. Accessed 9 August 2015.

U.S. Census Bureau. Trade in Goods with China. Accessed 9 August 2015.

We don't normally follow the Dow Industrials index (NYSE: DJI), since it really doesn't capture enough of the breadth of the U.S. stock market, but last Friday, 7 August 2015 saw a pretty rare occurrence, with the Dow having closed lower than the previous day for the seventh consecutive trading day in a row.

While the S&P 500 fared slightly better by that measure over that same period of time, declining in only six of the same seven days, we wondered what its worst streaks were over its entire history.

To find out, we tapped Yahoo! Finance's S&P 500 historical price database and ran the numbers. The chart below reveals the number and duration of two or more consecutively down days that the index has recorded over the 16,506 trading days from 4 January 1950 through 7 August 2015.

Since 4 January 1950, we see that the S&P 500 has had losing streaks run seven trading days or longer some 44 times, with 23 of those streaks lasting exactly seven days before the index recorded an up day to break its losing streak.

The longest losing streak recorded over this period of time lasted twelve consecutive trading days, which began after it peaked on 21 April 1966 and lasted through 9 May 1966.

The timing of that longest losing streak roughly corresponds to the fallout from the Fed's decision on 12 April 1966 to begin "'restricting' rather than 'moderating' the growth in the reserve base, bank credit, and the money supply" available to the U.S. financial system, inaugurating a prolonged period of increased distress for the U.S. economy. That distress was indicated by the reversing momentum of the S&P 500 index, where it coasted on its previous upward inertia to top at 92.42 on 21 April 1966, after which it entered into a general period of decline until it finally bottomed at 73.20 on 7 October 1966, some 20.7% below its previous peak level. It would not recover to that former peak until 27 April 1967.

Unless there is significant erosion in the expectations for future dividends or a significant negative noise event, that kind of decline is unlikely to occur in today's market, but the general trend our rebaselined model of how stock prices work currently forecasts is such that the remainder of August 2015 would appear to be set to follow a downward trajectory.

Things would appear set to improve in September 2015, with the biggest boost coinciding with the timing of the Federal Reserve's Open Market Committee meeting in the middle of that month, but our limited ability to peer into the farther future suggests that would provide only a short term boost, as 2015 on the whole would appear to be set to be best described as a year of relative stagnation for U.S. stock prices.

Labels: forecasting, SP 500

Welcome to the blogosphere's toolchest! Here, unlike other blogs dedicated to analyzing current events, we create easy-to-use, simple tools to do the math related to them so you can get in on the action too! If you would like to learn more about these tools, or if you would like to contribute ideas to develop for this blog, please e-mail us at:

ironman at politicalcalculations

Thanks in advance!

Closing values for previous trading day.

This site is primarily powered by:

CSS Validation

RSS Site Feed

JavaScript

The tools on this site are built using JavaScript. If you would like to learn more, one of the best free resources on the web is available at W3Schools.com.

Other Cool Resources

Blog Roll