At the beginning of December 2009, we recognized that investors had effectively reached the edge of the chart in navigating the U.S. stock market. They had first reached the edge in October 2009, as they looked forward from that month to the fourth quarter of 2010 to set the value of stock prices with respect to the level of the S&P 500's dividend futures expected in 2010Q4.

The fourth quarter of 2010 marked the edge of the known world where the available dividend futures for U.S. stock markets at that time and, at this writing, it still does as dividend futures contracts extending into 2011 have yet to be opened. These futures contracts should be opened sometime in the first quarter of 2010.

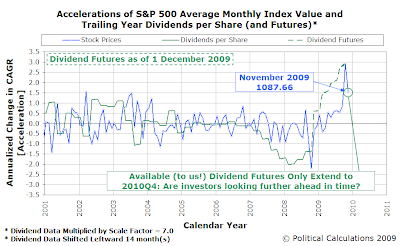

Here is what we observed at the time, as we recognized that investors were entering uncharted waters:

But we have a problem, and that problem is that we strongly suspect we've run over the edge of our chart. Here's exactly what we're looking at on 1 December 2009 as we consider our forecast:

There are two potential explanations for what we observe. The first is that investors have perhaps focused their attention upon the second quarter of 2010 instead of the fourth quarter, as we see that the level of the amplified change in the growth rate of dividends per share would seem to correlate reasonably well with the change in the rate of growth of stock prices we observed for November 2009.

That would make sense if there were some news affecting the expected future level of dividends per share to be paid in that quarter. However, we're unaware of any such news and in its absence, we think that to be unlikely.

The other potential explanation for what we see happening is that investors are looking past where they expect the S&P 500's dividends per share will be in 2010Q4 to the first quarter of 2011 instead, as determined by the dividend futures contract that applies for each quarter. That would make sense since the 2011Q1 contract would correspond to the period of time that includes the end of 2010, as the 2010Q4 futures contract only extends to 17 December 2010. That focus would also agree with much of what we observed during this year, with investors primarily focused from May through October upon the dividend futures contract for 2010Q1.

Today, we can confirm that both these potential explanations have elements that are both right and wrong. As we'll show you next, investors have indeed shifted their focus from where they expect the S&P 500's dividends per share will be in the fourth quarter of 2010 in setting the value of today's stock prices, but not to either where they expect they will be in the second quarter of 2010 or in the first quarter of 2011.

They've instead set them with respect to where they expect the S&P 500's trailing year dividends per share will be in the first quarter of 2010, just as they have throughout most of 2009!

In effect, stock market investors in the U.S. have returned to safer harbors. What we observe now is that the change in the rate of growth of stock prices in November 2009 was simply a transition between the two future points of investor focus.

With this knowledge, we can now revise our forecast for where the average of stock prices will be for the month of December 2009. Amplifying the value of the expected change in the growth rate of the S&P 500's trailing year dividends per share by scale factors of 6.5 to 11.0, which we've previously observed to be typical range for the U.S. stock market since January 2001, we project that the average of the S&P 500's closing daily index value for December 2009 will fall between 1101 and 1115, which is indicated as the converging orange region in the chart below. This marks an upward revision from the top end of our previous forecast range of 1032-1094, which is indicated by the dashed lines.

Having recorded an average value of 1105 through 22 December 2009, we find it very likely that stock prices will fall into our revised target range for the month.

Assuming that the average value of the S&P 500 index will end the month with the same average value of 1105 and that investors remain focused on 2010Q1, we would project that stock prices in January 2010 will fall between 1110 and 1123, provided there are no major changes in 2010Q1's expected dividend payouts.

And with that prediction based upon still incomplete data, we'll sign off for the year. Have a Merry Christmas and Happy New Year!

Labels: chaos, forecasting, SP 500, stock market

Do you have a geek in your life? Are you still looking for ideas for what to get them for Christmas?

Do you have a geek in your life? Are you still looking for ideas for what to get them for Christmas?

If so, you're in luck! Garth Sundem, most recently the author of The Geeks' Guide to World Domination, just announced the launching of new applications for the iPhone that are based upon the math he created for his previous book, Geek Logik!

Each of the applications are specifically designed to address the social dilemmas faced by geeks and ordinary people no matter where they are. The new apps cover Careers, Decisions and Love.

There's also a "Geek Logik Lite" version, available for free at this writing, which answers just three questions:

- Do you have a snowball's chance in hell with her?

- Should you call in sick to work?

- Should you wake up five minutes early?

Now, instead of awkwardly reacting to these and other potentially uncomfortable social situations, our heroic app user can instead pull out their mobile, disguising their discomfort by pretending the need to send an urgent text, while using the apps to instead solve their current social crisis, allowing them to move confidently forward in both real life and real time!

To get a better sense of those other potentially uncomfortable real life social situations that might now be answered while on the go, here's our index of the tools we developed based upon Garth's math from Geek Logik:

- What Are the Chances Your Marriage Will Last?

- Picking the Right Date for Valentine's Day

- Should You Call in Sick?

- Are You Too Good for Your Job?

- Should You Buy Something (or Not)?

- How Many Cups of Coffee Should You Drink This Morning?

- How Many Beers Should You Have at the Company Picnic?

- Earth Live: Walk, Bike or Drive?

- Should You Say It on the Grapevine?

- Should You Start or Stop Procrastinating?

- Should You Apologize?

- Should You Lie?

- Is Your Personal Grooming Adequate?

- Should You Quit Your Job?

- Should You Go Out with the Guys?...

- Are You Whipped?

- Should You Become Intimate with a Coworker?

- Do You Dare Run for Public Office?

- How Many Hours of Sports Can You Watch (Without Her Getting Angry)?

- Should You Stop to Put Gas in the Car?

Labels: geek logik

What does the future foretell for the U.S. economy in 2010? Well, why wonder when we can show you!

Our first graph shows how well the private sector of the U.S. economy is projected to perform, at least according to the expected trailing year dividends per share for the S&P 500. What we see is that this measure of economic health will likely bottom in the first quarter of 2010 and very slowly improve over the remainder of the year.

Our first graph shows how well the private sector of the U.S. economy is projected to perform, at least according to the expected trailing year dividends per share for the S&P 500. What we see is that this measure of economic health will likely bottom in the first quarter of 2010 and very slowly improve over the remainder of the year.

Looking instead at how these expectations have changed during the course of this year, the horizontal red bar indicates the range into which the S&P 500's dividends were expected to fall from 2009Q4 through 2010Q4 back on 22 June 2009. What our newer chart confirms is that U.S. economic performance clocked in just below what investors expected would happen in mid-2009, which we see in the vertical bars dropping below the range indicated by the horizontal red bar. We also see that they now anticipate a stronger recovery in 2010 than what they believed to be likely back in June 2009.

Let's look next at the expected level of dividends per share quarter by quarter through 2010. Here, we see that the bottom for the private sector of the U.S. economy occurred in 2009Q3. As a result, this quarter will be the most likely candidate for being the period of time in which the National Bureau of Economic Research (NBER) will declare the recession beginning in December 2007 to have ended.

Let's look next at the expected level of dividends per share quarter by quarter through 2010. Here, we see that the bottom for the private sector of the U.S. economy occurred in 2009Q3. As a result, this quarter will be the most likely candidate for being the period of time in which the National Bureau of Economic Research (NBER) will declare the recession beginning in December 2007 to have ended.

We also observe that the quarterly dividend value we're projecting for 2009Q4 isn't much of an improvement over 2009Q3, suggesting lackluster economic improvement. We'll note that we expect the final value for this quarter to be slightly different from the value indicated in the chart, as our method for anticipating a quarter's dividends typically puts us within 3-5 cents of the actual figure reported by S&P. S&P will report the value for the S&P 500's 2009Q4 dividend per share in January 2010.

If you look further forward into the future though, you'll see the bad news looming ahead - the U.S. economy will very likely reverse its momentum briefly in the second quarter of 2010. After this quarter however, investors currently anticipate that slow economic growth will resume through the end of 2010.

Consequently, the second quarter of 2010 is the most likely candidate to qualify as a double-dip for recession in the U.S. But then, this is the same as what investors have been expecting since at least August 2009.

This observation also provides an indication of how the job market in 2010 will play out. Job seekers can expect better luck in finding jobs into 2010Q1, then to drop off into the second quarter as companies freeze hiring plans until they can support new employees, and then to pick up again more strongly in the final two quarters of the year.

From our perspective, the only real question about the economy in 2010 is whether the NBER declare the recession to have ended in 2009Q3, which we think is most likely, or will they extend the end date of the recession to include part or all of 2010Q2?

Labels: forecasting

Welcome to the Friday, December 18, 2009 edition of On the Moneyed Midways, our final edition for 2009!

Welcome to the Friday, December 18, 2009 edition of On the Moneyed Midways, our final edition for 2009!

With Christmas and New Year's now a week away, OMM will resume with our Best Posts of 2009 edition and our Best Blogs We Found in 2009 edition on Thursday, 6 January 2010 and Friday, 7 January 2010 respectively! Our regular weekly edition will resume the following week, most likely on 14 January 2010 (assuming we don't box ourselves into a corner and need to schedule another dreaded "special" (aka "late") edition of OMM. Oh, and we'll finally get around to posting an index for all of this year's editions!

But rest assured that we're going out with a bang in this week's edition, as we're presenting two very timely posts on gift-giving - one to help you determine whether your gift is worth what you've paid for it and the other to help you be frugal and give something of value to those people for whom its difficult to decide what to get.

But neither of those posts ranks as being The Best Post of the Week, Anywhere! For that post, and the rest of this week's Absolutely essential reading, just scroll down....

| On the Moneyed Midways for December 17, 2009 | |||

|---|---|---|---|

| Carnival | Post | Blog | Comments |

| Carnival of Debt Reduction | You Can Never Earn Enough, So Quit Trying! | Eliminate the Muda | "You've go to count your pennies before you count your dollars." The LeanLifeCoach reflects on the wisdom of the advice that he received early in his working life. |

| Carnival of Personal Finance | Giving a Gift Someone Actually Likes or Wants Doubles the Value | Steadfast Finances | Steadfast Finances advocates a very different way to decide how well you've matched a gift to the person to whom you're giving it: take the value they place on the gift and add it to the value you place on the joy you receive in giving it. If the combined value it adds to up more than what you paid for the gift, you likely have a winner! The Best Post of the Week, Anywhere! |

| Carnival of Real Estate | Can the World Get a Good CRM for Real Estate… Please? | Bigger Pockets | What Ben Roberts really wants is a solid Customer Relationship Management tool. He specs the kind of application he's after and asks why doesn't it exist yet. |

| Cavalcade of Risk | Wage and Hour Suits Heat Up for Health Care Organizations | Risk Management for the 21st Century | Nancy Germond discusses the class action lawsuits that are making employers rethink their policies of "off-the-clock" employee activities, such as allowing them to eat lunch at their workstations. |

| Festival of Frugality | Three Frugal Gift Ideas for the Difficult People on Your List | Family Balance Sheet | Kristia lists three inexpensive things to give the people for whom you have no idea of what to get! |

| Festival of Stocks | The David Swenson Asset Allocation Model | The Dividend Guy | Should you model your investment portfolio based upon how David Swenson, who has averaged 16.3% annual returns since becoming the manager of Yale University's Endowment Fund has allocated that portfolio's assets? The Dividend Guy shares what he learned reviewing Swenson's investing advice for human investors! |

| Money Hacks Carnival | Tales from the NBA: A Baller on a Budget | Free Family Finance | FMF considers how professional basketball rookie Brandon Jennings might be a financial all-star on top of being a likely candidate for the NBA's rookie-of-the-year. Absolutely essential reading for the more-than-60% of professional athletes who are likely to declare bankruptcy once their playing days end and anyone who needs a stronger appreciation of the need for spending discipline! |

| Carnival of Money Stories | Reminiscences of a Stock Market Wallflower | Monevator | The Investor sat out the Dot-Com bubble, but learned an amazing amount of information on how to invest from it! |

| Facing Up Budget Blog Carnival | The Definition of Economic Insanity | Facing Up to the Nation's Finances | With two massive economic "stimulus" packages in two years, and a third major economic stimulus package now being advocated, Conn Carroll questions why it makes any kind of sense to rack up even more deficit spending to "stimulate" the U.S. economy when the first two attempts failed to forestall growing job losses. The Best Post of the Week, Anywhere! |

Previous Editions

- OMM's Running Index for 2008

- OMM's Running Index for 2007

- The Best Blogs Found in 2006 (and our full 2006 index)!

Labels: carnival

For the first time since April 2009 and the second time since April 2008, the overall employment situation improved in the United States in November 2009. Even for teens!

Compared to the previous month's data, the BLS' Labor Force Statistics indicate that 10,000 additional teens were counted as being employed than in the previous month, bringing that portion of the U.S. labor force up to 4,462,000. In October 2009, some 4,452,000 individuals Age 16-19 were counted as working, which marks the lowest point for U.S. teens since their employment levels began declining steadily in January 2007.

Compared to the previous month's data, the BLS' Labor Force Statistics indicate that 10,000 additional teens were counted as being employed than in the previous month, bringing that portion of the U.S. labor force up to 4,462,000. In October 2009, some 4,452,000 individuals Age 16-19 were counted as working, which marks the lowest point for U.S. teens since their employment levels began declining steadily in January 2007.

Compared to the peak of teen employment of June 2006 of 6,244,000, some 1,782,000 teen jobs, or 28.5%, have disappeared from the U.S. economy. Taking the average of the teen employment level for the year of 2009 through November, teen employment has declined by an average of 1,258,705 from its 2006 year-long average of 6,161,250.

Since December 2007, which the National Bureau of Economic Research declared to be the peak of the previous expansion of the U.S. economy, making it the starting point for recession, the employment level for teens Age 16-19 has fallen by 1,399,000, representing 17.1% of the total decline of 8,163,000 jobs since the latest recession began as of November 2009. That compares with 1,529,000 for young adults of Age 20-24, who account for 19.0% of that decline. Together, individuals Age 16-24 represent 36.1% of all jobs lost since the declared beginning of the recession.

Since December 2007, which the National Bureau of Economic Research declared to be the peak of the previous expansion of the U.S. economy, making it the starting point for recession, the employment level for teens Age 16-19 has fallen by 1,399,000, representing 17.1% of the total decline of 8,163,000 jobs since the latest recession began as of November 2009. That compares with 1,529,000 for young adults of Age 20-24, who account for 19.0% of that decline. Together, individuals Age 16-24 represent 36.1% of all jobs lost since the declared beginning of the recession.

As a percentage of the entire U.S. labor force in November 2009 of 138,502,000, teens represent 3.22% and young adults Age 20-24 account for 8.99% of the total. Those Age 16-19 are therefore 5.3 times more likely to have been affected by job loss during the recession than their percentage representation in the U.S. workforce would suggest, while those Age 20-24 are 2.1 times as likely.

Of course, there's a reason for that!...

The good news is that at least one economist at the University of Chicago has begun to catch on to why teens and young adults would seem to be so disproportionately affected by disappearing jobs. Oddly, the economist only seems to think that it only became an issue in July 2009. Rather than, say, January 2007, when the people who might hire teens and young adults began reacting to the situation that developed by not creating jobs for these youngest, least educated and least experienced potential members of the U.S. workforce:

It's an odd thing, this kind of economic myopia!

Labels: jobs, minimum wage

The motion of pendulums has been studied by students of physics for centuries. As a result, this kind of motion is really well understood. So much so that it's considered to be very predictable, and there are even simple online computer simulations based upon the fairly simple math that it takes to describe the mechanical motion of a pendulum operating under a constant gravity.

But what happens when you take a simple pendulum and add a couple of others? Then set the whole thing spinning?

What you get is chaos, or rather, really unique motions that arise from the complex interactions of otherwise very simple mechanics.

But don't take our word for it. As with all things these days, there's a YouTube video to demonstrate this principle in action! Just *try* to predict which way the whole pendulum, or its individual arms, are going to move next:

Again, pendulum motion is something that people have understood pretty well for centuries. And yet, add just a couple of additional pendulums to a simple system and the motion you get is highly unpredictable.

There's a lesson here somewhere....

Labels: chaos, none really

Perhaps nothing inspires more dread during the busy shopping season than the prospect of having to perform the most difficult maneuver most people might face while driving: parallel parking.

Perhaps nothing inspires more dread during the busy shopping season than the prospect of having to perform the most difficult maneuver most people might face while driving: parallel parking.

Fortunately for readers of Political Calculations, we now have the tool you need to decide if you should even attempt to squeeze your car into that tiny space between those two big cars parked alongside the road. The tool below was developed by Simon Blackburn of the University of London (HT: PhysOrg, who was commissioned by Vauxhall Motors to write The Geometry of Perfect Parking, which provides the mathematical formula we need to determine how big that parking space needs to be for your car!

The rest is just a matter of entering your car's and your parking situation's relevant information into our tool. The default data is that for a Corvette C5 (we can dream, can't we?!), with several of the dimensions entered in units of inches, which we've divided by 12 in the input fields below to convert into feet. We did make one assumption since we didn't have the specific data: that the distance from the nose of the car to the center of the front wheels is half the difference of the car's overall length and its wheel base.

And now that we've developed and presented this tool for your use, let us reassure you that we have absolutely no interest in discussing the subject of parallel parking, or the parking of vehicles any kind, any further. Interestingly, we note that Professor Blackburn also strongly affirms that he has little interest in discussing the subject given his greater interest in more challenging fields of mathematics, and he also notes that Rebecca Hoyle of the University of Surrey, perhaps the only other person in the world to have done similar math, isn't interested in parking as a research topic either.

It seems that aspect of parallel parking has similar rules to those of Fight Club.

Labels: none really, tool

Welcome to the Friday, December 11, 2009 edition of On the Moneyed Midways! Each week, we review the best of the past week's business and money-related blog carnivals and find the best posts in each, which we then list here to kick off your essential weekend reading!

Are you a gambler or an investor? Did Fannie Mae just hose you if you're shopping for a house? What do managers who fear confrontation do with their non-performing employees? What might make so-called "good debt" be bad for you?

The answer to these questions, and the rest of the best posts of the week that was, are just a click away....

| On the Moneyed Midways for December 11, 2009 | |||

|---|---|---|---|

| Carnival | Post | Blog | Comments |

| Carnival of Debt Reduction | How to Reduce Your Debt Significantly Without Tightening Your Belt | Personal Finance Analyst | David R. Lampsen's idea isn't revolutionary, but it can be effective: you change what you consume by replacing higher priced things you currently buy with less expensive substitutes. The real trick is to channel your savings toward reducing your debt or increasing your savings! |

| Carnival of HR | The Cowardly Manager's Guide to Dealing with Poor Performers | Great Leadership | Got an employee who's not pulling their weight? Don't really want to confront them about the issue? Dan McCarthy lists 11 ways managers without guts handle the poor performers among their staffs in Absolutely essential reading! |

| Carnival of Personal Finance | When Good Debt is Bad | Modern Gal | Student loans and mortgages have the reputation of being "good debt," but Elizabeth says that's not necessarily true. She asks the questions about these kinds of debts whose answer might put them in the "bad" category. |

| Carnival of Real Estate | Getting a Loan Just Got Tougher: Fannie Mae Changes Debt to Income Ratio | MyHomeHouston | The team at MyHomeHouston reacts to Fannie Mae's dropping of the maximum allowable debt-to-income ratio a potential homebuyer must satisfy from 55% of their income to 45%, wondering if that change will make a recovery in U.S. housing markets less likely to gain traction. |

| Carnival of Taxes | Should Someone Receiving Government Aid Give to Charity? | My Life ROI | MLR reacts to an angry letter written to a New York Times Magazine columnist condemning an individual's decision to donate 10% of his income received from unemployment compensation to his church. |

| Festival of Frugalilty | No Costco Membership? Shopping at Costco Still Saves Money | Digerati Life | Julia Scott describes how membership isn't necessarily required to take advantage of the services the warehouse retailer provides! |

| Best of Money | Are You a Gambler or Investor? | Bullishness | Soo-Young flow charts The Best Post of the Week, Anywhere! in helping you determine whether you're investing or gambling. We love Question 1: "Is your position based on a rumor, hunch or Cramer recommendation?" |

Previous Editions

- OMM's Running Index for 2008

- OMM's Running Index for 2007

- The Best Blogs Found in 2006 (and our full 2006 index)!

Labels: carnival

Today, we're celebrating our fifth anniversary as we have in previous years by sharing the most amazing discovery we've made in the past year. Unlike the previous three years, in which we put the entire history of the S&P 500 at Your Fingertips, uncovered the basic fundamental relationship of the stock market and revealed how changes in investor expectations directly drive stock prices, today's post has nothing to do with the stock market.

Today, we're celebrating our fifth anniversary as we have in previous years by sharing the most amazing discovery we've made in the past year. Unlike the previous three years, in which we put the entire history of the S&P 500 at Your Fingertips, uncovered the basic fundamental relationship of the stock market and revealed how changes in investor expectations directly drive stock prices, today's post has nothing to do with the stock market.

Instead, we've identified the conditions that trigger U.S. politicians into making significant changes in personal income tax rates.

Sounds pretty mundane, right? After all, politicians are always tweaking this or adjusting that in the U.S. tax code, which goes a long way to explaining why it has grown over time to be over 3.7 million words long.

But what politicians don't do very often is change the marginal tax rates that apply to individual income earners in the United States.

The reason why is pretty straightforward. These tax rates are the most visible part of the U.S. tax code. Unless politicians are taking the popular step of reducing them, they try to avoid making any changes in these rates. In the case of increasing the tax rates significantly, they will most often do so only when they have a strong consensus, say in the historical case of a declared war or other crisis, or when the political party in power has a large majority in the U.S. Congress and can achieve its aims without bipartisan compromise.

What we end up with then is a system where tax rate changes most often occur at the margins. The two questions that arise from that observation are "what are those margins" and "where are they"?

We know that once elected, politicians seek to retain the power of their office by putting money in their supporters' pockets. That happens in two ways: by spending the money that it borrows and that it collects through taxes to benefit their supporters or by reducing the amount of taxes their supporters have to pay.

These two things obviously contradict each other, but the balance and conflict that exists between them explains quite a bit. Politicians risk alienating supporters if they raise taxes too high to support the spending they believe will keep them in office, so they will seek to keep spending high and taxes low by borrowing the money needed to make up the difference between what the government collects and what the politicians want to spend.

The problem with that strategy is that if the amount of borrowing continually grows faster than the government's tax collections, it sets up the situation where tax rates must be raised to support the spending initiatives of the politicians. The politicians can get away with this for short periods of time, but once the level of debt grows too high, the people the politicians borrow money from will require taxes be raised as a condition of continuing to do business. In other words, the politicians put the government into a position similar to that of a distressed business nearing failure, where the business must do the things their creditors dictate, especially if they wish to keep borrowing money to keep in control of the business.

No, that's not healthy. Unlike a failing business however, the government has the power of being a monopoly, one that can force people into doing business with it. Or in this case, one that can compel people to pay more for it without having to deliver more or better benefits.

The amount of money the government can collect will then be proportional to the number of people it can tax and the amount of money they earn.

All these factors are represented in what we define as the national debt burden per capita. This is the ratio of the national debt to national income (also called gross domestic product, or GDP), divided by the total population. This result is then multiplied by a scale factor. We use a scale factor of one billion, which makes the resulting figures a lot friendlier to deal with.

Now that we've identified the things that define the margins for where politicians operate, we can now see how those things affect where they set tax rates. To do that, we've plotted the maximum income tax rate since 1913 against the debt burden per capita we've calculated for each year since. We used Zunzun's 2-D function finder to perform a regression analysis of the data, which is represented by the curve passing through the center of the data points.

Now that we've identified the things that define the margins for where politicians operate, we can now see how those things affect where they set tax rates. To do that, we've plotted the maximum income tax rate since 1913 against the debt burden per capita we've calculated for each year since. We used Zunzun's 2-D function finder to perform a regression analysis of the data, which is represented by the curve passing through the center of the data points.

We next calculated the standard deviation of the data with respect to the central curve, then through a process of trial and error, graphed two parallel curves some 1.25 standard deviations away from the central curve.

What we find is remarkable, in that we see that once the data falls outside these margins, politicians act within a relatively short period of time to pull back within them.

How they choose to do that varies by circumstance. Going chronologically, here's what we observe:

- We see a small tax hike from 1915 to 1916, as the U.S. began gearing up for its entry into World War I, then a significant increase in the maximum tax rate as the U.S. entered the Great War in 1917. The amount of debt then surged, pulling the U.S. close to the central curve.

- The maximum tax rates were held steady for a few years, but began decreasing as the national debt burden per capita decreased. The maximum tax rates settled near the lower margin in the late 1920s.

- The maximum tax rate was held level as the Great Depression began, but the debt burden per capita soon surged, pushing to the lower margin in 1931. Both tax rates and the debt burden per capita surged in 1932 as the U.S. fell deeper into the depression.

- The national debt burden per capita continued to rise, eventually triggering additional tax rate increases in the late 1930s. After 1939, the debt burden per capita began falling, until 1941.

- With the U.S. declaring war against both Japan and Germany following the 7 December 1941 attack on Pearl Harbor, personal income tax rates soon reached their historic highs and the debt burden per capita surged to levels not seen since the Civil War. Both tax rates and the debt burden per capita began falling after the conclusion of World War II in 1945.

- The maximum tax rate remained high as the debt burden per capita dropped off rapidly following the war. The maximum tax rate was increased in 1950 and again in 1952, before being decreased slightly after 1954. The maximum tax rate then held steady even as the national debt burden per capita declined into the early 1960s.

- The maximum tax rate pushed outside the upper margin in the early 1960s, which prompted the 1963 tax rate reduction in stages over two years. Rates held level as the debt burden per capita continued declining until 1968.

- In 1968 though, the U.S. Congress pushed through a 10% surtax on top income earners, pushing the maximum tax rate once again above the upper margin given for the respective national debt burden per capita. This prompted a rapid correction by lawmakers of the day, who responded by returning the top marginal tax rate back to the 70% by 1971.

- That level was just at the threshold of the upper margin. Tax rates held steady at this level throughout the 1970s, as the national debt burden per capita fell slowly, moving further outside the upper margin.

- In 1982, both marginal tax rates were slashed to 50% and the national debt burden per capita began increasing with the policy initiatives of the Reagan administration.

- The tax reform of 1986 saw tax rates drop to the lower margin, as these lowest rates of the postwar era took effect in 1987. The national debt burden per capita rose, moving outside the lower margin.

- Both the maximum income tax rate and the national debt burden per capita rose, paralleling the lower margin curve. The national debt burden per capita though continue to push outside the lower margin, which sparked a larger tax increase in 1993.

- At 39.6% throughout the rest of the 1990s, the national debt burden per capita fell with the strong economic growth of the period. That reversed with the recession of 2001, which continued to 2003.

- The maximum income tax rate was reduced in 2003, and during the period from 2003 to 2007, there was little movement in the national debt burden per capita as the national debt paced the growth of both population and GDP, staying well within the lower margin. That ended with the recession and banking crisis of 2008.

- 2008 saw a shift toward the lower margin as the economy fell into recession and the government acted to bail out distressed financial institutions. The national debt burden per capita then accelerated with the ascension of Barack Obama, pushing well outside the lower margin in 2009.

Using the White House's Office of Management and Budget's forecast for each year from 2010 to 2014 contained within Table 1.2 of the Historical Tables of the U.S. Budget, we've shown the trend the Obama administration expects after tax rates rise with the expiration of the 2003 tax cuts after 2010.

Unfortunately, these forecasts presume strong economic growth similar to that of the 1990s and do not incorporate the costs of the proposed health care reform now being considered in the U.S. Congress, so this trend is unlikely to be observed. Regardless, since these data points fall outside the lower margin, we can reasonably anticipate that a significant increase in marginal tax rates will be enacted.

If the Obama administration holds to the recent practice of U.S. politicians of keeping near the lower margin, the expected national debt burden for 2011 of 2.9 indicates that the top marginal income tax rate will increase to roughly 44-45%. Given the President's political party's current large majority in the U.S. Congress, it is possible that tax rates could go much higher. The tax rate corresponding to the central curve for the national debt burden expected in 2011 is 67-68%.

Happy 5th anniversary! We wish we had better news for you!

Labels: taxes

We have ourselves a cage match in the stock market today! CNN reports that U.S. markets are "poised for a rebound Wednesday", and the Associated Press reports this morning that "stock futures rise after sell-off as dollar falls."

We have ourselves a cage match in the stock market today! CNN reports that U.S. markets are "poised for a rebound Wednesday", and the Associated Press reports this morning that "stock futures rise after sell-off as dollar falls."

But, today's dividend futures data for the S&P 500 indicates that we should expect stock prices to fall.

Seeing as we turned out to be right last Thursday, when stock prices rose (even though the value of the U.S. dollar rose as well,) we'll go with what the dividend futures are telling us as our market prediction for the day.

A couple of other notes on last Thursday's prediction. That rise in stock prices occurred even as commodity prices and many of their related stocks fell, suggesting that dividend futures provide a stronger signal for stock prices to follow than the changing value of the U.S. dollar, which we consider to be a component of noise in the market. We also correctly anticipated in our morning update to that post that the market's reaction to the better-than-expected jobs report of that day would be short-lived. The spike from that good news appears to have only lasted until about noon that day!

Over the weekend, we'll note that the dividend futures fell below where they had been before we noted their jump in value, but the market didn't appear to absorb that information until Tuesday, December 8. If the noise from the falling dollar is strong enough today to counteract the change we observe in dividend futures, we might see a similar delayed reaction.

Like we said at the beginning, it's a cage match!

Update 6:32 PM EST: Dividend futures won the kickoff and held the lead for most of the day, but ultimately, new noise broke out late in the day, replacing the original team and carried the day!

Labels: forecasting

Hauser's law is one of the stranger phenomenons in economic data. It was originally proposed by Kurt Hauser, who observed back in 1993 that:

No matter what the tax rates have been, in postwar America tax revenues have remained at about 19.5% of GDP.

We decided to put Hauser's Law to the test to see if it holds up. To do that, we turned to the National Taxpayers Union, which maintains a table showing the level of the topmost marginal income tax rates for individuals from 1913 through the present. Looking just at the postwar period, we find that the marginal tax rate that applies for the U.S.' uppermost income tax bracket has ranged from a high of 92% in 1953 and 1954 to a low of 28% from 1988 through 1990. The current top rate is 35%, which is scheduled to increase after 2010 to 39.6% when the tax cuts of the 2003 Jobs and Growth Tax Relief Reconciliation Act expire.

We next turned to the Table 1.2 Summary of Receipts, Outlays, and Surpluses or Deficits as Percentages of GDP: 1930-2014, which is produced by the White House's Office of Management and Budget, since this Excel spreadsheet contains both the amount of total federal government tax revenues (aka "receipts") and the value of GDP for each of our years of interest, including forecasts for these values from 2009 through 2014.

But that's not all. It occurred to us that those total tax receipts include money from a lot more tax sources than just personal income taxes. Things like Social Security taxes, Medicare taxes, corporate income taxes, capital gains and excise taxes all contribute to the governments total tax collections. We wanted to also see how changing the individual income tax rates affected personal income tax collections, so we extracted the historic data on personal income tax collections provided by the Center on Budget and Policy Priorities through 2003, updated with data from the IRS for 2004, 2005 and 2006, the most recent year for which we could obtain the data and calculate the corresponding percentage share of GDP.

The results of what we found in doing this are graphically presented in the double chart (click for a larger image), where we've also indicated periods of recession.

The results of what we found in doing this are graphically presented in the double chart (click for a larger image), where we've also indicated periods of recession.

What we find in looking at the lower chart is that the federal government's tax collections from both personal income taxes and all sources of tax revenue are remarkably stable over time as a percentage share of annual GDP, regardless of the level to which marginal personal income tax rates have been set.

We also find that both total and personal income tax receipts appear to follow a normal distribution with respect to time. We calculate that personal income tax collections as a percentage share of GDP from 1946 through 2006 has a mean of 8.0%, with a standard deviation of 0.8%, which we've indicated by the horizontal orange band on the chart. We would expect that annual personal income tax collections would fall within the range indicated by the orange band some 68.2% of the time. We've also indicated upper and lower limits for personal income tax receipts, which correspond to the mean value we observe plus or minus three standard deviations, as we would expect personal income tax collections in any given year to fall within this range some 99.6% of the time.

Likewise, we see a similar pattern in total tax receipts. Here, we observe that total tax collections as a percentage share of annual GDP over the historic and forecast period have a mean value of 17.8% with a standard deviation of 1.2%.

We also observe that the three periods in which the federal government's tax receipts have risen above the orange bands marking a one-standard deviation difference from the mean value, each of which coincide with unusual circumstances, which we've indicated in the double chart with the light green vertical bands:

- In 1968, the Democratic U.S. Congress and President Lyndon Johnson passed a 10% income surtax that took effect in mid-year, which suddenly raised the top tax rate from 70% to 77% (which increased the amount collected from top income tax earners by 10%.) Coupled with a spike in inflation, for which personal income taxes were not adjusted to compensate, this tax hike led to outsize income tax collections in that year.

- The sustained high inflation of 1978 (7.62%), 1979 (11.22%), 1980 (13.58%) and 1981 (10.35%) led to higher tax collections through bracket creep, as income tax brackets in the U.S. were not adjusted for inflation until 1985 as part of President Ronald Reagan's first term Economic Recovery Tax Act.

- Beginning in April 1997, the Dot Com Stock Market Bubble created an excessive number of new millionaires as investors swarmed to participate in Internet and "tech" company initial public offerings or private capital ventures, which in turn, inflated personal income tax collections. Unfortunately, like the vaporware produced by many of the companies that sprang up to exploit the investor buying frenzy, the illusion of prosperity could not be sustained and tax collections crashed with the incomes of the Internet titans in the bursting of the bubble, leading to the recession that followed.

Now, what about those other taxes? Zubin Jelveh looked at the data back in 2008 and found that as corporate income taxes have declined over time, social insurance taxes (the payroll taxes collected to support Social Security and Medicare) have increased to sustain the margin between personal income tax receipts and total tax receipts. This makes sense given the matching taxes paid by employers to these programs, as these taxes have largely offset a good portion of corporate income taxes as a source of tax revenue from U.S. businesses. We also note that federal excise taxes have risen from 1946 through the present, which also has contributed to filling the gap and keeping the overall level of tax receipts as a percentage share of GDP stable over time.

More practically, Hauser's Law provides a method we can use to anticipate the likely range for how much money the U.S. government will collect in any given year, from just personal income taxes or in total, given that year's level of GDP.

Labels: taxes

If it weren't for the extraordinary expenditures the U.S. federal government has undertaken in recent years, such as for the wars in Iraq and Afghanistan, as well as the various bailouts and economic stimulus spending initiatives, how much would it be spending? Better yet, how much would it be committed to spending at a minimum for each year from now through 2080?

Here at Political Calculations, we ask and answer questions like these and what's more, we build tools so you can too!

What we've done for our latest project is to take the Congressional Budget Office forecasts for the "extended baseline" growth of various "mandatory" spending items into the future as part of its most recent Long Term Fiscal Outlook, which considers such programs as Medicare, Medicaid, Social Security and the Net Interest payments that must be made each year on the U.S. National Debt, and combine that with the baseline spending given by various discretionary spending programs, such as highways and mass transit, farm subsidies, et cetera, as given by the White House's Office of Management and Budget historical tables for these kinds of expenditures in recent years.

We determined each as a percentage share of GDP for any given year from 2009 through 2080, which means we just need to project what GDP would be for each year from now through then! That was easy, since the Social Security Administration's OASDI Trustees had already done that exercise for us from 2009 through 2085 as part of their annual review of the long term health of Social Security's retirement benefits program!

The results of that project are now just a few clicks away....

Why Baseline Government Spending?

To be able to anticipate what impact a new spending initiative or a change in an existing expenditure will have, you have to compare it against some reference point, namely, the spending that would most likely have occurred if the government were left on auto-pilot. By determining what that level spending is, we now have a tool we can use as a base of reference against which we can measure the cost impact to U.S. taxpayers of the decisions implemented by the country's elected officials and bureaucrats.

About the Data Behind the Tool

For National Defense, we used the percentage share of GDP indicated by the Congressional Budget Office that would apply in 2019 as our baseline value of 3.4%, when the United States' currently active military operations will presumably have long-since concluded. Historically, this value ranges between 3.0% and 4.0% of GDP, but has been higher than this range in recent years due to the decisions taken by both the Bush and Obama administrations, most notably to support significant military operations in both Iraq and Afghanistan.

Otherwise, we calculated the baseline percentage share of GDP for each budgetary line item provided in the OMB's Budget of the United States Government Fiscal Year 2010 Historical Tables 3.2 for 2007, since this year precedes the economic crises of 2008 and would be considered to be representative of a relatively typical level of spending in a non-economic crisis political environment. We noted that the majority of line-items listed in the tables were stable as a percentage of annual GDP from year to year.

We modeled the change in expenditures over time for the Medicaid, Medicare, Social Security and Net Interest mandatory spending line items in the U.S. federal government's budget using the data provided by the CBO in its Long-Term Budget Outlook, which it released in June 2009.

The projections for future GDP were modeled from data provided by in the Social Security Administration's 2009 OASDI Trustees Report, specifically from the Trustee's intermediate cost assumptions presented in Table VI.F6. - Selected Economic Variables, Calendar Years 2008-85. The OASDI Trustees describe their assumptions in Section 5 of the report.

Labels: economics, forecasting, gdp, politics

Welcome to our regular Friday, December 4, 2009 edition of On the Moneyed Midways, where we present the best posts we found in the best of the past week's business and money-related blog carnivals for your weekend reading pleasure!

We have a short edition this week, as we're falling in between the posting cycle for the biweekly and monthly business and money-related blog carnivals we regularly track. We also have a rare off-week for the Carnival of Real Estate, which looks to reappear in time for our next edition.

Other than that, we'd like to point you The Best Post of the Week, Anywhere! for the results of J. Money's experiment,, which we suspect many of you would love to try at least once in your life, but have been afraid to throw down the money it would take to find out if it would really work.

That post, and the rest of the best posts we found in the week that was, are ready for your review....

| On the Moneyed Midways for December 4, 2009 | |||

|---|---|---|---|

| Carnival | Post | Blog | Comments |

| Carnival of Debt Reduction | Raise the Bridge or Lower the Water | Eliminate the Muda | The LeanLifeCoach considers the two things you can do to give yourself more breathing room where your personal finances are concerned. |

| Carnival of Personal Finance | Bad Debt to Income Ratio | Money Funk | Christine describes how she used the Motley Fool’s guide to calculating a “bad debt” to after-tax income ratio to get a better grasp on how her debts were weighing her down. Absolutely essential reading for the attached spreadsheet! |

| Festival of Frugality | Oil Cleansing Method | Ultimate Money Blog | Mrs. Money reveals how she uses a blend of castor and olive oils to clean the oils from her skin. Yeah, it sounds crazy, but makes sense after you read it! |

| Carnival of Money Stories | Five Steps to Six Figures in Seven Years | Free Money Finance | FMF provides the kind of career advice that you wish you had back in high school, describing how to combine education and aggressive career management to generate a six-figure income. |

| Best of Money | Results of the $100 Scratch Off Lottery Project | Budgets are $exy | What if you had $100? Would you buy 100 scratch off lottery tickets to try to win more money? J. Money tests out this investing strategy, finds that they measure some 33 feet when laid out end-to-end and are 2 inches thick when stacked, and reports the financial results in The Best Post of the Week, Anywhere! |

| Cavalcade of Risk | Workers' Compensation Metrics: Creating a One-Page Scorecard | Workers Comp Insider | How should the impact of worker injuries be measured and communicated to senior management? Tom Lynch presents his idea for a consistent, simple and meaningful scorecard approach so they can make more informed decisions more quickly. |

Previous Editions

- OMM's Running Index for 2008

- OMM's Running Index for 2007

- The Best Blogs Found in 2006 (and our full 2006 index)!

Labels: carnival

Welcome to the blogosphere's toolchest! Here, unlike other blogs dedicated to analyzing current events, we create easy-to-use, simple tools to do the math related to them so you can get in on the action too! If you would like to learn more about these tools, or if you would like to contribute ideas to develop for this blog, please e-mail us at:

ironman at politicalcalculations

Thanks in advance!

Closing values for previous trading day.

This site is primarily powered by:

CSS Validation

RSS Site Feed

JavaScript

The tools on this site are built using JavaScript. If you would like to learn more, one of the best free resources on the web is available at W3Schools.com.

Other Cool Resources

Blog Roll